Tax-Efficient Wealth Management for CRA Filers: A 2026 Strategic Guide

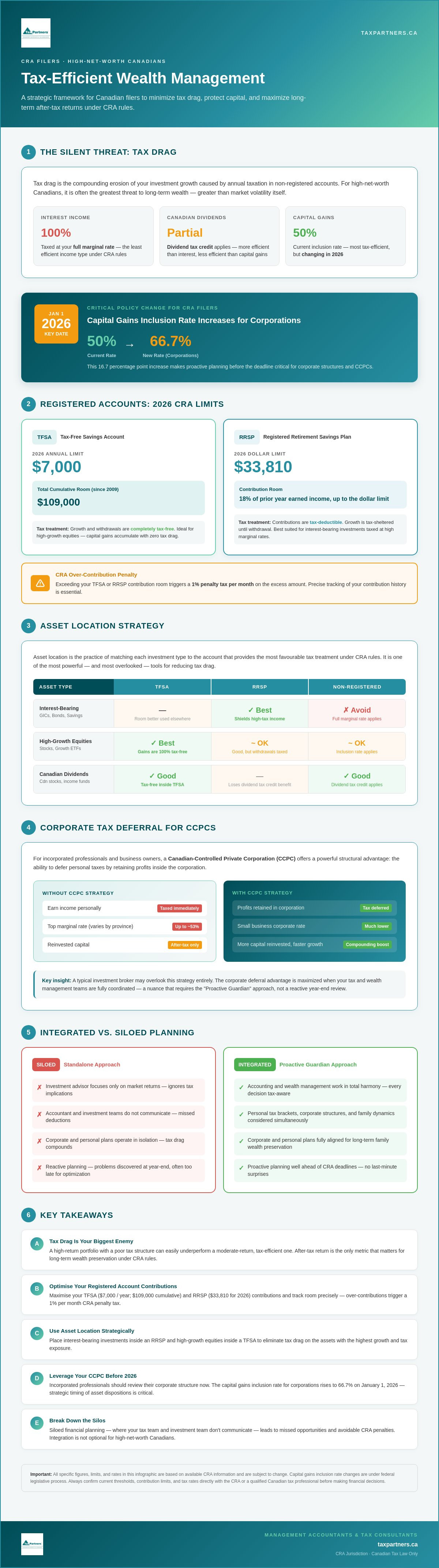

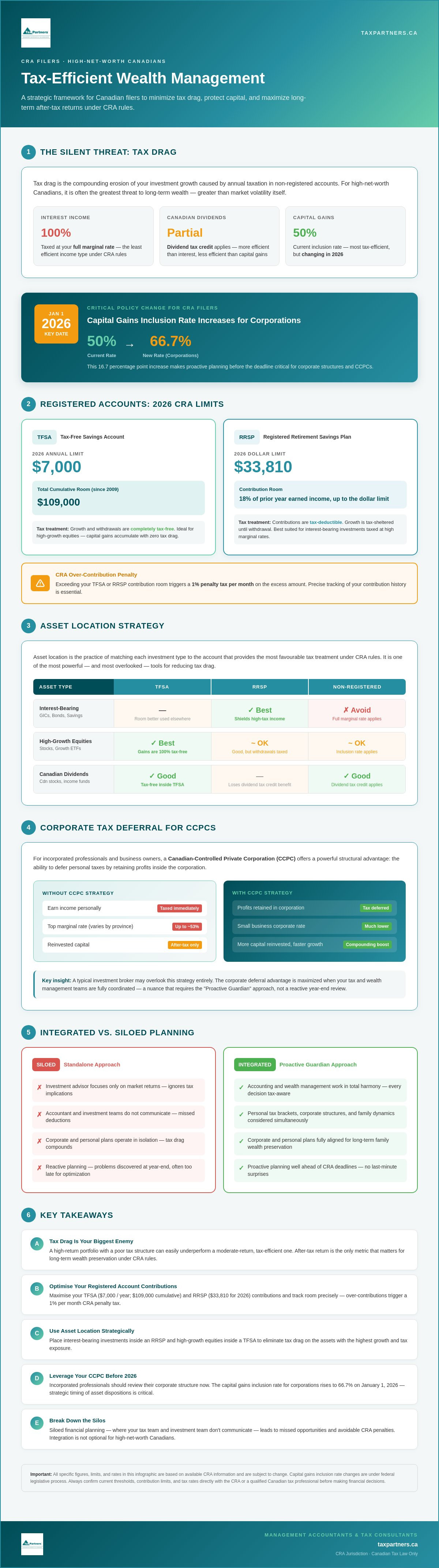

For high-net-worth Canadians, the most significant threat to your portfolio isn't market volatility; it's the silent, compounding erosion caused by tax drag. You've likely spent years building your capital, yet you now face the frustration of watching a substantial portion of your returns disappear before they can even be reinvested. Implementing a strategy for tax efficient wealth management for CRA filers is no longer optional; it's a necessity, especially with the capital gains inclusion rate scheduled to increase to 66.7 percent for corporations on January 1, 2026.

