CRA Audit Help: A Comprehensive Guide for Canadian Taxpayers in 2026

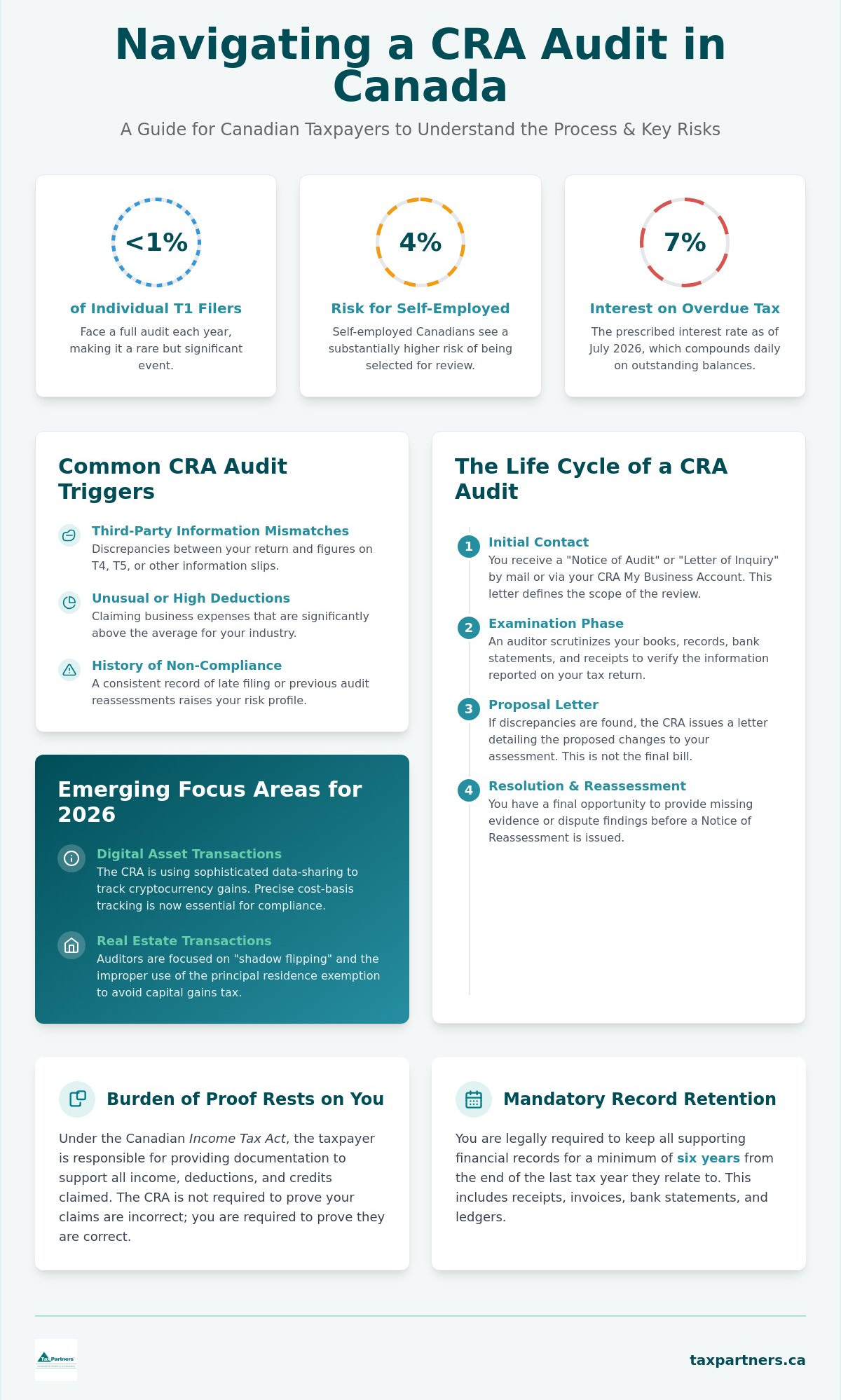

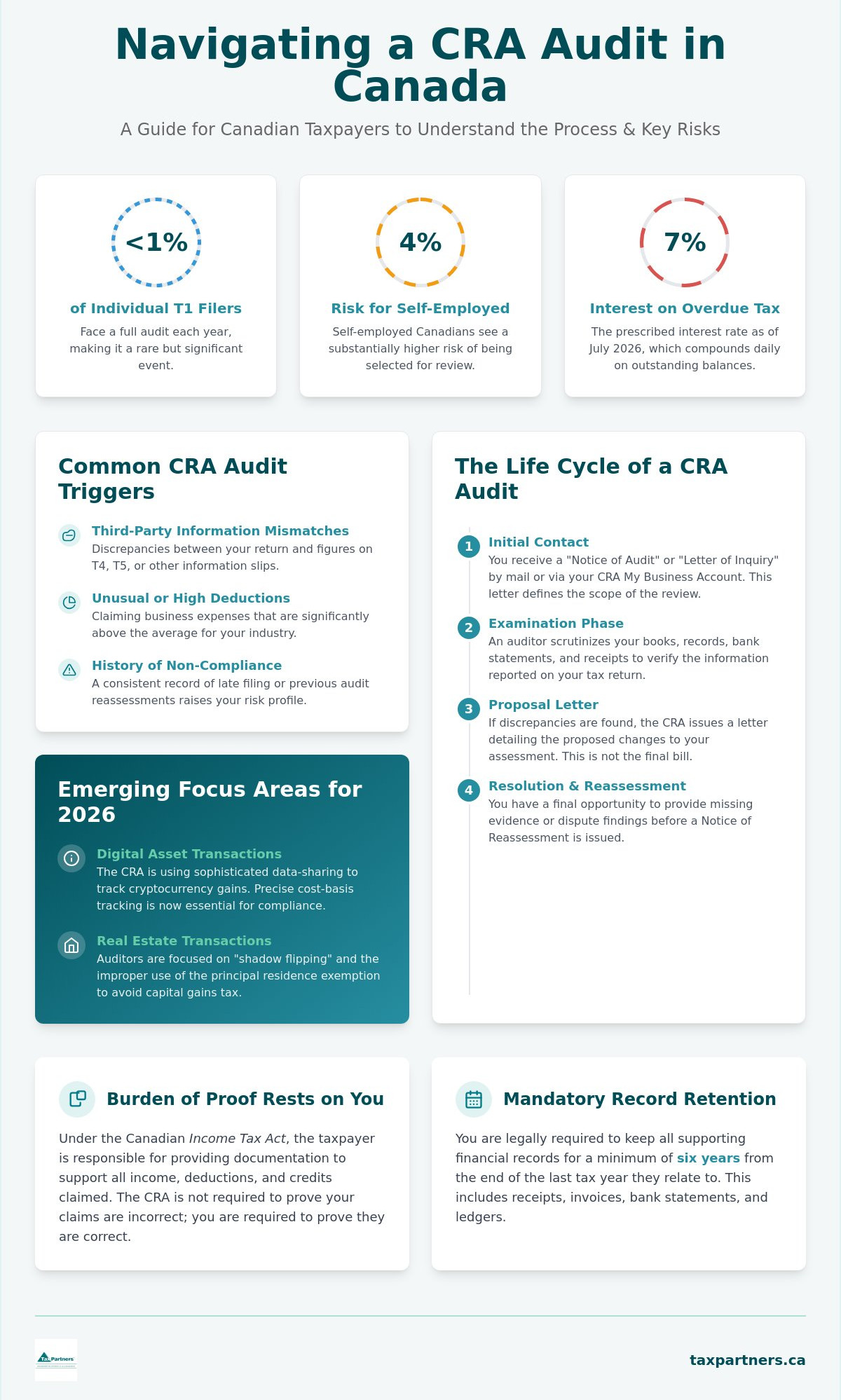

While less than 1% of individual T1 filers face a full audit each year, self-employed Canadians see that risk climb as high as 4%. Receiving a formal letter from the Canada Revenue Agency often feels like an immediate crisis, especially with the interest rate on overdue taxes currently sitting at 7% as of July 2026. You aren't alone if your first instinct is to worry about heavy penalties or the daunting task of gathering years of historical records. Seeking professional CRA audit help isn't just about defence. It's about regaining control over your financial narrative and ensuring every response is handled with meticulous care.

We understand that the complexity of CRA documentation requests can feel overwhelming and incredibly time-consuming. This guide will show you how to navigate the audit process with professional precision while protecting your rights under Canadian tax law. You'll learn about the latest 2026 interest rates, common triggers such as unreported digital economy income, and the specific steps you can take to secure a fair outcome with minimal reassessment. By the end of this article, you'll have a clear roadmap to move from uncertainty to a state of total control.

Key Takeaways

- Understand how the CRA uses sophisticated risk-assessment models to select filers and why your initial response to a Notice of Audit is critical for a successful outcome.

