FBAR Filing Requirements: A Guide for Canadians with US Ties

Could a single Canadian savings account or a forgotten TFSA really trigger a $16,536 penalty from the IRS? For many Canadians with U.S. citizenship or residency, the reality of fbar filing requirements often feels like a looming shadow over their financial peace of mind. It's perfectly natural to feel overwhelmed by the prospect of reporting your local bank accounts to a foreign government. You've worked hard to organize your finances, and the last thing you want is for a technicality to put your savings at risk.

We're here to help you master these complexities and ensure your cross-border interests remain fully compliant under IRS and FinCEN rules. This guide provides a clear roadmap through the filing process, from understanding the $10,000 aggregate threshold to identifying which specific Canadian accounts you must report. We'll examine the April 15, 2026, deadline and the automatic extension to October, giving you the clarity and foresight needed to secure your financial future with confidence.

Key Takeaways

- Identify your status as a "U.S. Person" to understand why your Canadian residency may still trigger reporting obligations under IRS rules.

- Master the fbar filing requirements by learning how to aggregate the maximum value of your Canadian bank, investment, and insurance accounts into U.S. dollars.

- Distinguish between the Treasury Department's FinCEN Form 114 and your standard IRS tax filings to ensure total cross-border transparency.

- Recognize the importance of the April 15 deadline and the automatic extension to October 15 for maintaining compliance without unnecessary stress.

- Learn how to utilize the Streamlined Foreign Offshore Procedures to correct past filing omissions and regain your financial peace of mind.

What is the FBAR? Understanding Your Transparency Obligations

FBAR stands for the Report of Foreign Bank and Financial Accounts. It is filed electronically through FinCEN Form 114. While many people associate it with their annual tax return, it's actually a transparency requirement rather than a tax. Under IRS rules, you must file this form if you meet specific thresholds, regardless of whether your accounts earned a single cent of interest. The goal is simple. The U.S. government wants to prevent money laundering and ensure a clear view of the worldwide assets held by its citizens. This is a disclosure tool used by the Treasury Department to monitor financial flows across borders.

You may feel that reporting your local Canadian savings is an overreach. However, the U.S. government views this information as vital for national security and financial integrity. Compliance isn't about paying more tax; it's about providing the transparency that the U.S. government demands from all its citizens, no matter where they choose to live or work. Establishing this baseline of honesty helps protect you from the severe penalties associated with non-disclosure.

The Legal Framework: IRS vs. FinCEN

The legislative foundation of this requirement is the Bank Secrecy Act (BSA). This act empowers the Financial Crimes Enforcement Network (FinCEN) to collect data on foreign financial interests. While the IRS handles the day-to-day administration and enforcement of these rules, the form itself belongs to the Treasury Department's FinCEN division. This distinction is vital because it means the fbar filing requirements exist independently of your income tax obligations. You might also hear about Form 8938 under the Foreign Account Tax Compliance Act (FATCA). While both forms report foreign assets, they have different thresholds and reporting rules. Being a U.S. person living in Toronto or Vancouver does not exempt you. It actually places you right at the centre of these regulations.

Why "Foreign" Includes Your Canadian Accounts

The term "foreign" can be confusing when you've lived in Canada for decades. From the perspective of the U.S. government, any financial account located outside the 50 states, the District of Columbia, or U.S. territories is considered foreign. If you hold a chequing account at TD Canada Trust or a savings account at RBC, those are foreign accounts under IRS rules. Many Canadians with U.S. ties mistakenly believe that because they pay Canadian taxes and reside in Canada, their local accounts are domestic. This is a dangerous assumption. The U.S. tax system is based on citizenship, not just residency. Your Canadian accounts are exactly what the U.S. Treasury wants to see on your FinCEN Form 114 to ensure full compliance with fbar filing requirements.

