How to Avoid Double Taxation Between the US and Canada: A Comprehensive 2026 Guide

Did you know that the Canada-US Tax Treaty does not automatically protect your income simply because you live or work across the border? Many taxpayers realize too late that double tax relief is a strategic filing process rather than a default setting. It is a common frustration to feel as though you are working for two different governments at once, especially when you are trying to avoid double taxation US Canada while managing conflicting filing deadlines and differing regulations.

We understand the deep-seated stress that comes with the fear of IRS penalties or the confusion over how retirement savings are treated by two separate nations. You deserve a clear, reliable path to financial stability. This comprehensive 2026 guide promises to show you how to leverage treaty benefits to protect your wealth and ensure you never pay more than is legally required. We will walk through the specific forms needed under IRS rules, explain how to claim credits for CRA filers, and provide a methodical roadmap for total cross-border compliance.

Key Takeaways

- Understand how the Canada-US Tax Treaty serves as your primary shield to protect your income from being taxed by both countries simultaneously.

- Learn how to correctly determine your residency status under IRS rules and CRA guidelines using specific tie-breaker provisions to resolve conflicting claims.

- Discover the strategic use of Foreign Tax Credits and exclusions to effectively avoid double taxation US Canada and minimize your overall tax burden.

- Identify the specific treaty-reduced withholding rates for passive income, such as dividends and interest, to ensure you retain more of your cross-border investments.

- Realize the importance of coordinated filing to maintain total compliance with both the IRS and CRA while safeguarding your long-term retirement savings.

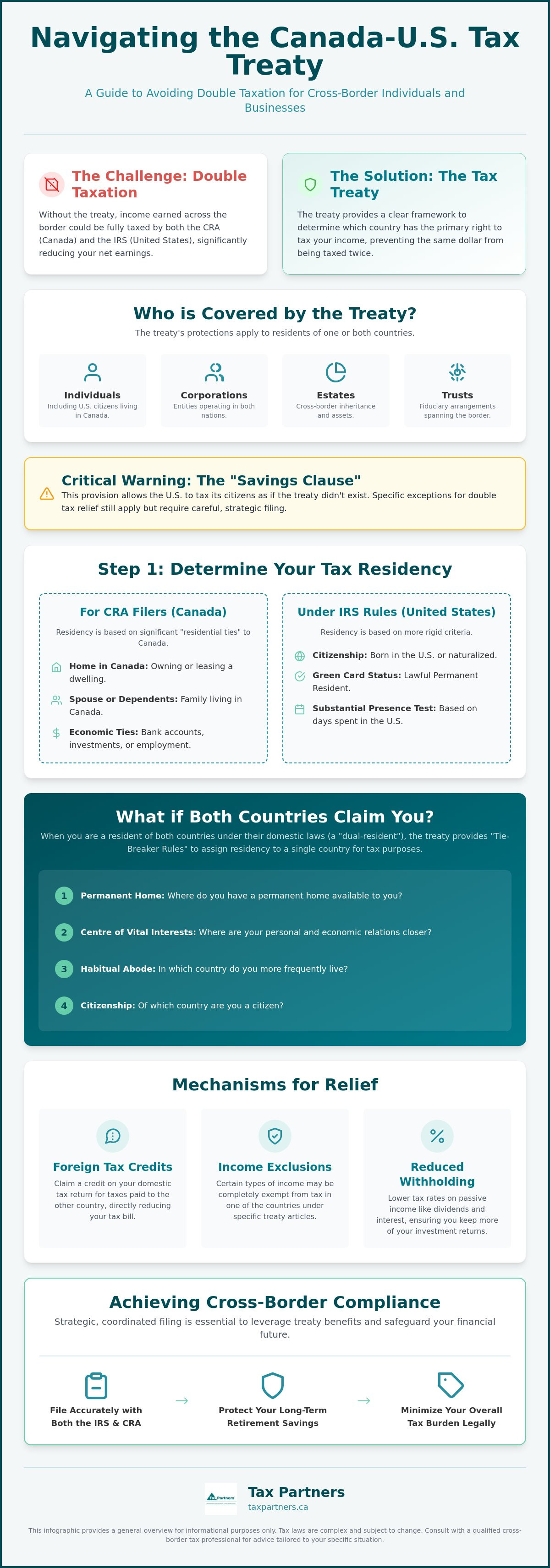

Understanding the Canada-US Tax Treaty Framework

The cornerstone of any strategy to avoid double taxation US Canada is a bilateral agreement formally known as the Convention Between Canada and the United States of America with Respect to Taxes on Income and on Capital. Most people simply call it the Treaty. Its primary purpose is twofold: to prevent fiscal evasion and to eliminate the heavy burden of being taxed twice on the same dollar. This Canada-US Tax Treaty Framework provides a structured set of rules that reconcile the federal income tax laws under IRS rules with the Income Tax Act for CRA filers. Without this agreement, many residents would face punishing tax rates that could effectively stall cross-border investment and mobility.