- Discover how professional CRA audit help acts as a strategic buffer, allowing an authorized representative to manage complex inquiries through the My Business Account portal.

- Learn why the burden of proof rests on the taxpayer under the Income Tax Act and how to adhere to the mandatory six-year record retention rule.

- Identify the specific triggers the CRA prioritizes in 2026, such as digital economy income and real estate transactions, to ensure your records are audit-ready.

- Explore a methodical resolution process designed to protect your rights and minimize potential penalties or interest during a formal review of your books and records.

Understanding the CRA Audit: Why Canadian Filers Are Selected

Under the Income Tax Act (ITA), an audit is defined as a formal examination of a taxpayer's books and records to ensure they fulfill their legal obligations. The Canada Revenue Agency (CRA) doesn't usually choose targets based on a roll of the dice. Instead, the agency employs a sophisticated risk-assessment model that analyzes thousands of data points to flag potential non-compliance. If your tax return deviates significantly from established norms or industry benchmarks, it's more likely to be selected for a closer look. This proactive monitoring allows the CRA to focus its resources where it believes tax revenue is most at risk.

It's helpful to distinguish between the different levels of scrutiny you might face. A "desk review" is typically a limited inquiry where an officer requests specific receipts or documents via mail or through your My Account portal. These are common and often resolved quickly. In contrast, a "field audit" is a comprehensive examination where an auditor may visit your place of business to review your entire financial history. Regardless of the scope, seeking professional CRA audit help early ensures you don't inadvertently provide more information than required. Transparency and meticulous record-keeping serve as your first line of defence, turning a potentially hostile process into a manageable verification exercise.

Common Triggers for a CRA Review in 2026

The CRA's automated systems are now highly efficient at spotting discrepancies between what you report and the information submitted by third parties. If the figures on your T4 or T5 slips don't match your return exactly, a computer-generated flag is almost certain. Another major trigger involves claiming unusual or high-value business deductions that seem out of proportion to your industry's averages. Finally, a consistent history of late filing or previous compliance issues creates a "risk profile" that makes you a frequent candidate for scrutiny. Staying organized isn't just about efficiency; it's about staying off the CRA's high-risk list.

Emerging Focus Areas: Crypto and Real Estate

In 2026, the CRA is paying closer attention to digital asset transactions than ever before. Sophisticated data-sharing agreements with major exchanges mean that cryptocurrency gains are no longer invisible to tax authorities. If you've been active in the crypto market, you must ensure your cost-basis tracking is precise. Similarly, the real estate sector remains a top priority for enforcement. Auditors are specifically looking for "shadow flipping" or the improper use of the principal residence exemption to avoid capital gains tax. If you're involved in property transactions, reviewing the CRA audit risks for real estate can help you understand how to document these complex sales properly. Professional CRA audit help can provide the foresight needed to address these emerging sectors before an auditor initiates contact.

The Life Cycle of a CRA Audit Under Canadian Tax Rules

An audit isn't a single event but a structured sequence of interactions. It begins when a "Notice of Audit" or "Letter of Inquiry" arrives in your mailbox or appears in your My Business Account. This initial contact defines the scope of the review. Your first response is vital because it sets the professional tone for the entire engagement. Being prompt and organized suggests that your books are in order, which can sometimes limit the auditor's desire to dig deeper into unrelated fiscal years. If the process feels overwhelming, connecting with our team can help you prepare your records effectively before the first meeting.

During the examination phase, the auditor scrutinizes your bank statements, receipts, and journals. Understanding the official CRA audit process helps you anticipate their moves. They're looking for evidence that supports the numbers you reported. If they find discrepancies, they won't issue a bill immediately. Instead, they'll send a "Proposal Letter." This document outlines the changes they intend to make and provides a final opportunity for you to present missing evidence. Professional CRA audit help is particularly valuable during this examination phase to ensure the auditor's findings are based on a complete and accurate understanding of your financial history.

The Information Request and Documentation Phase

The auditor will issue a Request for Information (RFI) that lists the specific documents they need to see. It's a common mistake to provide more information than what was explicitly requested. Doing so can inadvertently open new lines of inquiry that weren't part of the original scope. You should organize your digital and physical records to match the auditor's list exactly. This methodical approach facilitates a smoother review and demonstrates that you're acting in good faith. Clear, indexed records often lead to a faster resolution and fewer follow-up questions.

