Succession Planning for Family Business: A Guide for Canadian Owners

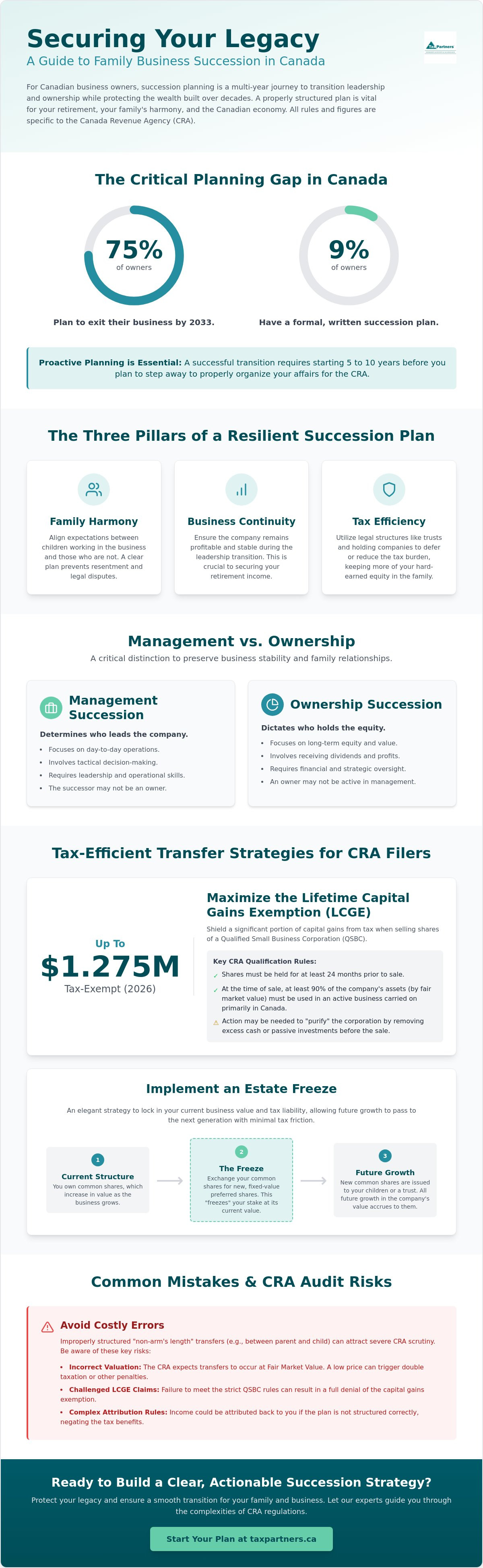

Did you know that while more than three-quarters of Canadian small business owners plan to exit their firms by 2033, only 9% have a formal roadmap in place? It's a staggering gap that often stems from a very personal place. You've spent a lifetime building your enterprise, and the thought of navigating intricate CRA tax rules or managing sensitive family dynamics can feel like a heavy burden. You want to ensure the next generation is truly ready to lead without risking the financial security you've worked so hard to achieve.

Effective succession planning for family business isn't just about paperwork; it's about securing your future and your family's peace of mind. In this guide, you'll learn how to protect your legacy and minimize tax liabilities when transitioning your company under current regulations. We'll walk you through strategic ways to utilize the $1,275,000 Lifetime Capital Gains Exemption (LCGE) for 2026 and organize a transition that balances professional leadership with personal harmony. We'll move from the uncertainty of "what if" to a clear, actionable strategy for a smooth leadership handover.

Key Takeaways

- Distinguish between management and ownership transitions to ensure your business continues to thrive while your family’s equity remains protected.

- Master the mechanics of an estate freeze to lock in current value and transfer future growth to the next generation with minimal tax friction.

- Explore how succession planning for family business uses formal governance to resolve conflicts before they start, keeping boardroom decisions separate from the dinner table.