The treaty acts as a jurisdictional map. It establishes which country has the primary right to tax specific types of income, such as employment earnings, dividends, or interest. By defining these boundaries, it allows taxpayers to plan with certainty. It transforms what could be a chaotic regulatory overlap into a manageable, predictable process of compliance. This clarity is essential for anyone looking to organize their financial life across the 49th parallel.

Who is Covered by the Treaty?

The treaty applies broadly to residents of Canada, the United States, or individuals who hold residency in both nations simultaneously. This coverage extends beyond just individuals; it includes corporations, estates, and trusts. It's particularly vital for US citizens living in Canada. Because the US taxes its citizens on their global income regardless of where they live, these individuals often find themselves caught between two jurisdictions. The treaty provides the necessary mechanisms to ensure that the IRS and CRA don't both take a full share of the same income. It helps you realize the full potential of your earnings without unnecessary loss to dual taxation.

The Savings Clause: A Critical Warning

Despite the protections offered, the treaty contains a provision known as the Savings Clause. This clause essentially allows the US to tax its citizens as if the treaty did not exist. It's a significant hurdle that can catch the unwary off guard. However, there are specific exceptions to this clause that still allow for double tax relief through credits and exemptions. Because these rules are intricate, navigating them requires a precise approach. Relying on professional US tax services or specialized Canadian tax services is the best way to ensure you don't fall victim to these complex overlaps. Protecting your wealth requires foresight and a deep understanding of how these two systems interact. We act as a proactive guardian to ensure your filings remain accurate and optimized.

Determining Tax Residency and Tie-Breaker Rules

Residency is the foundation of tax liability for both the CRA and the IRS. Before you can apply treaty benefits, you must first establish where you are considered a resident for tax purposes. For CRA filers, residency is typically determined by the strength of your residential ties to Canada, such as owning a home, having a spouse or dependents in the country, or maintaining social and economic connections. Under IRS rules, the criteria are different. The US determines residency based on citizenship, green card status, or the Substantial Presence Test. When both countries claim an individual as a resident under their domestic laws, the resulting dual residency can lead to significant confusion and potential overpayment.

The IRS Substantial Presence Test

The Substantial Presence Test is a formulaic approach used by the IRS to determine if a non-citizen has spent enough time in the US to be taxed as a resident. It calculates a weighted average of days spent in the US over a three-year period. This includes all days in the current year, one-third of the days in the previous year, and one-sixth of the days in the year before that. If this total reaches 183 days or more, you are generally considered a US resident for tax purposes. Because these rules are rigid, you should verify current day-count thresholds directly with the IRS. If you meet the test but have spent fewer than 183 days in the US during the current calendar year, you may be able to file for a Closer Connection Exception to maintain your status as a non-resident for US tax purposes.

Applying Treaty Tie-Breaker Rules

When dual residency occurs, the United States-Canada Income Tax Convention provides a hierarchical set of tie-breaker rules. These rules are essential to avoid double taxation US Canada because they assign a single country of residency for treaty purposes. The hierarchy begins with your permanent home. If you have a home available in both countries, the focus shifts to your centre of vital interests. This technical term refers to the place where your personal and economic ties are strongest, including your place of work, family location, and where you manage your finances. If the centre of vital interests cannot be determined, the rules look to your habitual abode, which is where you spend the majority of your time, and finally to your nationality. If you find yourself navigating these complex residency definitions, connecting with a cross-border specialist can help ensure your status is correctly identified and documented.