Responding to Proposed Reassessments

Once the auditor completes their review, they issue a proposal letter if they intend to change your tax return. You generally have a 30-day window to respond to this letter before it becomes final. This is your most critical opportunity for negotiation. You must craft a professional rebuttal supported by specific references to the Income Tax Act or relevant tax court cases. A CPA can often negotiate these adjustments down by identifying expenses the auditor may have overlooked or misinterpreted. If no rebuttal is sent, the CRA will issue a final Notice of Reassessment, which triggers the 7% interest rate on any balance owing as of July 2026.

CRA Audit Help: Professional Representation vs. Self-Representation

Facing a CRA auditor alone can feel like stepping into a courtroom without a lawyer. While the law allows you to represent yourself, the psychological toll of direct confrontation often leads to costly errors. Professional CRA audit help provides a vital buffer. It transforms what could be a high-stakes interrogation into a structured, technical exchange of facts. By appointing an authorized representative through the CRA's My Business Account, you delegate the technical heavy lifting to an expert who understands the nuances of the Income Tax Act. This shield allows you to focus on your business while we handle the scrutiny.

Most taxpayers aren't trained in the specific art of the audit. Under pressure, it's remarkably easy to volunteer information that wasn't requested. This inadvertent disclosure can lead an auditor to expand their review into other tax years or unrelated business activities. An expert ensures that the scope remains narrow and focused. When weighing professional fees, you must consider the potential for significant long-term savings. A well-managed audit often leads to reduced reassessments and helps you avoid harsh penalties, such as the 50% gross negligence penalty for understated tax. It's an investment in protecting your financial future from avoidable interest and adjustments.

Why Direct Communication with Auditors Can Be Risky

The auditor’s primary mandate is to verify compliance. They aren't looking for ways to lower your tax bill or find missed deductions. Casual comments about your personal lifestyle or business habits might be misinterpreted as admissions of negligence or intent. For CRA filers, every word carries weight. Ensuring all communication is written and precisely focused on the audit scope creates a clear, defensible paper trail. This level of precision prevents the auditor from making assumptions based on off-hand remarks or incomplete explanations.

The Role of a CPA as a Proactive Guardian

A CPA does more than just hand over folders of receipts. They translate your internal accounting records into the specific formats the CRA prefers, which reduces friction during the review. If the auditor makes a logical leap or a calculation error, your representative is there to challenge it immediately with professional authority. They manage the auditor’s expectations regarding timelines and data delivery, ensuring you aren't rushed into providing incomplete or unverified records. This proactive stance positions you as an organized and compliant taxpayer, which often leads to a more favourable and efficient resolution.

Preparing Your Defense: Documentation and the Burden of Proof

In a Canadian tax audit, the legal landscape differs significantly from other areas of law. The burden of proof rests squarely on your shoulders. Under the Income Tax Act, the CRA's assumptions are considered correct until you provide documentation that proves otherwise. This reality makes thorough record-keeping your most powerful tool. By law, you must retain all relevant records for a minimum of six years from the end of the last tax year they relate to. If you find yourself missing specific receipts, professional CRA audit help can assist in reconstructing your history through bank statements or third-party affidavits. We often recommend maintaining contemporaneous documentation, which are notes made at the exact time of a transaction, as these carry significant weight with auditors during a review.

Reconstructing a financial narrative from years ago is a daunting task. Auditors look for a clear, unbroken trail from your bank account to your general ledger. If there are gaps in your story, the auditor is permitted to make "reasonable" assumptions, which rarely favour the taxpayer. Having a proactive guardian to help you assemble these pieces ensures that your defense is built on facts rather than estimates. Organized records don't just win audits; they often shorten the duration of the investigation by giving the auditor exactly what they need in a format they can easily verify.

Essential Records for a Business Audit

Auditors expect your general ledgers, purchase invoices, and sales receipts to be readily available. You'll also need to produce corporate minute books and evidence of business-related travel or entertainment, such as logs or calendars. A frequent area of scrutiny for CRA filers involves GST/HST input tax credits (ITCs). To claim these, you must have valid invoices that include the supplier's GST/HST registration number. If your records are currently disorganized, it's best to connect with our team to ensure your files are audit-ready before the CRA's deadline.

Managing Deadlines and Extension Requests

The CRA typically sets tight deadlines for information requests, often giving taxpayers only 30 days to comply. If your files are complex or archived, you can request an extension, but you must do so before the original deadline expires. It's vital to confirm all extensions in writing to avoid "failure to comply" penalties. You should also be aware of the "statute-barred" period. Generally, the CRA can only reassess a return within three years of the date on your original Notice of Assessment. However, if they suspect fraud or misrepresentation, this limit is waived. Navigating these timelines requires precision and foresight to ensure you don't inadvertently waive your rights or miss a critical rebuttal window.