- Learn to navigate complex CRA attribution rules and valuation requirements to avoid costly penalties or challenges to your transition plan.

What is Succession Planning for Family Business in Canada?

Succession planning is often mistaken for a one-time event, like signing a will or selling a piece of equipment. In reality, it's a strategic, multi-year transition of both leadership and ownership. For Canadian owners, this process involves moving the steering wheel of the company to the next generation or a third-party buyer while protecting the wealth built over decades. Since family businesses account for over 60% of private sector firms in Canada, getting this right is vital for both your personal retirement and the stability of the local economy.

Effective succession planning for family business requires a proactive approach that begins long before you plan to step away. The Canada Revenue Agency (CRA) takes a keen interest in these transitions, especially when they involve "non-arm's length" transfers. This is a technical term for deals between related people, such as parents and children. If you don't structure the sale or gift of shares correctly, the CRA may challenge the valuation. They generally expect the business to be transferred at fair market value. If the price is set too low without proper documentation, it can trigger double taxation or the loss of crucial tax credits. This complexity is why starting five to ten years early isn't just a suggestion; it's a necessity to organize your affairs properly.

The Three Pillars of a Canadian Succession Plan

A resilient plan stands on three foundational supports. First is family harmony. You must align the expectations of children who work in the business with those who don't. Without a clear path, resentment can simmer and eventually boil over into legal disputes. Second is business continuity. The company must remain profitable and stable while the keys change hands to ensure your retirement income is secure. Finally, there's tax efficiency. For CRA filers, this means using legal structures like trusts or holding companies to defer or reduce the tax burden. This ensures more of your hard-earned equity stays within the family circle.

Management vs. Ownership: A Critical Distinction

It's a common trap to assume that the person who owns the shares must also be the person running the daily operations. These are two distinct roles that require different skill sets. Management succession determines who makes the tactical decisions and leads the team. Ownership succession dictates who receives the dividends and holds the long-term equity. You might have a daughter who is a brilliant operational leader but a son who prefers a silent shareholder role. Defining these boundaries early prevents "centre-of-conflict" scenarios where family members feel slighted. Providing options for family members to remain as shareholders without being employees can preserve both the business and your family relationships.

Tax-Efficient Ownership Transfer Strategies for CRA Filers

Moving from the conceptual "who" to the technical "how" of succession planning for family business requires a precise understanding of the Income Tax Act. For CRA filers, the goal is to extract the maximum value from the enterprise while minimizing the tax friction that often accompanies a change in ownership. This involves more than just a simple sale. It requires a coordinated strategy that uses every available exemption and deferral mechanism to keep wealth within the family circle.

Maximizing the Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption (LCGE) remains a cornerstone of Canadian tax planning. For the 2026 tax year, the indexed value of this exemption is estimated at $1,275,000. This allows you to shield a significant portion of your gains from tax when you sell qualified small business corporation (SBC) shares. To qualify under CRA rules, your company must pass several rigorous tests. At least 90% of the company's assets must be used in active business in Canada at the time of the transfer. Additionally, you must have held the shares for at least 24 months. If your business has accumulated too much passive investment income or excess cash, you may need to "purify" the corporation by stripping out non-active assets well before the sale date.

Implementing an Estate Freeze

An estate freeze is an elegant way to lock in your current tax liability while passing future growth to your heirs. You exchange your existing common shares for fixed-value preferred shares. This move "freezes" the value of your interest at its current level, ensuring your future tax bill on the growth you've already achieved is predictable. New common shares are then issued to the next generation or a family trust for a nominal amount. As the business grows, that new value accrues to your children. This effectively defers capital gains tax until they eventually sell their interest. You can maintain control of the company by holding voting shares, which provides a safety net as the new leadership finds its footing.

While these tools are powerful, they must be managed with extreme care. The CRA's Tax on Split Income (TOSI) rules, often referred to as the "kiddie tax," can apply the highest marginal tax rate to dividends paid to family members who don't meet specific activity thresholds. It's a delicate balance that requires foresight and technical precision. If you're ready to start mapping out these technical steps, we can help you structure a plan that protects your family's wealth for the long term.