We understand the complexity of trying to balance corporate distributions with personal growth while staying ahead of the CRA. This guide offers a clear framework to minimize your tax liability and preserve your hard-earned capital. You'll learn how to integrate your personal and corporate plans to ensure every dollar works toward your family's long-term security. We'll examine the 2026 federal tax brackets, new RRSP and TFSA limits, and the strategic timing of asset sales to help you regain total control over your financial future.

Key Takeaways

- Understand how tax efficient wealth management minimizes "tax drag" by strategically arranging your assets to reduce the impact of annual taxation under CRA rules.

- Discover how to optimize your registered accounts through precise asset location, ensuring each investment is held in the most tax-advantageous environment.

- Learn the mechanics of corporate tax deferral for CCPCs and how leaving profits inside your corporation can significantly enhance your long-term capital growth.

- Recognize the dangers of siloed financial planning and why integrated communication between your tax and investment teams is vital for avoiding unnecessary CRA penalties.

- Gain a clear framework for aligning your corporate and personal financial goals to secure a stable and resilient legacy for your family.

Defining Tax-Efficient Wealth Management for CRA Filers

Tax efficient wealth management for CRA filers is the deliberate, strategic arrangement of your financial assets to minimize the impact of "tax drag." In the Canadian context, this means looking beyond simple investment returns and focusing on how much you actually keep after the Canada Revenue Agency (CRA) takes its share. It is essential to distinguish this from tax evasion, which is the illegal non-payment or underpayment of taxes. Conversely, tax avoidance and optimization are legal, encouraged methods of planning that use the existing framework of the Income Tax Act to your advantage. True efficiency requires an integrated approach where your accounting and wealth management and financial planning work in total harmony.

The Concept of Tax Drag on Investment Returns

Tax drag is the silent reduction in your potential investment growth caused by annual taxation. Every time you receive interest, a dividend, or realize a capital gain in a non-registered account, a portion of that growth is diverted to the CRA. Under CRA rules, interest income is generally taxed at your full marginal rate, while Canadian dividends receive a tax credit. Capital gains currently benefit from a 50 percent inclusion rate, though this is scheduled to change for many filers on January 1, 2026. Because of these varying rates, a high-return portfolio with poor tax structure can easily underperform a moderate-return, tax-efficient portfolio. The only metric that truly impacts your long-term wealth preservation is your after-tax return. Utilizing tools like a Tax-Free Savings Account (TFSA) allows you to eliminate tax drag entirely on specific assets, providing a powerful boost to your compounding growth.

Why Integrated Planning Outperforms Simple Investing

Many investors rely on a standalone investment advisor who focuses solely on market performance. This often leads to missed opportunities. A comprehensive tax efficient wealth management strategy considers your personal tax brackets, corporate structures, and family dynamics simultaneously. For example, an incorporated professional might benefit from leaving profits inside a Canadian-Controlled Private Corporation (CCPC) to defer personal taxes, a nuance a typical investment broker might overlook. At Tax Partners, we employ a "Proactive Guardian" approach. This means we don't just react to your year-end numbers. We look ahead to secure better outcomes by aligning your corporate and personal plans well before CRA deadlines arrive. This ensures your wealth strategy is robust, compliant, and optimized for the long term.

Leveraging Registered Accounts for Long-Term Wealth Preservation

Registered accounts are the structural pillars of tax efficient wealth management for CRA filers. They aren't just savings buckets; they're sophisticated tools that allow you to shield your growth from the immediate reach of the tax collector. A truly effective strategy relies on "asset location." This is the practice of matching specific investments to the account type that offers the best tax treatment. For example, interest-bearing investments that are taxed at high marginal rates are often best suited for an RRSP, while high-growth equities might be better placed in a TFSA to ensure their capital gains remain entirely tax-free.