Secure Your Outcome with Tax Partners Professional Advisory

Experience is the most valuable asset when facing federal scrutiny. Tax Partners leverages over 40 years of institutional wisdom to manage complex CRA audit files with a level of precision that smaller firms cannot match. We don't believe in a reactive or defensive posture. Instead, we employ a methodical approach that begins with an intensive file review to identify every potential vulnerability before the auditor ever asks a question. This foresight allows us to present your financial narrative with professional clarity, ensuring that your rights remain protected throughout the entire interaction. For CRA filers, having this level of expertise is the difference between a stressful ordeal and a controlled, technical verification.

Our team acts as a steady hand at the helm, alleviating the heavy emotional and administrative burden of an investigation. We serve as your proactive guardian, managing all correspondence and acting as the primary point of contact for the CRA. As a national firm, we possess a deep understanding of the specific nuances within various Canadian industries, from emerging digital sectors to established real estate markets. This breadth of knowledge ensures that we can defend your position effectively by speaking the auditor's language. When you seek our CRA audit help, you gain a long-term partner dedicated to your financial steadfastness and ethical compliance.

Bespoke Audit Management Strategies

We develop customized preparation plans tailored to your specific industry and the unique triggers that led to your selection. Our experts engage in direct negotiation with CRA auditors to resolve disputes at the examination stage, which often prevents a file from escalating into a more punitive phase. We don't just look at the current year; we conduct a comprehensive review of your entire filing history to identify and mitigate potential future risks. This strategic oversight ensures that your business remains a low-priority target for future interventions.

Beyond the Audit: Long-Term Compliance and Wealth Preservation

A successful audit resolution should serve as a foundation for future stability. We help you implement robust bookkeeping and payroll systems that prevent the common clerical errors that often trigger CRA reviews. Beyond immediate compliance, our wealth management and financial planning services are designed to ensure you keep more of what you earn under Canadian law. We look ahead to secure your better outcome by combining modern accounting practices with decades of regulatory experience. Contact Tax Partners for a confidential audit consultation today.

Take Control of Your Audit Resolution

Navigating a CRA audit requires more than just compliance; it demands a strategic defence built on organized records and technical expertise. You've learned that the burden of proof rests on your shoulders. The first 30 days after receiving a proposal letter are your most critical window for negotiation. By maintaining meticulous documentation for at least six years, you create a foundation of transparency that simplifies the review process.

Professional CRA audit help ensures that your case is presented with precision while shielding you from the stress of direct negotiation. With over 40 years of Canadian tax experience and more than 495,000 returns filed, our team brings a legacy of reliability to your file. Our 1,390+ five-star Google reviews reflect our commitment to acting as a proactive guardian for our clients. Speak with a CPA about your CRA audit today to regain total control over your tax situation. We're here to guide you toward a fair resolution with confidence.

Frequently Asked Questions

How long does the CRA have to audit my tax return?

Under Canadian tax rules, the CRA generally has three years from the date of your original Notice of Assessment to reassess your return. This is known as the normal reassessment period. However, this limit is waived if the CRA suspects fraud or misrepresentation due to neglect or carelessness. In those cases, they can audit much further back. It's best to check your specific assessment dates to confirm your current status.

What happens if I cannot find the receipts the CRA is asking for?

If you cannot locate specific receipts, you must provide alternative evidence to support your claims. The CRA may accept bank statements, cancelled cheques, or written affidavits from third parties as secondary proof. However, without a formal receipt, the auditor has the discretion to disallow the expense entirely. Seeking professional CRA audit help can assist you in reconstructing your records to satisfy the auditor's requirements and protect your interests.

Can the CRA freeze my bank account during an audit?

No, the CRA typically does not freeze bank accounts during the audit phase itself. Freezing an account is a collection action that usually occurs only after a final Notice of Reassessment has been issued and the taxpayer has failed to pay the resulting debt. During the audit, the focus remains on verifying your books and records rather than seizing assets. Collections only begin once the tax liability is finalized.

What is the difference between a desk audit and a field audit?

A desk audit is a limited review conducted through correspondence where the auditor requests specific documents by mail or via your My Account portal. A field audit is much more comprehensive and involves an auditor visiting your home or place of business to examine your entire financial history. Field audits are typically reserved for complex files or business owners with high-value revenue streams that require on-site verification.

Do I have to meet the CRA auditor at my home or place of business?