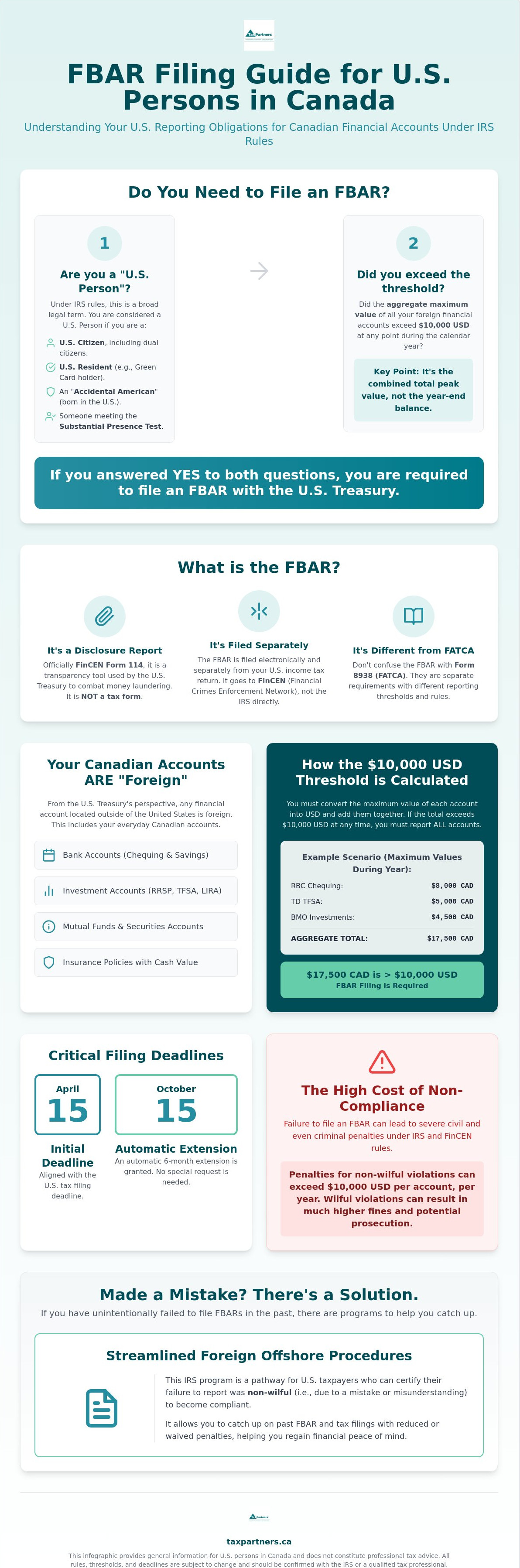

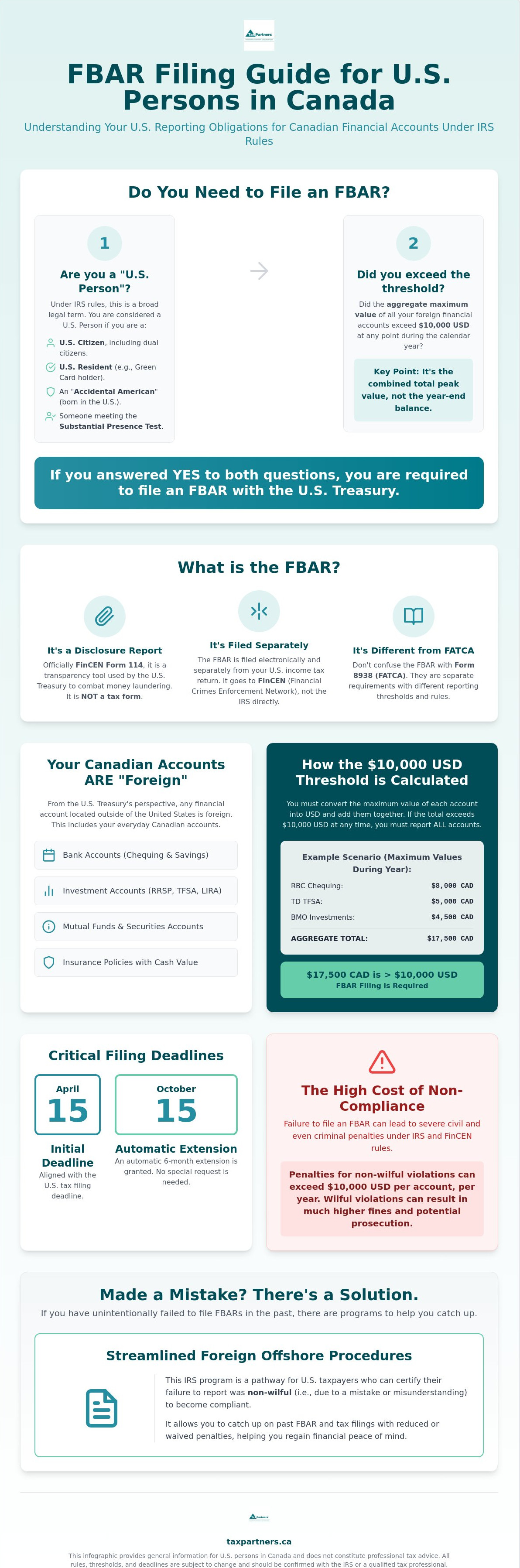

Determining Your Status: Who Qualifies as a 'US Person'?