Managing these accounts requires meticulous attention to CRA contribution limits. In 2026, the annual TFSA contribution limit is $7,000, bringing the total cumulative room to $109,000 for those eligible since 2009. Meanwhile, the RRSP dollar limit for 2026 has reached $33,810. Over-contributing to these plans can lead to a penalty tax of 1 percent per month on the excess amount. Precision matters. We help our clients track these rooms with certainty to avoid unnecessary friction with the CRA. If you're unsure how these limits apply to your specific situation, you can always speak with our team for a detailed review of your contribution history.

RRSPs and TFSAs: The Foundation of Canadian Tax Efficiency

The Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA) offer opposing but complementary benefits. RRSP contributions provide an immediate tax deduction, which is particularly valuable if you're currently in a high tax bracket. However, these funds are fully taxable when you eventually withdraw them. Conversely, the TFSA uses after-tax dollars but allows for entirely tax-free growth and withdrawals. Deciding which to prioritize depends on your current income versus your expected income in retirement. You can find a complete list of Canadian registered savings plans on the official government website to see which structures might fit your broader goals.

The First-Home Savings Account (FHSA) in a Wealth Strategy

The First-Home Savings Account (FHSA) has quickly become a "hybrid" powerhouse in Canadian wealth planning. It combines the best features of its predecessors: the tax-deductible contributions of an RRSP and the tax-free withdrawals of a TFSA. For high-net-worth parents or grandparents, the FHSA serves as an exceptional intergenerational wealth transfer tool. By gifting funds to adult children to maximize their FHSA room, families can facilitate a tax-free down payment for a first home. Under CRA rules, if the home isn't purchased within 15 years, the funds can be transferred to an RRSP without affecting existing contribution room. This ensures the capital continues to grow in a tax-sheltered environment regardless of the child's immediate real estate plans.

Strategic Income Planning for Business Owners and Professionals

For those operating through a Canadian-Controlled Private Corporation (CCPC), tax efficient wealth management is fundamentally about timing. You aren't just managing money; you're managing the friction between corporate and personal tax regimes. The primary advantage of a CCPC is the ability to defer personal income tax by leaving profits within the company. In 2026, the federal small business tax rate remains at 9 percent on the first $500,000 of active business income. By retaining earnings, you can reinvest more capital today than if you had immediately paid yourself and faced personal tax rates as high as 33 percent at the federal level.

This deferral strategy requires careful navigation of CRA passive income rules. If your corporation generates more than $50,000 in passive investment income annually, your access to the small business deduction begins to phase out. It's fully eliminated once passive income reaches $150,000. This is where a holistic accounting strategy becomes vital. We look at your total asset footprint to ensure your corporate investments don't inadvertently trigger higher tax rates on your active business earnings. We also help you navigate family income splitting within the current CRA legislative framework, ensuring compliance with Tax on Split Income (TOSI) rules while still optimizing your family's overall tax position.

The Salary vs. Dividend Decision for CRA Compliance

Choosing between salary and dividends is a core component of your annual planning. Employment income (salary) is a deductible expense for your corporation and creates valuable RRSP contribution room. It also requires contributions to the Canada Pension Plan (CPP), which provides a base level of retirement security. Dividends, on the other hand, are paid from after-tax corporate profits. While they don't create RRSP room or require CPP contributions, they are often taxed at a lower personal rate due to the dividend tax credit. The "best" mix isn't a static formula. It must align with your current cash flow needs and your 2026 contribution goals for the registered accounts we discussed previously.

Utilizing Holding Companies for Tax Deferral

A holding company can act as a powerful reservoir for your long-term wealth. It provides an extra layer of asset protection and allows you to move funds from an operating company via inter-corporate dividends. Under specific CRA conditions, these transfers can often occur tax-free, allowing you to accumulate wealth for future investment or estate planning without triggering immediate personal tax. If you're looking to refine your corporate architecture, our team at Tax Partners business solutions can help you design a structure that maximizes these deferral opportunities while ensuring full CRA compliance.

Avoiding Common Tax Planning Pitfalls in Canada

Even the most robust investment plan can falter if it isn't viewed through a tax lens. One of the most pervasive pitfalls we see is "siloed" planning. This occurs when your investment advisor and your accountant operate in isolation. Without a unified strategy for tax efficient wealth management, you risk incurring unnecessary CRA interest and penalties. For instance, chasing high-yield investments in a non-registered account can be a tax disaster for high-income earners. The interest is taxed at your full marginal rate, which in 2026 reaches 33 percent federally for income over $258,482. This effectively wipes out a significant portion of your gains before you've even had a chance to reinvest.