Structuring Governance to Preserve Wealth and Harmony

While tax efficiency secures your capital, governance secures your family's future. A common pitfall in succession planning for family business is the assumption that blood ties automatically lead to boardroom alignment. Without a clear set of rules, the lines between personal relationships and corporate responsibilities often blur. This is where a robust governance framework becomes essential, acting as a buffer against the conflicts that can derail even the most profitable Canadian enterprises. By formalizing how decisions are made, you protect both the business and the people you love.

Think of the Shareholders’ Agreement as the constitution of your company. It provides the legal certainty required to handle the "what-ifs" of life. This document should explicitly outline what happens if a shareholder faces disability, death, or simply wishes to retire. It often includes "shotgun" clauses, which are mechanisms where one shareholder offers to buy out another at a specific price, and the other must either accept or buy the first out at that same price. This serves as a powerful deterrent against prolonged disputes, ensuring the business can continue operating without being held hostage by a deadlock.

To protect the sanctity of the dinner table, many successful families establish a Family Council. This is a formal forum where family members, including those not active in the daily operations, can discuss the long-term vision and values of the firm. This proactive step is a cornerstone of succession planning for family business, as it establishes a culture of transparency. It separates emotional family discussions from the technical, profit-driven decisions of the board of directors. By setting clear entry and exit criteria, you ensure that family members join the business based on merit rather than birthright, which preserves morale among non-family employees.

The Essential Shareholders’ Agreement

A well-drafted agreement for CRA filers must include clear valuation formulas. Deciding how shares are priced before a conflict arises prevents expensive litigation later. You should also incorporate rights of first refusal, ensuring that if a family member wants to exit, the remaining shareholders have the first opportunity to purchase those shares. This keeps the ownership within the family and prevents outside interests from gaining a foothold in your private corporation. These provisions provide a steady hand at the helm when circumstances change unexpectedly.

Leadership Development and Mentorship

Preparing the next generation requires more than just a seat at the table. Many owners now require children to gain at least three to five years of outside experience before joining the family firm. This provides them with a fresh perspective and builds credibility with the existing team. Once they arrive, a formal training programme with specific performance benchmarks ensures they earn their leadership roles. This merit-based approach fosters a culture of excellence and prepares them for the complexities of running a Canadian business in a competitive market. It helps them realize their potential while ensuring the company’s legacy is in capable hands.

Common Succession Mistakes and CRA Audit Risks

Even with the best intentions, the technical execution of succession planning for family business can stumble on complex regulatory hurdles. The CRA maintains a watchful eye on transfers between related parties, searching for inconsistencies that could lead to significant tax reassessments. Avoiding these common pitfalls requires a blend of rigorous documentation and an objective view of your company's worth. A single error in how you structure a gift or sale of shares can evaporate the tax savings you worked so hard to achieve.

CRA Valuation Challenges

One of the most frequent mistakes is attempting a "sweetheart deal" by transferring shares to children at a price well below Fair Market Value (FMV). Under CRA rules, non-arm's length transactions must occur at FMV to be recognized as valid for tax purposes. If you sell shares for a nominal amount to a family member when the actual market value is significantly higher, the CRA may deem your proceeds to be the full market value. This often results in a double taxation trap: you pay tax on a gain you never actually received in cash, while the child's cost base remains at the lower price you set. An independent, professional valuation is non-negotiable for CRA compliance, providing the objective proof needed to justify the transfer price to the authorities.