Under IRS rules, the term "U.S. person" is a legal designation that extends far beyond those currently living within American borders. It encompasses U.S. citizens, even if they hold dual nationality, and U.S. residents, such as Green Card holders. This status also applies to domestic entities, including corporations, partnerships, and trusts created or organized under U.S. law. The IRS FBAR Information Page provides a foundational look at these categories, but the nuances for Canadians are often more complex than they first appear.

Many people fall into the category of "Accidental Americans." These are individuals born in the United States to Canadian parents who returned to Canada shortly after the birth. Despite having never worked or lived in the U.S. as an adult, the IRS considers them citizens with full fbar filing requirements. Similarly, the Substantial Presence Test can catch frequent travellers off guard. If you spend enough time in the U.S. over a three-year period, you may be treated as a resident for tax and reporting purposes. It's a mathematical formula that requires careful tracking of your days spent south of the border.

Dual Citizenship and Residency Realities

Holding a Canadian passport does not negate your obligations to the U.S. government. The IRS operates on a citizenship-based tax system, which is a significant departure from the residency-based system used by the CRA. Even if you have no intention of ever moving back to the States, your reporting duties remain mandatory. Today, compliance is harder to ignore. Under international agreements, Canadian financial institutions share information about accounts held by U.S. persons directly with the IRS. This transparency makes it easier for the government to identify those who haven't met their obligations. If you're feeling uncertain about your status, consulting with a cross-border expert can help you navigate these waters safely.

Business Entities and Signature Authority

This is where many Canadian small business owners and professionals face unexpected challenges. You must report any foreign financial account where you have "signature authority," even if you have no financial interest in the money itself. For example, if you're a director of a Canadian corporation and have the power to control the company's bank accounts, you must disclose those accounts on your personal FinCEN Form 114. This rule also applies if you manage accounts for an elderly family member or act as a trustee. Meticulous bookkeeping is essential here. You need to track the highest balance of these accounts throughout the year to ensure you're meeting the fbar filing requirements accurately. Proactive management of these records is the best way to prevent stress when the filing deadline approaches.

The $10,000 Threshold and Reportable Canadian Accounts

The most critical figure to remember regarding fbar filing requirements is $10,000 USD. This is an aggregate threshold, meaning it applies to the combined total of all your foreign financial accounts. If the sum of these accounts exceeds $10,000 USD at any single point during the calendar year, you must file. It's a common pitfall to assume this limit applies to each account individually. In reality, if you hold ten separate Canadian accounts with $1,100 in each, you have surpassed the limit and must report all ten. Under IRS rules, even a brief spike in your balance, perhaps from a temporary transfer or a house sale deposit, can trigger this obligation.

Calculating this total requires precision. You must convert your Canadian dollar balances into U.S. dollars using the official Treasury reporting rates of exchange. Because exchange rates fluctuate, a balance that seems safe in January might cross the threshold by July. We recommend keeping a meticulous record of the maximum value reached in every account throughout the year. For detailed guidance on the electronic submission process, you can consult the FinCEN FBAR Filing Information portal. Maintaining these records ensures you aren't caught off guard by currency shifts or aggregate totals.

Which Canadian Accounts Must Be Reported?

Under IRS rules, the definition of a "financial account" is quite broad. It includes standard chequing and savings accounts, but it also extends to brokerage accounts, mutual funds, and even some life insurance policies with a cash value. For U.S. persons in Canada, registered accounts are a primary focus. Your Registered Retirement Savings Plan (RRSP) and Registered Retirement Income Fund (RRIF) are generally reportable. You should also be wary of the "TFSA Trap." While the Tax-Free Savings Account (TFSA) and the Registered Education Savings Plan (RESP) offer tax benefits in Canada, they are fully reportable on an FBAR and often require additional, more complex disclosures to remain compliant with U.S. regulations.