You are not legally required to host the auditor at your personal residence if you have a representative. While the CRA may request an on-site visit to verify business operations, these meetings can often be held at your accountant's office instead. This provides a professional environment and ensures the auditor only has access to the specific records relevant to the current inquiry. It also minimizes disruption to your daily routine.

What should I do if I disagree with the CRA’s final reassessment?

You have the right to challenge a reassessment by filing a formal Notice of Objection. For most individual filers, this must be done within 90 days of the date on your Notice of Reassessment. This step initiates an independent review by the CRA’s Appeals Division. It's a critical process for taxpayers who believe the auditor made a logical or legal error during the examination and want a second opinion.

Will the CRA audit my previous years if they find an error in this year?

Yes, the CRA can expand an audit to previous years if they discover significant or recurring errors in the year under review. If a mistake appears to be part of a systemic pattern, the auditor may request records for the two prior years to determine if the same issues exist. Obtaining CRA audit help early can help you contain the scope of the inquiry and prevent further expansion into your historical records.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26 years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400 clients.

Frequently Asked Questions

Common Triggers for a CRA Review in 2026

The CRA's automated systems are now highly efficient at spotting discrepancies between what you report and the information submitted by third parties. If the figures on your T4 or T5 slips don't match your return exactly, a computer-generated flag is almost certain. Another major trigger involves claiming unusual or high-value business deductions that seem out of proportion to your industry's averages. Finally, a consistent history of late filing or previous compliance issues creates a "risk profile" that makes you a frequent candidate for scrutiny. Staying organized isn't just about efficiency; it's about staying off the CRA's high-risk list.

Emerging Focus Areas: Crypto and Real Estate

In 2026, the CRA is paying closer attention to digital asset transactions than ever before. Sophisticated data-sharing agreements with major exchanges mean that cryptocurrency gains are no longer invisible to tax authorities. If you've been active in the crypto market, you must ensure your cost-basis tracking is precise. Similarly, the real estate sector remains a top priority for enforcement. Auditors are specifically looking for "shadow flipping" or the improper use of the principal residence exemption to avoid capital gains tax. If you're involved in property transactions, reviewing the CRA audit risks for real estate can help you understand how to document these complex sales properly. Professional CRA audit help can provide the foresight needed to address these emerging sectors before an auditor initiates contact. An audit isn't a single event but a structured sequence of interactions. It begins when a "Notice of Audit" or "Letter of Inquiry" arrives in your mailbox or appears in your My Business Account. This initial contact defines the scope of the review. Your first response is vital because it sets the professional tone for the entire engagement. Being prompt and organized suggests that your books are in order, which can sometimes limit the auditor's desire to dig deeper into unrelated fiscal years. If the process feels overwhelming, connecting with our team can help you prepare your records effectively before the first meeting. During the examination phase, the auditor scrutinizes your bank statements, receipts, and journals. Understanding the official CRA audit process helps you anticipate their moves. They're looking for evidence that supports the numbers you reported. If they find discrepancies, they won't issue a bill immediately. Instead, they'll send a "Proposal Letter." This document outlines the changes they intend to make and provides a final opportunity for you to present missing evidence. Professional CRA audit help is particularly valuable during this examination phase to ensure the auditor's findings are based on a complete and accurate understanding of your financial history.

The Information Request and Documentation Phase

The auditor will issue a Request for Information (RFI) that lists the specific documents they need to see. It's a common mistake to provide more information than what was explicitly requested. Doing so can inadvertently open new lines of inquiry that weren't part of the original scope. You should organize your digital and physical records to match the auditor's list exactly. This methodical approach facilitates a smoother review and demonstrates that you're acting in good faith. Clear, indexed records often lead to a faster resolution and fewer follow-up questions.

Responding to Proposed Reassessments

Once the auditor completes their review, they issue a proposal letter if they intend to change your tax return. You generally have a 30-day window to respond to this letter before it becomes final. This is your most critical opportunity for negotiation. You must craft a professional rebuttal supported by specific references to the Income Tax Act or relevant tax court cases. A CPA can often negotiate these adjustments down by identifying expenses the auditor may have overlooked or misinterpreted. If no rebuttal is sent, the CRA will issue a final Notice of Reassessment, which triggers the 7% interest rate on any balance owing as of July 2026. Facing a CRA auditor alone can feel like stepping into a courtroom without a lawyer. While the law allows you to represent yourself, the psychological toll of direct confrontation often leads to costly errors. Professional CRA audit help provides a vital buffer. It transforms what could be a high-stakes interrogation into a structured, technical exchange of facts. By appointing an authorized representative through the CRA's My Business Account, you delegate the technical heavy lifting to an expert who understands the nuances of the Income Tax Act. This shield allows you to focus on your business while we handle the scrutiny. Most taxpayers aren't trained in the specific art of the audit. Under pressure, it's remarkably easy to volunteer information that wasn't requested. This inadvertent disclosure can lead an auditor to expand their review into other tax years or unrelated business activities. An expert ensures that the scope remains narrow and focused. When weighing professional fees, you must consider the potential for significant long-term savings. A well-managed audit often leads to reduced reassessments and helps you avoid harsh penalties, such as the 50% gross negligence penalty for understated tax. It's an investment in protecting your financial future from avoidable interest and adjustments.