The Complexity of Attribution Rules

The CRA uses attribution rules, specifically under Section 74.4 of the Income Tax Act, to prevent taxpayers from shifting income to family members in lower tax brackets. If you transfer property to a corporation to benefit a spouse or minor child, the CRA may attribute a portion of that corporate income back to you at your higher marginal tax rate. This is particularly relevant when navigating the Tax on Split Income (TOSI) rules, which apply the highest tax rate to certain types of income received by family members who don't meet specific "excluded business" criteria. To avoid this, family members must typically be actively engaged in the business on a regular, continuous, and substantial basis. Failure to document these roles and contributions can result in the CRA re-characterizing the income and stripping away your tax advantages.

The Danger of a Static Plan

Tax laws are not set in stone. As we've seen with the 2026 indexation of the Lifetime Capital Gains Exemption to an estimated $1,275,000, thresholds and rules evolve. A plan drafted five years ago may no longer be optimal under current CRA regulations or your family's current circumstances. Beyond the technicalities, neglecting the emotional readiness of your successors can lead to a leadership vacuum that threatens the company’s survival. A successful transition requires constant refinement as both the law and your family's goals change. If you're concerned about your current exposure to audit risks, contact our team to review your structure and ensure your legacy remains secure.

How Tax Partners Guides Your Family Transition

Transitioning a legacy requires more than just technical expertise; it demands a partner who understands the weight of your life's work. At Tax Partners, we've spent over 40 years helping Canadian families navigate these pivotal moments with confidence. Our role is that of a proactive guardian. We don't just react to CRA requirements; we look ahead to identify potential risks before they ever escalate into audits. By integrating your personal wealth with your corporate structure, we ensure that your succession planning for family business is both tax-efficient and emotionally sustainable.

We recognize that every enterprise is unique. Whether you're managing a portfolio in real estate, a private practice in healthcare, or a firm in the tech sector, we provide customized roadmaps. These plans balance your need for financial security in retirement with the desire for long-term family harmony. Our team takes the stress out of complex regulations, providing a steady hand at the helm so you can focus on the next chapter of your life.

Integrated Financial and Tax Advisory

A successful transition involves many moving parts that must work in perfect synchronization. We coordinate directly with your legal team to ensure that every Shareholders' Agreement and trust deed accurately reflects your broader tax strategy. This level of precision is vital for CRA filers, as even small discrepancies between legal documents and tax filings can trigger unwanted scrutiny. We also conduct regular reviews to keep your plan aligned with shifting CRA thresholds and legislative updates. This methodical approach ensures your strategy remains robust, regardless of how the economic environment evolves.

Begin Your Legacy Planning Today

The most important step in any transition is the first conversation. We're committed to providing clear, plain-language advice that demystifies complex financial matters for you and your heirs. You won't find dense, impenetrable jargon here. Instead, you'll find an accessible expert who is deeply invested in your success and your family's future. We want to lead you from a state of potential uncertainty toward a feeling of total control over your business legacy. Secure your family’s future with a professional succession plan from Tax Partners and ensure that what you've built continues to thrive for generations to come.

Secure Your Legacy for the Next Generation

Transitioning your life's work is a profound milestone that requires both technical precision and emotional foresight. By aligning tax-efficient structures like estate freezes with robust governance frameworks, you protect your wealth while preserving family harmony. Proactive succession planning for family business ensures that your transition happens on your terms, not the CRA's. It's about moving from a state of uncertainty to one of complete control and lasting peace of mind.

Since 1981, our team has filed over 495,000 returns and helped clients save more than $87M in taxes. With over 1,390 five-star Google reviews, we've built a reputation for deep reliability and personalized care. We're here to act as your proactive guardian, looking ahead to secure a better outcome for your family and your enterprise. Your legacy is too important to leave to chance. Contact Tax Partners for a Comprehensive Succession Planning Consultation and take the first step toward a seamless transition today.

Frequently Asked Questions

When should I start succession planning for my family business?

You should ideally begin the process five to ten years before your anticipated retirement date. This timeline allows you to "purify" your corporation to meet CRA eligibility tests for tax exemptions and gives you enough time to mentor your successor. Starting early ensures that leadership and ownership transitions happen gradually; this reduces the risk of operational disruption or family conflict during the handover.