Non-Reportable Accounts and Exceptions

Not every asset you own in Canada falls under fbar filing requirements. Physical assets held directly, such as real estate or a collection of gold coins stored in a home safe, are typically not reportable on FinCEN Form 114. Similarly, Canadian Social Security or government-owned accounts generally don't require disclosure. There are also rare exceptions for certain retirement plans where a U.S. custodian is involved, though this is uncommon for those living and working primarily in Canada. While these exceptions provide some relief, the safest approach is to review your entire portfolio to ensure no financial account has been overlooked. Clear documentation is your best defence against the stress of an audit.

Critical Deadlines and the Cost of Non-Compliance

Timing is everything when it comes to cross-border transparency. The primary deadline for filing FinCEN Form 114 is April 15. This date is intentionally aligned with the standard 1040 tax filing for Canadians, making it easier to manage your U.S. obligations in a single window. If you miss this spring date, don't panic. Under IRS rules, all filers receive an automatic extension to October 15. You don't need to file a formal request or jump through administrative hoops to secure this extra time. It's a built-in safety net designed to help you gather the necessary data from your Canadian financial institutions.

However, missing these deadlines entirely or filing inaccurate information carries heavy risks. The cost of non-compliance is steep. For non-willful violations, where a filer simply wasn't aware of the fbar filing requirements, the penalty can reach $16,536 per report. If the IRS determines a violation was "willful," the stakes escalate dramatically. These penalties can be the greater of $165,353 or 50% of the account balance at the time of the violation. Recent court rulings have even expanded the definition of willfulness to include "reckless disregard," meaning that simply ignoring the rules can lead to life-altering financial consequences.

The Risk of an IRS Audit for Canadians

The days of financial anonymity are over. Under the Foreign Account Tax Compliance Act (FATCA), Canadian banks share information about U.S. account holders directly with the IRS. This data makes it easier for the government to flag non-filers and initiate audits. You should also be aware that the statute of limitations for FBAR violations is generally six years. This gives the IRS a long window to look back at your financial history. Claiming you didn't know about the rules is a fragile defence in an era where cross-border compliance information is readily accessible. If you're concerned about your past filings, reach out to our cross-border specialists to discuss your options for coming forward.

Record-Keeping Best Practices

Staying organized is your best protection against IRS scrutiny. Under IRS rules, you're required to maintain records of your foreign accounts for at least five years. We recommend creating a centralized, digital system to track the essential details for every reportable account. This includes the name on the account, the account number, the name and address of the Canadian bank, and the peak balance reached during the calendar year. Regular reviews of your cross-border status with a professional ensure that your record-keeping stays sharp. This proactive approach transforms a stressful annual task into a routine part of your wealth management strategy.

Solving Past Mistakes: Catching Up with Streamlined Procedures

Realizing you've missed years of filings can be a source of significant anxiety. For many Canadians, especially those who only recently discovered their "U.S. person" status, the fear of retroactive penalties is real. The IRS provides a specific relief program known as the Streamlined Foreign Offshore Procedures. This program is designed for taxpayers whose failure to meet fbar filing requirements was non-willful. In this context, non-willful means your conduct was due to negligence, inadvertence, or a simple mistake based on a good-faith misunderstanding of the law.

The primary benefit of this program is the potential to avoid all FBAR-related penalties. By coming forward voluntarily, you demonstrate a commitment to transparency that the U.S. government values. This process requires a detailed narrative statement explaining why you didn't file in the past. Crafting this statement requires precision and honesty. It is your opportunity to tell your story and secure your financial standing. Professional guidance is essential here to ensure your narrative meets the specific standards required under IRS rules.

The Eligibility Criteria for Canadians

To qualify for this relief, you must meet specific residency requirements. Under IRS rules, you must not have had a "U.S. abode" during the period in question and must have been physically outside the United States for a required duration. The program requires you to file the last three years of delinquent tax returns and the last six years of FBARs. If you lack the necessary identification to start this process, we offer a specialized ITIN application service in Canada to help you obtain your Individual Taxpayer Identification Number securely.

Why Professional Oversight is Essential

Navigating a disclosure program is not a task to handle alone. A specialized CPA firm acts as a proactive guardian, ensuring every figure is accurate and every form is complete. Precision is your best defence against further IRS scrutiny. One small error in your aggregate balance calculations could trigger the very audit you're trying to resolve. It's also vital to act quickly. Eligibility for these relief programs usually disappears once the IRS contacts you or begins an investigation. Taking the first step now puts you back in control of your cross-border journey and ensures your fbar filing requirements are met with total accuracy.