Why Direct Communication with Auditors Can Be Risky

The auditor’s primary mandate is to verify compliance. They aren't looking for ways to lower your tax bill or find missed deductions. Casual comments about your personal lifestyle or business habits might be misinterpreted as admissions of negligence or intent. For CRA filers, every word carries weight. Ensuring all communication is written and precisely focused on the audit scope creates a clear, defensible paper trail. This level of precision prevents the auditor from making assumptions based on off-hand remarks or incomplete explanations.

The Role of a CPA as a Proactive Guardian

A CPA does more than just hand over folders of receipts. They translate your internal accounting records into the specific formats the CRA prefers, which reduces friction during the review. If the auditor makes a logical leap or a calculation error, your representative is there to challenge it immediately with professional authority. They manage the auditor’s expectations regarding timelines and data delivery, ensuring you aren't rushed into providing incomplete or unverified records. This proactive stance positions you as an organized and compliant taxpayer, which often leads to a more favourable and efficient resolution. In a Canadian tax audit, the legal landscape differs significantly from other areas of law. The burden of proof rests squarely on your shoulders. Under the Income Tax Act, the CRA's assumptions are considered correct until you provide documentation that proves otherwise. This reality makes thorough record-keeping your most powerful tool. By law, you must retain all relevant records for a minimum of six years from the end of the last tax year they relate to. If you find yourself missing specific receipts, professional CRA audit help can assist in reconstructing your history through bank statements or third-party affidavits. We often recommend maintaining contemporaneous documentation, which are notes made at the exact time of a transaction, as these carry significant weight with auditors during a review. Reconstructing a financial narrative from years ago is a daunting task. Auditors look for a clear, unbroken trail from your bank account to your general ledger. If there are gaps in your story, the auditor is permitted to make "reasonable" assumptions, which rarely favour the taxpayer. Having a proactive guardian to help you assemble these pieces ensures that your defense is built on facts rather than estimates. Organized records don't just win audits; they often shorten the duration of the investigation by giving the auditor exactly what they need in a format they can easily verify.

Essential Records for a Business Audit

Auditors expect your general ledgers, purchase invoices, and sales receipts to be readily available. You'll also need to produce corporate minute books and evidence of business-related travel or entertainment, such as logs or calendars. A frequent area of scrutiny for CRA filers involves GST/HST input tax credits (ITCs). To claim these, you must have valid invoices that include the supplier's GST/HST registration number. If your records are currently disorganized, it's best to connect with our team to ensure your files are audit-ready before the CRA's deadline.

Managing Deadlines and Extension Requests

The CRA typically sets tight deadlines for information requests, often giving taxpayers only 30 days to comply. If your files are complex or archived, you can request an extension, but you must do so before the original deadline expires. It's vital to confirm all extensions in writing to avoid "failure to comply" penalties. You should also be aware of the "statute-barred" period. Generally, the CRA can only reassess a return within three years of the date on your original Notice of Assessment. However, if they suspect fraud or misrepresentation, this limit is waived. Navigating these timelines requires precision and foresight to ensure you don't inadvertently waive your rights or miss a critical rebuttal window. Experience is the most valuable asset when facing federal scrutiny. Tax Partners leverages over 40 years of institutional wisdom to manage complex CRA audit files with a level of precision that smaller firms cannot match. We don't believe in a reactive or defensive posture. Instead, we employ a methodical approach that begins with an intensive file review to identify every potential vulnerability before the auditor ever asks a question. This foresight allows us to present your financial narrative with professional clarity, ensuring that your rights remain protected throughout the entire interaction. For CRA filers, having this level of expertise is the difference between a stressful ordeal and a controlled, technical verification. Our team acts as a steady hand at the helm, alleviating the heavy emotional and administrative burden of an investigation. We serve as your proactive guardian, managing all correspondence and acting as the primary point of contact for the CRA. As a national firm, we possess a deep understanding of the specific nuances within various Canadian industries, from emerging digital sectors to established real estate markets. This breadth of knowledge ensures that we can defend your position effectively by speaking the auditor's language. When you seek our CRA audit help, you gain a long-term partner dedicated to your financial steadfastness and ethical compliance.