Can I pass my business to my children tax-free in Canada?

While a completely tax-free transfer is rare, you can significantly reduce or defer the tax burden for CRA filers using strategic tools. For example, rules surrounding intergenerational transfers make it easier to sell shares to your children while still accessing the Lifetime Capital Gains Exemption. By using an estate freeze or a family trust, you can defer capital gains taxes until a later date, effectively preserving the company's capital.

What is the Lifetime Capital Gains Exemption (LCGE) for 2026?

For the 2026 tax year, the Lifetime Capital Gains Exemption is estimated to be $1,275,000 due to inflation indexing. This exemption allows Canadian owners to shield a portion of the capital gains realized on the sale of qualified small business corporation shares. Because these thresholds change annually, you should verify the exact limit with the CRA or a qualified tax professional before finalizing any share transfers or sales.

What happens to the business if I die without a succession plan?

If a business owner dies without a plan, the CRA generally treats the shares as having been sold at fair market value immediately before death. This "deemed disposition" can trigger a massive capital gains tax bill that the estate may not have the liquid cash to pay. Without a clear roadmap, the business could be forced into a fire sale or become the centre of a protracted legal battle.

Is a family trust better than an estate freeze for succession?

A family trust and an estate freeze are not mutually exclusive; they're often used together to maximize flexibility. An estate freeze locks in your current tax liability, while a family trust holds the new growth shares for multiple beneficiaries. This combination allows you to decide later which family members should receive dividends or equity, providing a layer of protection against future changes in family dynamics or tax laws.

How does the CRA view selling my business to a family member at a discount?

The CRA views sales to family members as "non-arm's length" transactions and expects them to occur at fair market value. If you sell your business at a significant discount, the CRA may adjust the transfer price for tax purposes. This can lead to double taxation, where you're taxed on a gain you didn't receive while your child is stuck with a lower cost base for future sales.

What is a Shareholders’ Agreement and why do I need one for a family firm?

A Shareholders’ Agreement acts as the legal constitution for succession planning for family business by defining how shares are bought, sold, or transferred. It provides a clear framework for handling death, disability, divorce, departure, and disagreement. By establishing these rules while everyone is on good terms, you prevent future disputes from reaching the courtroom and ensure the business remains stable during leadership transitions.

How do I handle family members who are not active in the business?

You can handle inactive family members by providing them with an inheritance through non-business assets or life insurance proceeds rather than company shares. If they must hold equity, consider issuing non-voting shares that provide dividend income without giving them a say in daily operations. This approach maintains "sweat equity" for the children running the firm while ensuring overall estate fairness for those who chose different career paths.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Frequently Asked Questions

The Three Pillars of a Canadian Succession Plan

A resilient plan stands on three foundational supports. First is family harmony. You must align the expectations of children who work in the business with those who don't. Without a clear path, resentment can simmer and eventually boil over into legal disputes. Second is business continuity. The company must remain profitable and stable while the keys change hands to ensure your retirement income is secure. Finally, there's tax efficiency. For CRA filers, this means using legal structures like trusts or holding companies to defer or reduce the tax burden. This ensures more of your hard-earned equity stays within the family circle.

Management vs. Ownership: A Critical Distinction

It's a common trap to assume that the person who owns the shares must also be the person running the daily operations. These are two distinct roles that require different skill sets. Management succession determines who makes the tactical decisions and leads the team. Ownership succession dictates who receives the dividends and holds the long-term equity. You might have a daughter who is a brilliant operational leader but a son who prefers a silent shareholder role. Defining these boundaries early prevents "centre-of-conflict" scenarios where family members feel slighted. Providing options for family members to remain as shareholders without being employees can preserve both the business and your family relationships. Moving from the conceptual "who" to the technical "how" of succession planning for family business requires a precise understanding of the Income Tax Act. For CRA filers, the goal is to extract the maximum value from the enterprise while minimizing the tax friction that often accompanies a change in ownership. This involves more than just a simple sale. It requires a coordinated strategy that uses every available exemption and deferral mechanism to keep wealth within the family circle.