Secure Your Cross-Border Financial Future

Mastering the fbar filing requirements is more than just a regulatory hurdle; it's a vital step in protecting your Canadian assets and maintaining your long-term financial stability. Whether you're an "accidental American" or a long-term resident, the path to compliance is paved with precision and proactive planning. By identifying your reportable accounts and meeting the April 15 deadline, you move from a state of uncertainty to one of total control. If you've fallen behind, programs like the Streamlined Foreign Offshore Procedures offer a clear way forward without the weight of life-altering penalties.

At Tax Partners, we bring over 40 years of cross-border tax expertise to every client relationship. With more than 495,000 returns filed and 1,390 five-star Google reviews, our team acts as your dedicated guardian in a complex regulatory landscape. We understand the stress of dual-country compliance and are here to provide the steady hand you need. Secure your cross-border compliance with a professional FBAR consultation at Tax Partners today. Let's work together to ensure your financial interests remain safe, transparent, and fully compliant for years to come.

Frequently Asked Questions

Do I need to file an FBAR if my Canadian account has less than $10,000?

You only avoid filing if the aggregate total of all your foreign financial accounts remained below $10,000 USD throughout the entire year. If you hold three accounts with $4,000 each, your combined total is $12,000, which triggers the requirement to report every account. Under IRS rules, the threshold is based on the total maximum value of all accounts, not the balance of a single one.

What is the penalty for not filing an FBAR while living in Canada?

Penalties are divided into non-willful and willful categories under Treasury Department regulations. A non-willful violation can result in a penalty of up to $16,536 per year. If the IRS determines the failure was willful, the fine can escalate to the greater of $165,353 or 50% of the account balance. These figures are adjusted annually for inflation and represent a significant financial risk for non-compliant filers.

Are Canadian RRSPs and TFSAs reportable on the FBAR?

Yes, both Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs) are considered reportable foreign financial accounts. While these accounts provide tax benefits under Canadian law, they don't enjoy the same status under IRS rules for disclosure purposes. You must include their maximum annual values on your FinCEN Form 114 to ensure you're meeting all transparency obligations for your Canadian holdings.

Can I file my FBAR and US tax return together?

No, you must file these documents separately because they are processed by different government agencies. Your U.S. income tax return is submitted to the IRS, while the FBAR is filed electronically with the Financial Crimes Enforcement Network (FinCEN). Although the deadlines are often the same, they require distinct submission processes through different online portals to remain fully compliant with U.S. law.

What is the FBAR deadline for the 2026 tax year?

The primary deadline to meet your fbar filing requirements for the 2025 calendar year is April 15, 2026. If you miss this date, you're granted an automatic extension to October 15, 2026. You don't need to file any specific forms to receive this extension. This timeline ensures you have sufficient time to gather maximum balance information from your Canadian financial institutions.

What happens if I have signature authority over my employer’s Canadian bank account?

You must report any account where you have signature authority, even if you have no personal financial interest in the money. Under IRS rules, the power to control the disposition of funds is enough to trigger a reporting duty. This commonly affects Canadian residents who serve as corporate officers or employees with signing power over their company's operational bank accounts.

Is there a way to catch up on years of missed FBAR filings without huge penalties?

Yes, the IRS provides the Streamlined Filing Compliance Procedures for taxpayers who can certify that their previous failure to file was non-willful. This program allows you to come forward voluntarily by submitting six years of FBARs and three years of amended tax returns. It's a proactive path to meeting fbar filing requirements while significantly reducing or even eliminating the threat of standard non-compliance penalties.

Does the CRA share my Canadian bank account information with the IRS?

Yes, the CRA shares specific financial data with the IRS under the Intergovernmental Agreement for the implementation of FATCA. Canadian banks are required to identify accounts held by U.S. persons and provide that information to the CRA for exchange with U.S. authorities. This level of international cooperation means the IRS has a clear window into Canadian accounts, making voluntary compliance more important than ever.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Frequently Asked Questions

The Legal Framework: IRS vs. FinCEN

The legislative foundation of this requirement is the Bank Secrecy Act (BSA). This act empowers the Financial Crimes Enforcement Network (FinCEN) to collect data on foreign financial interests. While the IRS handles the day-to-day administration and enforcement of these rules, the form itself belongs to the Treasury Department's FinCEN division. This distinction is vital because it means the fbar filing requirements exist independently of your income tax obligations. You might also hear about Form 8938 under the Foreign Account Tax Compliance Act (FATCA). While both forms report foreign assets, they have different thresholds and reporting rules. Being a U.S. person living in Toronto or Vancouver does not exempt you. It actually places you right at the centre of these regulations.