Mechanisms for Relief: Foreign Tax Credits and Exclusions

Foreign Tax Credits (FTCs) represent the most effective tool to realize treaty benefits and protect your hard-earned income. The general principle is that tax paid to one country acts as a dollar-for-dollar credit against tax owed to the other on the same income. This prevents your earnings from being unfairly diminished by two separate authorities. However, these credits are typically limited to the amount of tax that would have been paid on that income locally. You cannot use a high Canadian tax rate to wipe out US tax on unrelated domestic income. Properly organizing your documentation, including copies of foreign tax assessments and proof of payment, is essential for claiming these credits successfully. Without a methodical approach to record-keeping, you may find your claims for relief scrutinized or denied.

Claiming Credits with the IRS

Individuals filing under IRS rules typically use Form 1116 to claim a credit for Canadian taxes paid on various types of income. A critical decision involves choosing between the "paid" and "accrual" methods. The paid method allows you to claim credits in the year you actually pay the tax, while the accrual method lets you claim them in the year the tax liability arises. This distinction is vital for matching tax years between the two countries, as Canada and the US operate on different schedules. The U.S.-Canada Income Tax Treaty guidelines also reference the Foreign Earned Income Exclusion (FEIE). By filing Form 2555, US citizens living in Canada can exclude a portion of their foreign earnings from US taxation, provided they meet specific residency requirements. Choosing the right mechanism is the only way to avoid double taxation US Canada effectively.

Claiming Credits with the CRA

For CRA filers, relief is sought through Form T2209, known as the Federal Foreign Tax Credit, along with corresponding provincial forms. Canadian credits are applied only after any treaty-based withholding reductions are taken into account. For example, if the treaty reduces a US withholding rate on interest to 0%, you cannot claim a credit for US tax that was withheld in error. You must first seek a refund from the IRS for the over-withheld amount. This requires a precise understanding of which country has the primary taxing right over each income stream. Because of these intricate requirements, specialized individual tax return preparation is a prudent step. We help you navigate these forms to ensure that every available credit is captured and your global tax bill is legally minimized.

Treaty Rules for Specific Income Types

The treaty is not a blanket policy that applies equally to every dollar you earn. It is a collection of specific articles, each governing a different type of income stream. This granular approach is exactly how you avoid double taxation US Canada while ensuring you remain compliant with both jurisdictions. Precision is paramount here. A mistake in how you categorize a dividend versus a pension payment can lead to over-withholding that is difficult to recover. You must identify the specific article of the treaty that applies to your unique financial situation to realize the full benefits of the convention.

Employment income also has its own set of thresholds. Under certain conditions, your earnings might be exempt from tax in the country where the work was performed. This usually depends on the length of your stay and the total amount earned during the tax year. However, these rules are complex and often interact with state or provincial laws that may not follow the federal treaty. Always verify your specific circumstances before assuming an exemption applies to your paycheck.

Dividends, Interest, and Royalties

Passive income is frequently subject to high default withholding rates. Under IRS rules, the standard withholding tax on US-source income paid to non-residents is 30%. The treaty significantly reduces this burden, typically lowering the rate to 15% for dividends and 0% for interest paid between arm's-length parties. To claim these reduced rates, Canadian residents must provide the US payer with a completed Form W-8BEN before any payments are made. If you do not have the required identification for these forms, using an ITIN application service Canada can help you obtain a US tax ID efficiently. This proactive step ensures that the correct amount of tax is withheld at the source, preventing the need for complex refund claims later.

Pensions and RRSPs

Retirement savings receive special consideration under the treaty framework. For IRS purposes, Canadian Registered Retirement Savings Plans (RRSPs) and Registered Retirement Income Funds (RRIFs) are generally recognized as tax-deferred pension plans. This means that the growth within these accounts is not taxed annually by the US, provided the accounts meet treaty requirements. Social Security benefits are also subject to unique "source country" rules. For example, if a Canadian resident receives US Social Security, only 85% of that benefit is included in their taxable income for CRA filers. You should realize, however, that lump-sum pension distributions often fall under different rules than periodic payments. These one-time withdrawals can trigger higher withholding rates or immediate tax liabilities if not structured correctly. To protect your retirement nest egg from unnecessary dual taxation, speak with our cross-border specialists today for a personalized compliance review.

Achieving Cross-Border Compliance with Tax Partners

Managing your financial obligations across the 49th parallel is a delicate balancing act. While the treaty provides the legal framework to avoid double taxation US Canada, the actual execution of these rules is where many taxpayers encounter significant risks. Cross-border tax is not a project you should tackle on your own. A single error in form selection or a missed deadline under IRS rules can trigger heavy penalties or the very double taxation you are trying to prevent. We provide a seamless, integrated solution by offering both US tax services and Canadian tax services under one roof. This unified approach ensures that your CRA filings and IRS returns are perfectly synchronized.