Maximizing the Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption (LCGE) remains a cornerstone of Canadian tax planning. For the 2026 tax year, the indexed value of this exemption is estimated at $1,275,000. This allows you to shield a significant portion of your gains from tax when you sell qualified small business corporation (SBC) shares. To qualify under CRA rules, your company must pass several rigorous tests. At least 90% of the company's assets must be used in active business in Canada at the time of the transfer. Additionally, you must have held the shares for at least 24 months. If your business has accumulated too much passive investment income or excess cash, you may need to "purify" the corporation by stripping out non-active assets well before the sale date.

Implementing an Estate Freeze

An estate freeze is an elegant way to lock in your current tax liability while passing future growth to your heirs. You exchange your existing common shares for fixed-value preferred shares. This move "freezes" the value of your interest at its current level, ensuring your future tax bill on the growth you've already achieved is predictable. New common shares are then issued to the next generation or a family trust for a nominal amount. As the business grows, that new value accrues to your children. This effectively defers capital gains tax until they eventually sell their interest. You can maintain control of the company by holding voting shares, which provides a safety net as the new leadership finds its footing. While these tools are powerful, they must be managed with extreme care. The CRA's Tax on Split Income (TOSI) rules, often referred to as the "kiddie tax," can apply the highest marginal tax rate to dividends paid to family members who don't meet specific activity thresholds. It's a delicate balance that requires foresight and technical precision. If you're ready to start mapping out these technical steps, we can help you structure a plan that protects your family's wealth for the long term. While tax efficiency secures your capital, governance secures your family's future. A common pitfall in succession planning for family business is the assumption that blood ties automatically lead to boardroom alignment. Without a clear set of rules, the lines between personal relationships and corporate responsibilities often blur. This is where a robust governance framework becomes essential, acting as a buffer against the conflicts that can derail even the most profitable Canadian enterprises. By formalizing how decisions are made, you protect both the business and the people you love. Think of the Shareholders’ Agreement as the constitution of your company. It provides the legal certainty required to handle the "what-ifs" of life. This document should explicitly outline what happens if a shareholder faces disability, death, or simply wishes to retire. It often includes "shotgun" clauses, which are mechanisms where one shareholder offers to buy out another at a specific price, and the other must either accept or buy the first out at that same price. This serves as a powerful deterrent against prolonged disputes, ensuring the business can continue operating without being held hostage by a deadlock. To protect the sanctity of the dinner table, many successful families establish a Family Council. This is a formal forum where family members, including those not active in the daily operations, can discuss the long-term vision and values of the firm. This proactive step is a cornerstone of succession planning for family business, as it establishes a culture of transparency. It separates emotional family discussions from the technical, profit-driven decisions of the board of directors. By setting clear entry and exit criteria, you ensure that family members join the business based on merit rather than birthright, which preserves morale among non-family employees.

The Essential Shareholders’ Agreement

A well-drafted agreement for CRA filers must include clear valuation formulas. Deciding how shares are priced before a conflict arises prevents expensive litigation later. You should also incorporate rights of first refusal, ensuring that if a family member wants to exit, the remaining shareholders have the first opportunity to purchase those shares. This keeps the ownership within the family and prevents outside interests from gaining a foothold in your private corporation. These provisions provide a steady hand at the helm when circumstances change unexpectedly.