Why "Foreign" Includes Your Canadian Accounts

The term "foreign" can be confusing when you've lived in Canada for decades. From the perspective of the U.S. government, any financial account located outside the 50 states, the District of Columbia, or U.S. territories is considered foreign. If you hold a chequing account at TD Canada Trust or a savings account at RBC, those are foreign accounts under IRS rules. Many Canadians with U.S. ties mistakenly believe that because they pay Canadian taxes and reside in Canada, their local accounts are domestic. This is a dangerous assumption. The U.S. tax system is based on citizenship, not just residency. Your Canadian accounts are exactly what the U.S. Treasury wants to see on your FinCEN Form 114 to ensure full compliance with fbar filing requirements. Under IRS rules, the term "U.S. person" is a legal designation that extends far beyond those currently living within American borders. It encompasses U.S. citizens, even if they hold dual nationality, and U.S. residents, such as Green Card holders. This status also applies to domestic entities, including corporations, partnerships, and trusts created or organized under U.S. law. The IRS FBAR Information Page provides a foundational look at these categories, but the nuances for Canadians are often more complex than they first appear. Many people fall into the category of "Accidental Americans." These are individuals born in the United States to Canadian parents who returned to Canada shortly after the birth. Despite having never worked or lived in the U.S. as an adult, the IRS considers them citizens with full fbar filing requirements. Similarly, the Substantial Presence Test can catch frequent travellers off guard. If you spend enough time in the U.S. over a three-year period, you may be treated as a resident for tax and reporting purposes. It's a mathematical formula that requires careful tracking of your days spent south of the border.

Dual Citizenship and Residency Realities

Holding a Canadian passport does not negate your obligations to the U.S. government. The IRS operates on a citizenship-based tax system, which is a significant departure from the residency-based system used by the CRA. Even if you have no intention of ever moving back to the States, your reporting duties remain mandatory. Today, compliance is harder to ignore. Under international agreements, Canadian financial institutions share information about accounts held by U.S. persons directly with the IRS. This transparency makes it easier for the government to identify those who haven't met their obligations. If you're feeling uncertain about your status, consulting with a cross-border expert can help you navigate these waters safely.

Business Entities and Signature Authority

This is where many Canadian small business owners and professionals face unexpected challenges. You must report any foreign financial account where you have "signature authority," even if you have no financial interest in the money itself. For example, if you're a director of a Canadian corporation and have the power to control the company's bank accounts, you must disclose those accounts on your personal FinCEN Form 114. This rule also applies if you manage accounts for an elderly family member or act as a trustee. Meticulous bookkeeping is essential here. You need to track the highest balance of these accounts throughout the year to ensure you're meeting the fbar filing requirements accurately. Proactive management of these records is the best way to prevent stress when the filing deadline approaches. The most critical figure to remember regarding fbar filing requirements is $10,000 USD. This is an aggregate threshold, meaning it applies to the combined total of all your foreign financial accounts. If the sum of these accounts exceeds $10,000 USD at any single point during the calendar year, you must file. It's a common pitfall to assume this limit applies to each account individually. In reality, if you hold ten separate Canadian accounts with $1,100 in each, you have surpassed the limit and must report all ten. Under IRS rules, even a brief spike in your balance, perhaps from a temporary transfer or a house sale deposit, can trigger this obligation. Calculating this total requires precision. You must convert your Canadian dollar balances into U.S. dollars using the official Treasury reporting rates of exchange. Because exchange rates fluctuate, a balance that seems safe in January might cross the threshold by July. We recommend keeping a meticulous record of the maximum value reached in every account throughout the year. For detailed guidance on the electronic submission process, you can consult the FinCEN FBAR Filing Information portal. Maintaining these records ensures you aren't caught off guard by currency shifts or aggregate totals.

Which Canadian Accounts Must Be Reported?