Digital assets present another hurdle. If you hold cryptocurrency, the CRA expects meticulous record-keeping. Failing to track the adjusted cost base (ACB) of each transaction can lead to severe audit headaches or penalties. Furthermore, if your foreign-held digital assets exceed certain cost thresholds, you may be required to file Form T1135. If you're managing complex digital portfolios, you should connect with our tax specialists to ensure your reporting is accurate and your structures are optimized for 2026 compliance.

Misunderstanding Capital Gains and Dividend Tax Credits

Capital gains remain a preferred form of income for CRA filers because of the inclusion rate. However, you must plan for the changes taking effect on January 1, 2026. For individuals, the inclusion rate increases to 66.7 percent only on net capital gains realized annually above a $250,000 threshold. For corporations, this higher rate applies to all gains. Many filers also find the "gross-up" and tax credit mechanism for Canadian dividends confusing. It's vital to distinguish between "eligible" dividends from large corporations and "non-eligible" dividends from small businesses. Assuming they're taxed the same can lead to significant errors in your personal cash flow projections.

The Risks of Improper Asset Location

Asset location is the deliberate act of placing high-tax investments, such as interest-bearing bonds, within your registered accounts. A common mistake is holding US-listed dividend stocks inside a TFSA. While the growth is tax-free in Canada, the US government often applies unrecoverable foreign withholding taxes because they don't recognize the TFSA as a retirement account. Conversely, Canadian equities are often better suited for non-registered accounts because they allow you to utilize the dividend tax credit effectively. Strategic placement ensures you aren't leaving money on the table or paying more to the CRA than is legally required.

Building a Resilient Financial Future with Tax Partners

Securing your legacy in a shifting regulatory environment requires more than just a standard accounting service. It demands a partnership built on decades of institutional wisdom and a forward-thinking outlook. For 40 years, Tax Partners has served as a steady hand for Canadian families, helping them navigate the complexities of the Income Tax Act with confidence. By consolidating your bookkeeping, corporate tax, and wealth planning within a single firm, you eliminate the communication gaps that often lead to CRA audits or missed deductions. This integrated approach ensures that your personal and corporate plans are perfectly aligned, providing you with a seamless path toward long-term wealth preservation.

We encourage our clients to move away from reactive, year-end filing and embrace year-round strategic management. When your tax and investment teams work in isolation, you lose the ability to pivot before deadlines arrive. Our comprehensive model allows us to monitor your "tax drag" in real time, adjusting your strategies as market conditions or CRA rules evolve. You gain the peace of mind that comes from knowing every dollar is working toward your family's future, rather than being eroded by inefficient structures or late-stage corrections.

The Proactive Guardian Approach to Wealth

At Tax Partners, we view our role as that of a "proactive guardian." We don't just react to requirements; we actively look ahead to secure better outcomes for your portfolio. This commitment to precision and foresight is woven into our Tax Partners mission and vision, which prioritizes ethical steadfastness and personalized care. Having managed over 495,000 returns, our firm possesses a deep database of CRA knowledge that we leverage to protect your capital. We understand the nuances of the 2026 tax landscape, and we use that expertise to ensure your wealth strategy remains resilient against any legislative changes.

Transitioning from Reactive Filing to Strategic Planning

Preparing for 2026 requires a holistic review of your financial architecture. To begin your journey toward tax efficient wealth management, we recommend preparing a few key items for your initial consultation. Bring your corporate articles of incorporation, your last three years of CRA notices of assessment, and a clear list of your family's long-term objectives. If you're a business owner considering an eventual exit, you should also review Succession Planning for Family Business to understand how to protect your hard-earned value during a transition. We invite you to reach out for a bespoke consultation today. Let us help you organize your financial life and provide the steady guidance you need to thrive in the years ahead.

Secure Your Legacy for 2026 and Beyond

The transition into the 2026 tax year represents a pivotal moment for your financial health. By understanding how to minimize tax drag and strategically locating assets across your registered and corporate accounts, you can protect your capital from unnecessary erosion. We've explored how integrated planning for your corporation ensures that every dividend and salary decision supports your long-term family goals. Achieving true tax efficient wealth management is about more than just compliance; it's about gaining the foresight to act before the CRA's rules impact your returns. Our guidance ensures your personal and corporate plans are always aligned, removing the stress of siloed advice and missed opportunities.