Our team specializes in the complexities of 1040 tax filing for Canadians. We don't just fill out forms; we act as a proactive guardian for your wealth. By analyzing your global income through the lens of both jurisdictions, we identify potential issues before either the CRA or the IRS flags your return for review. This foresight allows you to move forward with total confidence in your compliance status.

FBAR and FATCA: Beyond Just Income Tax

If you're a US citizen or green card holder living in Canada, your reporting obligations extend far beyond just your annual income tax return. You're required to report foreign financial accounts if their aggregate value exceeds certain thresholds at any time during the year. This is done through the FBAR (Foreign Bank and Financial Accounts Report), also known as FinCEN Form 114. You can find detailed steps in our guide on FBAR filing requirements. Additionally, the Foreign Account Tax Compliance Act (FATCA) requires reporting on Form 8938 for IRS filers with significant foreign assets. While these two reports overlap, they have different filing thresholds and deadlines that you must monitor closely to avoid draconian penalties.

The Streamlined Filing Procedure

It's common for taxpayers to be genuinely unaware of their US filing obligations while living in Canada. If you've fallen behind, the IRS offers a program called the Streamlined Filing Compliance Procedures. This path allows eligible taxpayers to catch up on their filings and avoid double taxation US Canada without facing the standard non-willful penalties. We've helped countless individuals navigate The IRS Streamlined Procedure for US Expats to regain their standing with the IRS. Our methodical process leads you from uncertainty toward a state of total control, ensuring your cross-border journey remains secure and predictable.

Secure Your Cross-Border Financial Future

Navigating the intersection of two complex tax systems requires more than just filling out forms; it demands a strategic vision for your global assets. By correctly applying the residency tie-breaker rules and leveraging Foreign Tax Credits, you can effectively avoid double taxation US Canada while staying fully compliant with the law. Whether you're managing retirement savings in an RRSP or reporting foreign accounts under IRS rules, precision is the key to protecting your wealth from unnecessary erosion.

At Tax Partners, we bring over 40 years of institutional wisdom to every return we file. With more than 1,390 five-star Google reviews and deep-seated expertise in both CRA and IRS regulations, we act as your proactive guardian on both sides of the border. Don't leave your financial stability to chance. Contact Tax Partners today for a professional cross-border tax consultation to ensure your filings are optimized for 2026 and beyond. You've worked hard for your success, and we're here to ensure you keep more of what you earn.

Frequently Asked Questions

Do I have to file a US tax return if I live in Canada?

Yes, you must file a US tax return if you are a US citizen or resident alien, regardless of where you live in the world. The United States employs a citizenship-based taxation system, which means your global income is subject to IRS rules even if you are a permanent resident of Canada. Most individuals will file Form 1040 annually to report their earnings and claim any applicable treaty benefits.

Can the Canada-US Tax Treaty eliminate my tax bill entirely?

The treaty can often reduce your tax liability to zero through credits and exclusions, but it never eliminates your legal obligation to file. By using mechanisms like the Foreign Tax Credit, you can effectively avoid double taxation US Canada by applying the taxes you paid to the CRA as a credit against what you owe the IRS. While you might not owe a dollar in the end, the paperwork remains a mandatory requirement for compliance.

What is the "Closer Connection" exception for IRS filers?

The Closer Connection exception is a way for individuals who meet the Substantial Presence Test to maintain their status as non-residents for US tax purposes. If you spent a significant amount of time in the US but still have stronger social and economic ties to Canada, you may qualify. You should verify the current day-count thresholds and specific filing requirements directly with the IRS to ensure you meet the criteria for this exception.

How do I avoid paying tax on my Canadian RRSP to the IRS?

You can generally avoid annual US tax on the growth within your RRSP because the treaty recognizes these accounts as tax-deferred pension plans. Under IRS rules, the income earned inside the plan is not taxed until you begin making withdrawals. This protection allows your retirement savings to grow without being diminished by dual taxation, provided the account is properly disclosed on your annual filings.

What happens if I forget to file an FBAR while living in Canada?