Under IRS rules, the definition of a "financial account" is quite broad. It includes standard chequing and savings accounts, but it also extends to brokerage accounts, mutual funds, and even some life insurance policies with a cash value. For U.S. persons in Canada, registered accounts are a primary focus. Your Registered Retirement Savings Plan (RRSP) and Registered Retirement Income Fund (RRIF) are generally reportable. You should also be wary of the "TFSA Trap." While the Tax-Free Savings Account (TFSA) and the Registered Education Savings Plan (RESP) offer tax benefits in Canada, they are fully reportable on an FBAR and often require additional, more complex disclosures to remain compliant with U.S. regulations.

Non-Reportable Accounts and Exceptions

Not every asset you own in Canada falls under fbar filing requirements. Physical assets held directly, such as real estate or a collection of gold coins stored in a home safe, are typically not reportable on FinCEN Form 114. Similarly, Canadian Social Security or government-owned accounts generally don't require disclosure. There are also rare exceptions for certain retirement plans where a U.S. custodian is involved, though this is uncommon for those living and working primarily in Canada. While these exceptions provide some relief, the safest approach is to review your entire portfolio to ensure no financial account has been overlooked. Clear documentation is your best defence against the stress of an audit. Timing is everything when it comes to cross-border transparency. The primary deadline for filing FinCEN Form 114 is April 15. This date is intentionally aligned with the standard 1040 tax filing for Canadians, making it easier to manage your U.S. obligations in a single window. If you miss this spring date, don't panic. Under IRS rules, all filers receive an automatic extension to October 15. You don't need to file a formal request or jump through administrative hoops to secure this extra time. It's a built-in safety net designed to help you gather the necessary data from your Canadian financial institutions. However, missing these deadlines entirely or filing inaccurate information carries heavy risks. The cost of non-compliance is steep. For non-willful violations, where a filer simply wasn't aware of the fbar filing requirements, the penalty can reach $16,536 per report. If the IRS determines a violation was "willful," the stakes escalate dramatically. These penalties can be the greater of $165,353 or 50% of the account balance at the time of the violation. Recent court rulings have even expanded the definition of willfulness to include "reckless disregard," meaning that simply ignoring the rules can lead to life-altering financial consequences.

The Risk of an IRS Audit for Canadians

The days of financial anonymity are over. Under the Foreign Account Tax Compliance Act (FATCA), Canadian banks share information about U.S. account holders directly with the IRS. This data makes it easier for the government to flag non-filers and initiate audits. You should also be aware that the statute of limitations for FBAR violations is generally six years. This gives the IRS a long window to look back at your financial history. Claiming you didn't know about the rules is a fragile defence in an era where cross-border compliance information is readily accessible. If you're concerned about your past filings, reach out to our cross-border specialists to discuss your options for coming forward.

Record-Keeping Best Practices

Staying organized is your best protection against IRS scrutiny. Under IRS rules, you're required to maintain records of your foreign accounts for at least five years. We recommend creating a centralized, digital system to track the essential details for every reportable account. This includes the name on the account, the account number, the name and address of the Canadian bank, and the peak balance reached during the calendar year. Regular reviews of your cross-border status with a professional ensure that your record-keeping stays sharp. This proactive approach transforms a stressful annual task into a routine part of your wealth management strategy. Realizing you've missed years of filings can be a source of significant anxiety. For many Canadians, especially those who only recently discovered their "U.S. person" status, the fear of retroactive penalties is real. The IRS provides a specific relief program known as the Streamlined Foreign Offshore Procedures. This program is designed for taxpayers whose failure to meet fbar filing requirements was non-willful. In this context, non-willful means your conduct was due to negligence, inadvertence, or a simple mistake based on a good-faith misunderstanding of the law. The primary benefit of this program is the potential to avoid all FBAR-related penalties. By coming forward voluntarily, you demonstrate a commitment to transparency that the U.S. government values. This process requires a detailed narrative statement explaining why you didn't file in the past. Crafting this statement requires precision and honesty. It is your opportunity to tell your story and secure your financial standing. Professional guidance is essential here to ensure your narrative meets the specific standards required under IRS rules.

The Eligibility Criteria for Canadians

To qualify for this relief, you must meet specific residency requirements. Under IRS rules, you must not have had a "U.S. abode" during the period in question and must have been physically outside the United States for a required duration. The program requires you to file the last three years of delinquent tax returns and the last six years of FBARs. If you lack the necessary identification to start this process, we offer a specialized ITIN application service in Canada to help you obtain your Individual Taxpayer Identification Number securely.