With over 40 years of Canadian tax expertise and 1,390 five-star Google reviews, our team has saved clients more than $87 million in taxes to date. We act as your proactive guardian, providing the stability and precision needed to thrive in a complex regulatory environment. Secure your financial future with Tax Partners' integrated wealth management services. You've worked hard to build your wealth, and we're here to ensure you keep it for generations to come.

Frequently Asked Questions for CRA Filers

What is the most tax-efficient way to invest in Canada?

The most tax-efficient way involves maximizing your registered accounts to eliminate or defer taxation on investment growth. By using structures like the TFSA, your gains remain entirely tax-free; whereas an RRSP provides an immediate deduction to lower your current taxable income. Beyond these accounts, focusing on capital gains rather than interest income in non-registered accounts ensures you benefit from a lower inclusion rate under CRA rules.

How does a holding company help with wealth management under CRA rules?

A holding company allows you to defer personal income taxes by retaining business profits within a corporate structure rather than paying them out as personal income. This strategy facilitates the reinvestment of capital that would otherwise be lost to high personal tax brackets. Additionally, holding companies provide a layer of asset protection and can receive tax-free inter-corporate dividends from an operating company under specific conditions.

Is a TFSA or an RRSP better for high-income professionals?

High-income professionals often find the RRSP more beneficial for immediate tax relief because contributions reduce income taxed at the highest marginal rates. However, a TFSA is an essential component of tax efficient wealth management because it provides flexibility and tax-free withdrawals in retirement. Most successful strategies involve maximizing both accounts to balance current tax savings with long-term, tax-free growth.

Can I split my investment income with my spouse to save on taxes?

You can split investment income, but you must strictly adhere to the CRA's Tax on Split Income (TOSI) rules to avoid high-rate penalties. Common legal methods include using a prescribed rate spousal loan, where one spouse lends money to the other at a CRA-approved interest rate. This allows the lower-income spouse to report the investment returns at their lower tax bracket, effectively reducing the family's total tax bill.

What is the difference between tax-efficient investing and tax-efficient wealth management?

Tax-efficient investing focuses on selecting specific financial products, like corporate class funds, to minimize taxes. In contrast, tax efficient wealth management is a holistic approach that integrates your corporate structure, personal income needs, and family estate planning. It ensures that every part of your financial life, from your bookkeeping to your long-term legacy, is organized to minimize the silent erosion caused by "tax drag."

How often should I review my tax-efficient wealth strategy with a CPA?

You should review your strategy at least once a year during your annual tax planning session. However, significant life events or major legislative shifts, such as the 2026 changes to capital gains inclusion rates, require more frequent consultations. Regular touchpoints with a CPA ensure your plan remains proactive rather than reactive, allowing you to adjust your asset location before the CRA's filing deadlines arrive.

Does the CRA tax capital gains differently than regular income?

The CRA taxes capital gains more favourably than regular interest income by only taxing a portion of the gain, known as the inclusion rate. Currently, this rate is 50 percent, but for many filers, it's scheduled to increase to 66.7 percent on January 1, 2026. This makes capital gains a preferred form of income for many investors compared to interest, which is taxed at your full marginal rate.

What happens if I over-contribute to my registered accounts like the TFSA?

Over-contributing to a TFSA or RRSP triggers a penalty tax of 1 percent per month on the excess amount for as long as it remains in the account. The CRA is very strict regarding these limits, so it's vital to track your contribution room through your official portals or with your accountant. If you discover an over-contribution, you should withdraw the excess funds immediately to stop the monthly penalty from compounding.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

The Concept of Tax Drag on Investment Returns

Tax drag is the silent reduction in your potential investment growth caused by annual taxation. Every time you receive interest, a dividend, or realize a capital gain in a non-registered account, a portion of that growth is diverted to the CRA. Under CRA rules, interest income is generally taxed at your full marginal rate, while Canadian dividends receive a tax credit. Capital gains currently benefit from a 50 percent inclusion rate, though this is scheduled to change for many filers on January 1, 2026. Because of these varying rates, a high-return portfolio with poor tax structure can easily underperform a moderate-return, tax-efficient portfolio. The only metric that truly impacts your long-term wealth preservation is your after-tax return. Utilizing tools like a Tax-Free Savings Account (TFSA) allows you to eliminate tax drag entirely on specific assets, providing a powerful boost to your compounding growth.