Forgetting to file an FBAR can lead to significant financial penalties, though the IRS offers pathways for taxpayers to correct these errors. If your failure to file was non-willful, you may be eligible for the Streamlined Filing Compliance Procedures. This program is a vital tool to help you avoid double taxation US Canada and resolve past-due reporting requirements without facing the most severe draconian penalties.

Does the treaty cover state or provincial taxes?

No, the Canada-US Tax Treaty applies specifically to federal income taxes and does not automatically cover state or provincial jurisdictions. While most Canadian provinces follow the federal lead, some US states do not recognize treaty provisions. This can result in a situation where you owe state-level tax even if you are exempt at the federal level under IRS rules. You should confirm the specific rules for the state or province where your income is sourced.

How do I claim a reduced withholding rate on US dividends?

You claim a reduced withholding rate by providing a completed Form W-8BEN to the US person or institution paying the dividends. This form notifies the payer that you are a resident of Canada and are eligible for the lower treaty rate, which is typically 15 percent instead of the standard 30 percent. Ensuring this form is on file before a payment is made is the most efficient way to manage your cross-border investment income.

Is a Canadian TFSA tax-free in the United States?

No, the IRS does not recognize the Tax-Free Savings Account (TFSA) as a tax-exempt vehicle, meaning its earnings are taxable for US persons. Unlike the RRSP, the TFSA is not protected by the pension provisions of the treaty. For CRA filers who are also US citizens, this often means that the "tax-free" benefits of the account are lost to US federal tax obligations on the annual gains and dividends.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

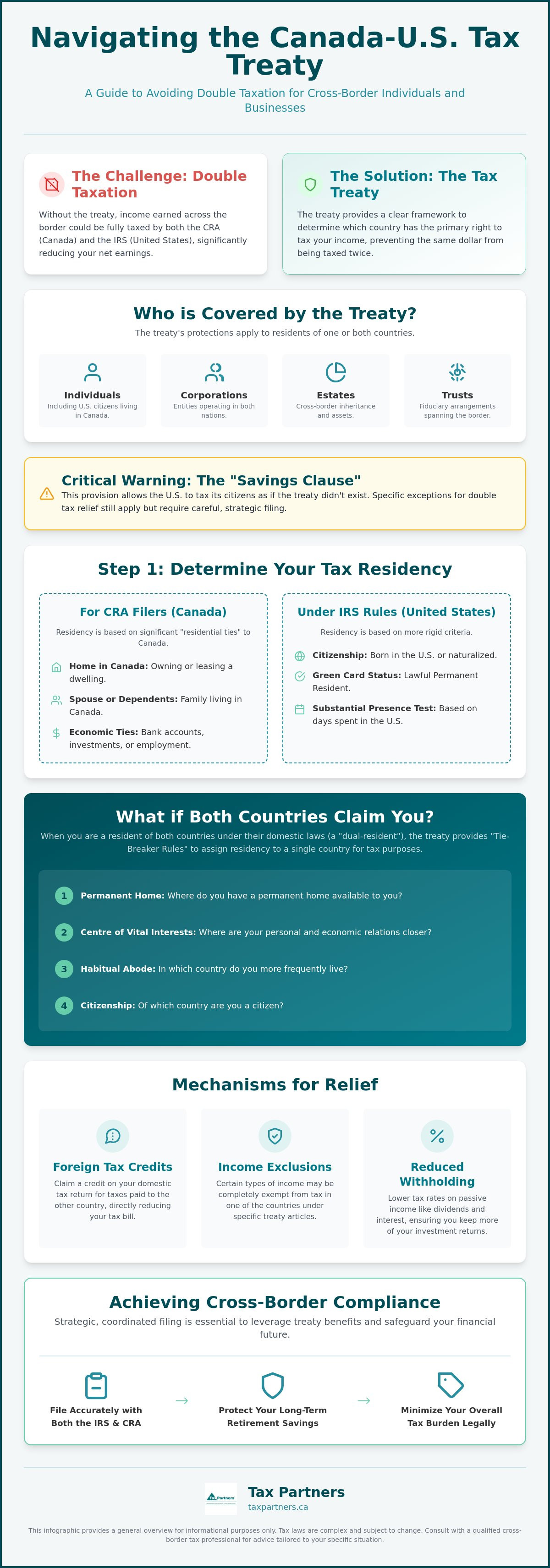

Who is Covered by the Treaty?