Why Professional Oversight is Essential

Navigating a disclosure program is not a task to handle alone. A specialized CPA firm acts as a proactive guardian, ensuring every figure is accurate and every form is complete. Precision is your best defence against further IRS scrutiny. One small error in your aggregate balance calculations could trigger the very audit you're trying to resolve. It's also vital to act quickly. Eligibility for these relief programs usually disappears once the IRS contacts you or begins an investigation. Taking the first step now puts you back in control of your cross-border journey and ensures your fbar filing requirements are met with total accuracy. Mastering the fbar filing requirements is more than just a regulatory hurdle; it's a vital step in protecting your Canadian assets and maintaining your long-term financial stability. Whether you're an "accidental American" or a long-term resident, the path to compliance is paved with precision and proactive planning. By identifying your reportable accounts and meeting the April 15 deadline, you move from a state of uncertainty to one of total control. If you've fallen behind, programs like the Streamlined Foreign Offshore Procedures offer a clear way forward without the weight of life-altering penalties. At Tax Partners, we bring over 40 years of cross-border tax expertise to every client relationship. With more than 495,000 returns filed and 1,390 five-star Google reviews, our team acts as your dedicated guardian in a complex regulatory landscape. We understand the stress of dual-country compliance and are here to provide the steady hand you need. Secure your cross-border compliance with a professional FBAR consultation at Tax Partners today. Let's work together to ensure your financial interests remain safe, transparent, and fully compliant for years to come.

Do I need to file an FBAR if my Canadian account has less than $10,000?

You only avoid filing if the aggregate total of all your foreign financial accounts remained below $10,000 USD throughout the entire year. If you hold three accounts with $4,000 each, your combined total is $12,000, which triggers the requirement to report every account. Under IRS rules, the threshold is based on the total maximum value of all accounts, not the balance of a single one.

What is the penalty for not filing an FBAR while living in Canada?

Penalties are divided into non-willful and willful categories under Treasury Department regulations. A non-willful violation can result in a penalty of up to $16,536 per year. If the IRS determines the failure was willful, the fine can escalate to the greater of $165,353 or 50% of the account balance. These figures are adjusted annually for inflation and represent a significant financial risk for non-compliant filers.

Are Canadian RRSPs and TFSAs reportable on the FBAR?

Yes, both Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs) are considered reportable foreign financial accounts. While these accounts provide tax benefits under Canadian law, they don't enjoy the same status under IRS rules for disclosure purposes. You must include their maximum annual values on your FinCEN Form 114 to ensure you're meeting all transparency obligations for your Canadian holdings.

Can I file my FBAR and US tax return together?

No, you must file these documents separately because they are processed by different government agencies. Your U.S. income tax return is submitted to the IRS, while the FBAR is filed electronically with the Financial Crimes Enforcement Network (FinCEN). Although the deadlines are often the same, they require distinct submission processes through different online portals to remain fully compliant with U.S. law.

What is the FBAR deadline for the 2026 tax year?

The primary deadline to meet your fbar filing requirements for the 2025 calendar year is April 15, 2026. If you miss this date, you're granted an automatic extension to October 15, 2026. You don't need to file any specific forms to receive this extension. This timeline ensures you have sufficient time to gather maximum balance information from your Canadian financial institutions.

What happens if I have signature authority over my employer’s Canadian bank account?

You must report any account where you have signature authority, even if you have no personal financial interest in the money. Under IRS rules, the power to control the disposition of funds is enough to trigger a reporting duty. This commonly affects Canadian residents who serve as corporate officers or employees with signing power over their company's operational bank accounts.

Is there a way to catch up on years of missed FBAR filings without huge penalties?

Yes, the IRS provides the Streamlined Filing Compliance Procedures for taxpayers who can certify that their previous failure to file was non-willful. This program allows you to come forward voluntarily by submitting six years of FBARs and three years of amended tax returns. It's a proactive path to meeting fbar filing requirements while significantly reducing or even eliminating the threat of standard non-compliance penalties.

Does the CRA share my Canadian bank account information with the IRS?

Yes, the CRA shares specific financial data with the IRS under the Intergovernmental Agreement for the implementation of FATCA. Canadian banks are required to identify accounts held by U.S. persons and provide that information to the CRA for exchange with U.S. authorities. This level of international cooperation means the IRS has a clear window into Canadian accounts, making voluntary compliance more important than ever.