Why Integrated Planning Outperforms Simple Investing

Many investors rely on a standalone investment advisor who focuses solely on market performance. This often leads to missed opportunities. A comprehensive tax efficient wealth management strategy considers your personal tax brackets, corporate structures, and family dynamics simultaneously. For example, an incorporated professional might benefit from leaving profits inside a Canadian-Controlled Private Corporation (CCPC) to defer personal taxes, a nuance a typical investment broker might overlook. At Tax Partners, we employ a "Proactive Guardian" approach. This means we don't just react to your year-end numbers. We look ahead to secure better outcomes by aligning your corporate and personal plans well before CRA deadlines arrive. This ensures your wealth strategy is robust, compliant, and optimized for the long term. Registered accounts are the structural pillars of tax efficient wealth management for CRA filers. They aren't just savings buckets; they're sophisticated tools that allow you to shield your growth from the immediate reach of the tax collector. A truly effective strategy relies on "asset location." This is the practice of matching specific investments to the account type that offers the best tax treatment. For example, interest-bearing investments that are taxed at high marginal rates are often best suited for an RRSP, while high-growth equities might be better placed in a TFSA to ensure their capital gains remain entirely tax-free. Managing these accounts requires meticulous attention to CRA contribution limits. In 2026, the annual TFSA contribution limit is $7,000, bringing the total cumulative room to $109,000 for those eligible since 2009. Meanwhile, the RRSP dollar limit for 2026 has reached $33,810. Over-contributing to these plans can lead to a penalty tax of 1 percent per month on the excess amount. Precision matters. We help our clients track these rooms with certainty to avoid unnecessary friction with the CRA. If you're unsure how these limits apply to your specific situation, you can always speak with our team for a detailed review of your contribution history.

RRSPs and TFSAs: The Foundation of Canadian Tax Efficiency

The Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA) offer opposing but complementary benefits. RRSP contributions provide an immediate tax deduction, which is particularly valuable if you're currently in a high tax bracket. However, these funds are fully taxable when you eventually withdraw them. Conversely, the TFSA uses after-tax dollars but allows for entirely tax-free growth and withdrawals. Deciding which to prioritize depends on your current income versus your expected income in retirement. You can find a complete list of Canadian registered savings plans on the official government website to see which structures might fit your broader goals.

The First-Home Savings Account (FHSA) in a Wealth Strategy

The First-Home Savings Account (FHSA) has quickly become a "hybrid" powerhouse in Canadian wealth planning. It combines the best features of its predecessors: the tax-deductible contributions of an RRSP and the tax-free withdrawals of a TFSA. For high-net-worth parents or grandparents, the FHSA serves as an exceptional intergenerational wealth transfer tool. By gifting funds to adult children to maximize their FHSA room, families can facilitate a tax-free down payment for a first home. Under CRA rules, if the home isn't purchased within 15 years, the funds can be transferred to an RRSP without affecting existing contribution room. This ensures the capital continues to grow in a tax-sheltered environment regardless of the child's immediate real estate plans. For those operating through a Canadian-Controlled Private Corporation (CCPC), tax efficient wealth management is fundamentally about timing. You aren't just managing money; you're managing the friction between corporate and personal tax regimes. The primary advantage of a CCPC is the ability to defer personal income tax by leaving profits within the company. In 2026, the federal small business tax rate remains at 9 percent on the first $500,000 of active business income. By retaining earnings, you can reinvest more capital today than if you had immediately paid yourself and faced personal tax rates as high as 33 percent at the federal level. This deferral strategy requires careful navigation of CRA passive income rules. If your corporation generates more than $50,000 in passive investment income annually, your access to the small business deduction begins to phase out. It's fully eliminated once passive income reaches $150,000. This is where a holistic accounting strategy becomes vital. We look at your total asset footprint to ensure your corporate investments don't inadvertently trigger higher tax rates on your active business earnings. We also help you navigate family income splitting within the current CRA legislative framework, ensuring compliance with Tax on Split Income (TOSI) rules while still optimizing your family's overall tax position.

The Salary vs. Dividend Decision for CRA Compliance

Choosing between salary and dividends is a core component of your annual planning. Employment income (salary) is a deductible expense for your corporation and creates valuable RRSP contribution room. It also requires contributions to the Canada Pension Plan (CPP), which provides a base level of retirement security. Dividends, on the other hand, are paid from after-tax corporate profits. While they don't create RRSP room or require CPP contributions, they are often taxed at a lower personal rate due to the dividend tax credit. The "best" mix isn't a static formula. It must align with your current cash flow needs and your 2026 contribution goals for the registered accounts we discussed previously.