Leadership Development and Mentorship

Preparing the next generation requires more than just a seat at the table. Many owners now require children to gain at least three to five years of outside experience before joining the family firm. This provides them with a fresh perspective and builds credibility with the existing team. Once they arrive, a formal training programme with specific performance benchmarks ensures they earn their leadership roles. This merit-based approach fosters a culture of excellence and prepares them for the complexities of running a Canadian business in a competitive market. It helps them realize their potential while ensuring the company’s legacy is in capable hands. Even with the best intentions, the technical execution of succession planning for family business can stumble on complex regulatory hurdles. The CRA maintains a watchful eye on transfers between related parties, searching for inconsistencies that could lead to significant tax reassessments. Avoiding these common pitfalls requires a blend of rigorous documentation and an objective view of your company's worth. A single error in how you structure a gift or sale of shares can evaporate the tax savings you worked so hard to achieve.

CRA Valuation Challenges

One of the most frequent mistakes is attempting a "sweetheart deal" by transferring shares to children at a price well below Fair Market Value (FMV). Under CRA rules, non-arm's length transactions must occur at FMV to be recognized as valid for tax purposes. If you sell shares for a nominal amount to a family member when the actual market value is significantly higher, the CRA may deem your proceeds to be the full market value. This often results in a double taxation trap: you pay tax on a gain you never actually received in cash, while the child's cost base remains at the lower price you set. An independent, professional valuation is non-negotiable for CRA compliance, providing the objective proof needed to justify the transfer price to the authorities.

The Complexity of Attribution Rules

The CRA uses attribution rules, specifically under Section 74.4 of the Income Tax Act, to prevent taxpayers from shifting income to family members in lower tax brackets. If you transfer property to a corporation to benefit a spouse or minor child, the CRA may attribute a portion of that corporate income back to you at your higher marginal tax rate. This is particularly relevant when navigating the Tax on Split Income (TOSI) rules, which apply the highest tax rate to certain types of income received by family members who don't meet specific "excluded business" criteria. To avoid this, family members must typically be actively engaged in the business on a regular, continuous, and substantial basis. Failure to document these roles and contributions can result in the CRA re-characterizing the income and stripping away your tax advantages.

The Danger of a Static Plan

Tax laws are not set in stone. As we've seen with the 2026 indexation of the Lifetime Capital Gains Exemption to an estimated $1,275,000, thresholds and rules evolve. A plan drafted five years ago may no longer be optimal under current CRA regulations or your family's current circumstances. Beyond the technicalities, neglecting the emotional readiness of your successors can lead to a leadership vacuum that threatens the company’s survival. A successful transition requires constant refinement as both the law and your family's goals change. If you're concerned about your current exposure to audit risks, contact our team to review your structure and ensure your legacy remains secure. Transitioning a legacy requires more than just technical expertise; it demands a partner who understands the weight of your life's work. At Tax Partners, we've spent over 40 years helping Canadian families navigate these pivotal moments with confidence. Our role is that of a proactive guardian. We don't just react to CRA requirements; we look ahead to identify potential risks before they ever escalate into audits. By integrating your personal wealth with your corporate structure, we ensure that your succession planning for family business is both tax-efficient and emotionally sustainable. We recognize that every enterprise is unique. Whether you're managing a portfolio in real estate, a private practice in healthcare, or a firm in the tech sector, we provide customized roadmaps. These plans balance your need for financial security in retirement with the desire for long-term family harmony. Our team takes the stress out of complex regulations, providing a steady hand at the helm so you can focus on the next chapter of your life.

Integrated Financial and Tax Advisory

A successful transition involves many moving parts that must work in perfect synchronization. We coordinate directly with your legal team to ensure that every Shareholders' Agreement and trust deed accurately reflects your broader tax strategy. This level of precision is vital for CRA filers, as even small discrepancies between legal documents and tax filings can trigger unwanted scrutiny. We also conduct regular reviews to keep your plan aligned with shifting CRA thresholds and legislative updates. This methodical approach ensures your strategy remains robust, regardless of how the economic environment evolves.