Bespoke Audit Management Strategies

We develop customized preparation plans tailored to your specific industry and the unique triggers that led to your selection. Our experts engage in direct negotiation with CRA auditors to resolve disputes at the examination stage, which often prevents a file from escalating into a more punitive phase. We don't just look at the current year; we conduct a comprehensive review of your entire filing history to identify and mitigate potential future risks. This strategic oversight ensures that your business remains a low-priority target for future interventions.

Beyond the Audit: Long-Term Compliance and Wealth Preservation

A successful audit resolution should serve as a foundation for future stability. We help you implement robust bookkeeping and payroll systems that prevent the common clerical errors that often trigger CRA reviews. Beyond immediate compliance, our wealth management and financial planning services are designed to ensure you keep more of what you earn under Canadian law. We look ahead to secure your better outcome by combining modern accounting practices with decades of regulatory experience. Contact Tax Partners for a confidential audit consultation today. Navigating a CRA audit requires more than just compliance; it demands a strategic defence built on organized records and technical expertise. You've learned that the burden of proof rests on your shoulders. The first 30 days after receiving a proposal letter are your most critical window for negotiation. By maintaining meticulous documentation for at least six years, you create a foundation of transparency that simplifies the review process. Professional CRA audit help ensures that your case is presented with precision while shielding you from the stress of direct negotiation. With over 40 years of Canadian tax experience and more than 495,000 returns filed, our team brings a legacy of reliability to your file. Our 1,390+ five-star Google reviews reflect our commitment to acting as a proactive guardian for our clients. Speak with a CPA about your CRA audit today to regain total control over your tax situation. We're here to guide you toward a fair resolution with confidence.

How long does the CRA have to audit my tax return?

Under Canadian tax rules, the CRA generally has three years from the date of your original Notice of Assessment to reassess your return. This is known as the normal reassessment period. However, this limit is waived if the CRA suspects fraud or misrepresentation due to neglect or carelessness. In those cases, they can audit much further back. It's best to check your specific assessment dates to confirm your current status.

What happens if I cannot find the receipts the CRA is asking for?

If you cannot locate specific receipts, you must provide alternative evidence to support your claims. The CRA may accept bank statements, cancelled cheques, or written affidavits from third parties as secondary proof. However, without a formal receipt, the auditor has the discretion to disallow the expense entirely. Seeking professional CRA audit help can assist you in reconstructing your records to satisfy the auditor's requirements and protect your interests.

Can the CRA freeze my bank account during an audit?

No, the CRA typically does not freeze bank accounts during the audit phase itself. Freezing an account is a collection action that usually occurs only after a final Notice of Reassessment has been issued and the taxpayer has failed to pay the resulting debt. During the audit, the focus remains on verifying your books and records rather than seizing assets. Collections only begin once the tax liability is finalized.

What is the difference between a desk audit and a field audit?

A desk audit is a limited review conducted through correspondence where the auditor requests specific documents by mail or via your My Account portal. A field audit is much more comprehensive and involves an auditor visiting your home or place of business to examine your entire financial history. Field audits are typically reserved for complex files or business owners with high-value revenue streams that require on-site verification.

Do I have to meet the CRA auditor at my home or place of business?

You are not legally required to host the auditor at your personal residence if you have a representative. While the CRA may request an on-site visit to verify business operations, these meetings can often be held at your accountant's office instead. This provides a professional environment and ensures the auditor only has access to the specific records relevant to the current inquiry. It also minimizes disruption to your daily routine.

What should I do if I disagree with the CRA’s final reassessment?

You have the right to challenge a reassessment by filing a formal Notice of Objection. For most individual filers, this must be done within 90 days of the date on your Notice of Reassessment. This step initiates an independent review by the CRA’s Appeals Division. It's a critical process for taxpayers who believe the auditor made a logical or legal error during the examination and want a second opinion.

Will the CRA audit my previous years if they find an error in this year?

Yes, the CRA can expand an audit to previous years if they discover significant or recurring errors in the year under review. If a mistake appears to be part of a systemic pattern, the auditor may request records for the two prior years to determine if the same issues exist. Obtaining CRA audit help early can help you contain the scope of the inquiry and prevent further expansion into your historical records.