Utilizing Holding Companies for Tax Deferral

A holding company can act as a powerful reservoir for your long-term wealth. It provides an extra layer of asset protection and allows you to move funds from an operating company via inter-corporate dividends. Under specific CRA conditions, these transfers can often occur tax-free, allowing you to accumulate wealth for future investment or estate planning without triggering immediate personal tax. If you're looking to refine your corporate architecture, our team at Tax Partners business solutions can help you design a structure that maximizes these deferral opportunities while ensuring full CRA compliance. Even the most robust investment plan can falter if it isn't viewed through a tax lens. One of the most pervasive pitfalls we see is "siloed" planning. This occurs when your investment advisor and your accountant operate in isolation. Without a unified strategy for tax efficient wealth management, you risk incurring unnecessary CRA interest and penalties. For instance, chasing high-yield investments in a non-registered account can be a tax disaster for high-income earners. The interest is taxed at your full marginal rate, which in 2026 reaches 33 percent federally for income over $258,482. This effectively wipes out a significant portion of your gains before you've even had a chance to reinvest. Digital assets present another hurdle. If you hold cryptocurrency, the CRA expects meticulous record-keeping. Failing to track the adjusted cost base (ACB) of each transaction can lead to severe audit headaches or penalties. Furthermore, if your foreign-held digital assets exceed certain cost thresholds, you may be required to file Form T1135. If you're managing complex digital portfolios, you should connect with our tax specialists to ensure your reporting is accurate and your structures are optimized for 2026 compliance.

Misunderstanding Capital Gains and Dividend Tax Credits

Capital gains remain a preferred form of income for CRA filers because of the inclusion rate. However, you must plan for the changes taking effect on January 1, 2026. For individuals, the inclusion rate increases to 66.7 percent only on net capital gains realized annually above a $250,000 threshold. For corporations, this higher rate applies to all gains. Many filers also find the "gross-up" and tax credit mechanism for Canadian dividends confusing. It's vital to distinguish between "eligible" dividends from large corporations and "non-eligible" dividends from small businesses. Assuming they're taxed the same can lead to significant errors in your personal cash flow projections.

The Risks of Improper Asset Location

Asset location is the deliberate act of placing high-tax investments, such as interest-bearing bonds, within your registered accounts. A common mistake is holding US-listed dividend stocks inside a TFSA. While the growth is tax-free in Canada, the US government often applies unrecoverable foreign withholding taxes because they don't recognize the TFSA as a retirement account. Conversely, Canadian equities are often better suited for non-registered accounts because they allow you to utilize the dividend tax credit effectively. Strategic placement ensures you aren't leaving money on the table or paying more to the CRA than is legally required. Securing your legacy in a shifting regulatory environment requires more than just a standard accounting service. It demands a partnership built on decades of institutional wisdom and a forward-thinking outlook. For 40 years, Tax Partners has served as a steady hand for Canadian families, helping them navigate the complexities of the Income Tax Act with confidence. By consolidating your bookkeeping, corporate tax, and wealth planning within a single firm, you eliminate the communication gaps that often lead to CRA audits or missed deductions. This integrated approach ensures that your personal and corporate plans are perfectly aligned, providing you with a seamless path toward long-term wealth preservation. We encourage our clients to move away from reactive, year-end filing and embrace year-round strategic management. When your tax and investment teams work in isolation, you lose the ability to pivot before deadlines arrive. Our comprehensive model allows us to monitor your "tax drag" in real time, adjusting your strategies as market conditions or CRA rules evolve. You gain the peace of mind that comes from knowing every dollar is working toward your family's future, rather than being eroded by inefficient structures or late-stage corrections.

The Proactive Guardian Approach to Wealth

At Tax Partners, we view our role as that of a "proactive guardian." We don't just react to requirements; we actively look ahead to secure better outcomes for your portfolio. This commitment to precision and foresight is woven into our Tax Partners mission and vision, which prioritizes ethical steadfastness and personalized care. Having managed over 495,000 returns, our firm possesses a deep database of CRA knowledge that we leverage to protect your capital. We understand the nuances of the 2026 tax landscape, and we use that expertise to ensure your wealth strategy remains resilient against any legislative changes.