The treaty applies broadly to residents of Canada, the United States, or individuals who hold residency in both nations simultaneously. This coverage extends beyond just individuals; it includes corporations, estates, and trusts. It's particularly vital for US citizens living in Canada. Because the US taxes its citizens on their global income regardless of where they live, these individuals often find themselves caught between two jurisdictions. The treaty provides the necessary mechanisms to ensure that the IRS and CRA don't both take a full share of the same income. It helps you realize the full potential of your earnings without unnecessary loss to dual taxation.

The Savings Clause: A Critical Warning

Despite the protections offered, the treaty contains a provision known as the Savings Clause. This clause essentially allows the US to tax its citizens as if the treaty did not exist. It's a significant hurdle that can catch the unwary off guard. However, there are specific exceptions to this clause that still allow for double tax relief through credits and exemptions. Because these rules are intricate, navigating them requires a precise approach. Relying on professional US tax services or specialized Canadian tax services is the best way to ensure you don't fall victim to these complex overlaps. Protecting your wealth requires foresight and a deep understanding of how these two systems interact. We act as a proactive guardian to ensure your filings remain accurate and optimized. Residency is the foundation of tax liability for both the CRA and the IRS. Before you can apply treaty benefits, you must first establish where you are considered a resident for tax purposes. For CRA filers, residency is typically determined by the strength of your residential ties to Canada, such as owning a home, having a spouse or dependents in the country, or maintaining social and economic connections. Under IRS rules, the criteria are different. The US determines residency based on citizenship, green card status, or the Substantial Presence Test. When both countries claim an individual as a resident under their domestic laws, the resulting dual residency can lead to significant confusion and potential overpayment.

The IRS Substantial Presence Test

The Substantial Presence Test is a formulaic approach used by the IRS to determine if a non-citizen has spent enough time in the US to be taxed as a resident. It calculates a weighted average of days spent in the US over a three-year period. This includes all days in the current year, one-third of the days in the previous year, and one-sixth of the days in the year before that. If this total reaches 183 days or more, you are generally considered a US resident for tax purposes. Because these rules are rigid, you should verify current day-count thresholds directly with the IRS. If you meet the test but have spent fewer than 183 days in the US during the current calendar year, you may be able to file for a Closer Connection Exception to maintain your status as a non-resident for US tax purposes.

Applying Treaty Tie-Breaker Rules

When dual residency occurs, the United States-Canada Income Tax Convention provides a hierarchical set of tie-breaker rules. These rules are essential to avoid double taxation US Canada because they assign a single country of residency for treaty purposes. The hierarchy begins with your permanent home. If you have a home available in both countries, the focus shifts to your centre of vital interests. This technical term refers to the place where your personal and economic ties are strongest, including your place of work, family location, and where you manage your finances. If the centre of vital interests cannot be determined, the rules look to your habitual abode, which is where you spend the majority of your time, and finally to your nationality. If you find yourself navigating these complex residency definitions, connecting with a cross-border specialist can help ensure your status is correctly identified and documented. Foreign Tax Credits (FTCs) represent the most effective tool to realize treaty benefits and protect your hard-earned income. The general principle is that tax paid to one country acts as a dollar-for-dollar credit against tax owed to the other on the same income. This prevents your earnings from being unfairly diminished by two separate authorities. However, these credits are typically limited to the amount of tax that would have been paid on that income locally. You cannot use a high Canadian tax rate to wipe out US tax on unrelated domestic income. Properly organizing your documentation, including copies of foreign tax assessments and proof of payment, is essential for claiming these credits successfully. Without a methodical approach to record-keeping, you may find your claims for relief scrutinized or denied.

Claiming Credits with the IRS

Individuals filing under IRS rules typically use Form 1116 to claim a credit for Canadian taxes paid on various types of income. A critical decision involves choosing between the "paid" and "accrual" methods. The paid method allows you to claim credits in the year you actually pay the tax, while the accrual method lets you claim them in the year the tax liability arises. This distinction is vital for matching tax years between the two countries, as Canada and the US operate on different schedules. The U.S.-Canada Income Tax Treaty guidelines also reference the Foreign Earned Income Exclusion (FEIE). By filing Form 2555, US citizens living in Canada can exclude a portion of their foreign earnings from US taxation, provided they meet specific residency requirements. Choosing the right mechanism is the only way to avoid double taxation US Canada effectively.