Begin Your Legacy Planning Today

The most important step in any transition is the first conversation. We're committed to providing clear, plain-language advice that demystifies complex financial matters for you and your heirs. You won't find dense, impenetrable jargon here. Instead, you'll find an accessible expert who is deeply invested in your success and your family's future. We want to lead you from a state of potential uncertainty toward a feeling of total control over your business legacy. Secure your family’s future with a professional succession plan from Tax Partners and ensure that what you've built continues to thrive for generations to come. Transitioning your life's work is a profound milestone that requires both technical precision and emotional foresight. By aligning tax-efficient structures like estate freezes with robust governance frameworks, you protect your wealth while preserving family harmony. Proactive succession planning for family business ensures that your transition happens on your terms, not the CRA's. It's about moving from a state of uncertainty to one of complete control and lasting peace of mind. Since 1981, our team has filed over 495,000 returns and helped clients save more than $87M in taxes. With over 1,390 five-star Google reviews, we've built a reputation for deep reliability and personalized care. We're here to act as your proactive guardian, looking ahead to secure a better outcome for your family and your enterprise. Your legacy is too important to leave to chance. Contact Tax Partners for a Comprehensive Succession Planning Consultation and take the first step toward a seamless transition today.

When should I start succession planning for my family business?

You should ideally begin the process five to ten years before your anticipated retirement date. This timeline allows you to "purify" your corporation to meet CRA eligibility tests for tax exemptions and gives you enough time to mentor your successor. Starting early ensures that leadership and ownership transitions happen gradually; this reduces the risk of operational disruption or family conflict during the handover.

Can I pass my business to my children tax-free in Canada?

While a completely tax-free transfer is rare, you can significantly reduce or defer the tax burden for CRA filers using strategic tools. For example, rules surrounding intergenerational transfers make it easier to sell shares to your children while still accessing the Lifetime Capital Gains Exemption. By using an estate freeze or a family trust, you can defer capital gains taxes until a later date, effectively preserving the company's capital.

What is the Lifetime Capital Gains Exemption (LCGE) for 2026?

For the 2026 tax year, the Lifetime Capital Gains Exemption is estimated to be $1,275,000 due to inflation indexing. This exemption allows Canadian owners to shield a portion of the capital gains realized on the sale of qualified small business corporation shares. Because these thresholds change annually, you should verify the exact limit with the CRA or a qualified tax professional before finalizing any share transfers or sales.

What happens to the business if I die without a succession plan?

If a business owner dies without a plan, the CRA generally treats the shares as having been sold at fair market value immediately before death. This "deemed disposition" can trigger a massive capital gains tax bill that the estate may not have the liquid cash to pay. Without a clear roadmap, the business could be forced into a fire sale or become the centre of a protracted legal battle.

Is a family trust better than an estate freeze for succession?

A family trust and an estate freeze are not mutually exclusive; they're often used together to maximize flexibility. An estate freeze locks in your current tax liability, while a family trust holds the new growth shares for multiple beneficiaries. This combination allows you to decide later which family members should receive dividends or equity, providing a layer of protection against future changes in family dynamics or tax laws.

How does the CRA view selling my business to a family member at a discount?

The CRA views sales to family members as "non-arm's length" transactions and expects them to occur at fair market value. If you sell your business at a significant discount, the CRA may adjust the transfer price for tax purposes. This can lead to double taxation, where you're taxed on a gain you didn't receive while your child is stuck with a lower cost base for future sales.

What is a Shareholders’ Agreement and why do I need one for a family firm?

A Shareholders’ Agreement acts as the legal constitution for succession planning for family business by defining how shares are bought, sold, or transferred. It provides a clear framework for handling death, disability, divorce, departure, and disagreement. By establishing these rules while everyone is on good terms, you prevent future disputes from reaching the courtroom and ensure the business remains stable during leadership transitions.

How do I handle family members who are not active in the business?

You can handle inactive family members by providing them with an inheritance through non-business assets or life insurance proceeds rather than company shares. If they must hold equity, consider issuing non-voting shares that provide dividend income without giving them a say in daily operations. This approach maintains "sweat equity" for the children running the firm while ensuring overall estate fairness for those who chose different career paths.