Transitioning from Reactive Filing to Strategic Planning

Preparing for 2026 requires a holistic review of your financial architecture. To begin your journey toward tax efficient wealth management, we recommend preparing a few key items for your initial consultation. Bring your corporate articles of incorporation, your last three years of CRA notices of assessment, and a clear list of your family's long-term objectives. If you're a business owner considering an eventual exit, you should also review Succession Planning for Family Business to understand how to protect your hard-earned value during a transition. We invite you to reach out for a bespoke consultation today. Let us help you organize your financial life and provide the steady guidance you need to thrive in the years ahead. The transition into the 2026 tax year represents a pivotal moment for your financial health. By understanding how to minimize tax drag and strategically locating assets across your registered and corporate accounts, you can protect your capital from unnecessary erosion. We've explored how integrated planning for your corporation ensures that every dividend and salary decision supports your long-term family goals. Achieving true tax efficient wealth management is about more than just compliance; it's about gaining the foresight to act before the CRA's rules impact your returns. Our guidance ensures your personal and corporate plans are always aligned, removing the stress of siloed advice and missed opportunities. With over 40 years of Canadian tax expertise and 1,390 five-star Google reviews, our team has saved clients more than $87 million in taxes to date. We act as your proactive guardian, providing the stability and precision needed to thrive in a complex regulatory environment. Secure your financial future with Tax Partners' integrated wealth management services. You've worked hard to build your wealth, and we're here to ensure you keep it for generations to come.

What is the most tax-efficient way to invest in Canada?

The most tax-efficient way involves maximizing your registered accounts to eliminate or defer taxation on investment growth. By using structures like the TFSA, your gains remain entirely tax-free; whereas an RRSP provides an immediate deduction to lower your current taxable income. Beyond these accounts, focusing on capital gains rather than interest income in non-registered accounts ensures you benefit from a lower inclusion rate under CRA rules.

How does a holding company help with wealth management under CRA rules?

A holding company allows you to defer personal income taxes by retaining business profits within a corporate structure rather than paying them out as personal income. This strategy facilitates the reinvestment of capital that would otherwise be lost to high personal tax brackets. Additionally, holding companies provide a layer of asset protection and can receive tax-free inter-corporate dividends from an operating company under specific conditions.

Is a TFSA or an RRSP better for high-income professionals?

High-income professionals often find the RRSP more beneficial for immediate tax relief because contributions reduce income taxed at the highest marginal rates. However, a TFSA is an essential component of tax efficient wealth management because it provides flexibility and tax-free withdrawals in retirement. Most successful strategies involve maximizing both accounts to balance current tax savings with long-term, tax-free growth.

Can I split my investment income with my spouse to save on taxes?

You can split investment income, but you must strictly adhere to the CRA's Tax on Split Income (TOSI) rules to avoid high-rate penalties. Common legal methods include using a prescribed rate spousal loan, where one spouse lends money to the other at a CRA-approved interest rate. This allows the lower-income spouse to report the investment returns at their lower tax bracket, effectively reducing the family's total tax bill.

What is the difference between tax-efficient investing and tax-efficient wealth management?

Tax-efficient investing focuses on selecting specific financial products, like corporate class funds, to minimize taxes. In contrast, tax efficient wealth management is a holistic approach that integrates your corporate structure, personal income needs, and family estate planning. It ensures that every part of your financial life, from your bookkeeping to your long-term legacy, is organized to minimize the silent erosion caused by "tax drag."

How often should I review my tax-efficient wealth strategy with a CPA?

You should review your strategy at least once a year during your annual tax planning session. However, significant life events or major legislative shifts, such as the 2026 changes to capital gains inclusion rates, require more frequent consultations. Regular touchpoints with a CPA ensure your plan remains proactive rather than reactive, allowing you to adjust your asset location before the CRA's filing deadlines arrive.

Does the CRA tax capital gains differently than regular income?

The CRA taxes capital gains more favourably than regular interest income by only taxing a portion of the gain, known as the inclusion rate. Currently, this rate is 50 percent, but for many filers, it's scheduled to increase to 66.7 percent on January 1, 2026. This makes capital gains a preferred form of income for many investors compared to interest, which is taxed at your full marginal rate.

What happens if I over-contribute to my registered accounts like the TFSA?

Over-contributing to a TFSA or RRSP triggers a penalty tax of 1 percent per month on the excess amount for as long as it remains in the account. The CRA is very strict regarding these limits, so it's vital to track your contribution room through your official portals or with your accountant. If you discover an over-contribution, you should withdraw the excess funds immediately to stop the monthly penalty from compounding.