Claiming Credits with the CRA

For CRA filers, relief is sought through Form T2209, known as the Federal Foreign Tax Credit, along with corresponding provincial forms. Canadian credits are applied only after any treaty-based withholding reductions are taken into account. For example, if the treaty reduces a US withholding rate on interest to 0%, you cannot claim a credit for US tax that was withheld in error. You must first seek a refund from the IRS for the over-withheld amount. This requires a precise understanding of which country has the primary taxing right over each income stream. Because of these intricate requirements, specialized individual tax return preparation is a prudent step. We help you navigate these forms to ensure that every available credit is captured and your global tax bill is legally minimized. The treaty is not a blanket policy that applies equally to every dollar you earn. It is a collection of specific articles, each governing a different type of income stream. This granular approach is exactly how you avoid double taxation US Canada while ensuring you remain compliant with both jurisdictions. Precision is paramount here. A mistake in how you categorize a dividend versus a pension payment can lead to over-withholding that is difficult to recover. You must identify the specific article of the treaty that applies to your unique financial situation to realize the full benefits of the convention. Employment income also has its own set of thresholds. Under certain conditions, your earnings might be exempt from tax in the country where the work was performed. This usually depends on the length of your stay and the total amount earned during the tax year. However, these rules are complex and often interact with state or provincial laws that may not follow the federal treaty. Always verify your specific circumstances before assuming an exemption applies to your paycheck.

Dividends, Interest, and Royalties

Passive income is frequently subject to high default withholding rates. Under IRS rules, the standard withholding tax on US-source income paid to non-residents is 30%. The treaty significantly reduces this burden, typically lowering the rate to 15% for dividends and 0% for interest paid between arm's-length parties. To claim these reduced rates, Canadian residents must provide the US payer with a completed Form W-8BEN before any payments are made. If you do not have the required identification for these forms, using an ITIN application service Canada can help you obtain a US tax ID efficiently. This proactive step ensures that the correct amount of tax is withheld at the source, preventing the need for complex refund claims later.

Pensions and RRSPs

Retirement savings receive special consideration under the treaty framework. For IRS purposes, Canadian Registered Retirement Savings Plans (RRSPs) and Registered Retirement Income Funds (RRIFs) are generally recognized as tax-deferred pension plans. This means that the growth within these accounts is not taxed annually by the US, provided the accounts meet treaty requirements. Social Security benefits are also subject to unique "source country" rules. For example, if a Canadian resident receives US Social Security, only 85% of that benefit is included in their taxable income for CRA filers. You should realize, however, that lump-sum pension distributions often fall under different rules than periodic payments. These one-time withdrawals can trigger higher withholding rates or immediate tax liabilities if not structured correctly. To protect your retirement nest egg from unnecessary dual taxation, speak with our cross-border specialists today for a personalized compliance review. Managing your financial obligations across the 49th parallel is a delicate balancing act. While the treaty provides the legal framework to avoid double taxation US Canada, the actual execution of these rules is where many taxpayers encounter significant risks. Cross-border tax is not a project you should tackle on your own. A single error in form selection or a missed deadline under IRS rules can trigger heavy penalties or the very double taxation you are trying to prevent. We provide a seamless, integrated solution by offering both US tax services and Canadian tax services under one roof. This unified approach ensures that your CRA filings and IRS returns are perfectly synchronized. Our team specializes in the complexities of 1040 tax filing for Canadians. We don't just fill out forms; we act as a proactive guardian for your wealth. By analyzing your global income through the lens of both jurisdictions, we identify potential issues before either the CRA or the IRS flags your return for review. This foresight allows you to move forward with total confidence in your compliance status.

FBAR and FATCA: Beyond Just Income Tax

If you're a US citizen or green card holder living in Canada, your reporting obligations extend far beyond just your annual income tax return. You're required to report foreign financial accounts if their aggregate value exceeds certain thresholds at any time during the year. This is done through the FBAR (Foreign Bank and Financial Accounts Report), also known as FinCEN Form 114. You can find detailed steps in our guide on FBAR filing requirements. Additionally, the Foreign Account Tax Compliance Act (FATCA) requires reporting on Form 8938 for IRS filers with significant foreign assets. While these two reports overlap, they have different filing thresholds and deadlines that you must monitor closely to avoid draconian penalties.

The Streamlined Filing Procedure

It's common for taxpayers to be genuinely unaware of their US filing obligations while living in Canada. If you've fallen behind, the IRS offers a program called the Streamlined Filing Compliance Procedures. This path allows eligible taxpayers to catch up on their filings and avoid double taxation US Canada without facing the standard non-willful penalties. We've helped countless individuals navigate The IRS Streamlined Procedure for US Expats to regain their standing with the IRS. Our methodical process leads you from uncertainty toward a state of total control, ensuring your cross-border journey remains secure and predictable. Navigating the intersection of two complex tax systems requires more than just filling out forms; it demands a strategic vision for your global assets. By correctly applying the residency tie-breaker rules and leveraging Foreign Tax Credits, you can effectively avoid double taxation US Canada while staying fully compliant with the law. Whether you're managing retirement savings in an RRSP or reporting foreign accounts under IRS rules, precision is the key to protecting your wealth from unnecessary erosion. At Tax Partners, we bring over 40 years of institutional wisdom to every return we file. With more than 1,390 five-star Google reviews and deep-seated expertise in both CRA and IRS regulations, we act as your proactive guardian on both sides of the border. Don't leave your financial stability to chance. Contact Tax Partners today for a professional cross-border tax consultation to ensure your filings are optimized for 2026 and beyond. You've worked hard for your success, and we're here to ensure you keep more of what you earn.

Do I have to file a US tax return if I live in Canada?

Yes, you must file a US tax return if you are a US citizen or resident alien, regardless of where you live in the world. The United States employs a citizenship-based taxation system, which means your global income is subject to IRS rules even if you are a permanent resident of Canada. Most individuals will file Form 1040 annually to report their earnings and claim any applicable treaty benefits.

Can the Canada-US Tax Treaty eliminate my tax bill entirely?

The treaty can often reduce your tax liability to zero through credits and exclusions, but it never eliminates your legal obligation to file. By using mechanisms like the Foreign Tax Credit, you can effectively avoid double taxation US Canada by applying the taxes you paid to the CRA as a credit against what you owe the IRS. While you might not owe a dollar in the end, the paperwork remains a mandatory requirement for compliance.

What is the "Closer Connection" exception for IRS filers?

The Closer Connection exception is a way for individuals who meet the Substantial Presence Test to maintain their status as non-residents for US tax purposes. If you spent a significant amount of time in the US but still have stronger social and economic ties to Canada, you may qualify. You should verify the current day-count thresholds and specific filing requirements directly with the IRS to ensure you meet the criteria for this exception.

How do I avoid paying tax on my Canadian RRSP to the IRS?

You can generally avoid annual US tax on the growth within your RRSP because the treaty recognizes these accounts as tax-deferred pension plans. Under IRS rules, the income earned inside the plan is not taxed until you begin making withdrawals. This protection allows your retirement savings to grow without being diminished by dual taxation, provided the account is properly disclosed on your annual filings.

What happens if I forget to file an FBAR while living in Canada?

Forgetting to file an FBAR can lead to significant financial penalties, though the IRS offers pathways for taxpayers to correct these errors. If your failure to file was non-willful, you may be eligible for the Streamlined Filing Compliance Procedures. This program is a vital tool to help you avoid double taxation US Canada and resolve past-due reporting requirements without facing the most severe draconian penalties.

Does the treaty cover state or provincial taxes?

No, the Canada-US Tax Treaty applies specifically to federal income taxes and does not automatically cover state or provincial jurisdictions. While most Canadian provinces follow the federal lead, some US states do not recognize treaty provisions. This can result in a situation where you owe state-level tax even if you are exempt at the federal level under IRS rules. You should confirm the specific rules for the state or province where your income is sourced.

How do I claim a reduced withholding rate on US dividends?

You claim a reduced withholding rate by providing a completed Form W-8BEN to the US person or institution paying the dividends. This form notifies the payer that you are a resident of Canada and are eligible for the lower treaty rate, which is typically 15 percent instead of the standard 30 percent. Ensuring this form is on file before a payment is made is the most efficient way to manage your cross-border investment income.

Is a Canadian TFSA tax-free in the United States?

No, the IRS does not recognize the Tax-Free Savings Account (TFSA) as a tax-exempt vehicle, meaning its earnings are taxable for US persons. Unlike the RRSP, the TFSA is not protected by the pension provisions of the treaty. For CRA filers who are also US citizens, this often means that the "tax-free" benefits of the account are lost to US federal tax obligations on the annual gains and dividends.