Business Incorporation Tax Advice: A Strategic Guide for Canadian Entrepreneurs in 2026

What if your business structure isn't just a legal shield, but a strategic vault designed to protect your hard-earned capital from unnecessary taxation? Many Canadian entrepreneurs view incorporation as a mere formality, yet seeking professional business incorporation tax advice is the first step toward true wealth preservation under CRA rules. You've likely felt the sting of high personal tax brackets as your revenue grows, or perhaps you've spent sleepless nights worrying about the complexity of payroll versus dividends. It's a common struggle, and you're right to seek a more stable path forward.

This guide provides the clarity you need to navigate the 2026 fiscal year with total confidence. We'll show you how to leverage the 9% federal small business tax rate and maximize deferrals to build a sustainable financial foundation. You'll learn exactly when your profits hit the threshold for incorporation, how to pay yourself efficiently, and how to ensure your corporate structure is fully CRA-compliant. As you realize your growth goals, we'll help you organize your corporate affairs to maintain a steady hand at the helm.

Key Takeaways

- Identify the specific profit thresholds where transitioning to a corporation provides the greatest tax relief for CRA filers.

- Learn how to leverage specialized business incorporation tax advice to access the 9% federal small business tax rate and maximize tax deferrals.

- Compare the long-term benefits of salary versus dividends to determine the most efficient way to pay yourself while managing CPP contributions.

- Simplify your regulatory journey by mastering the steps to register your Business Number and essential CRA program accounts for HST and payroll.

- Build a resilient financial legacy by understanding how to navigate TOSI rules and integrate estate planning into your business structure.

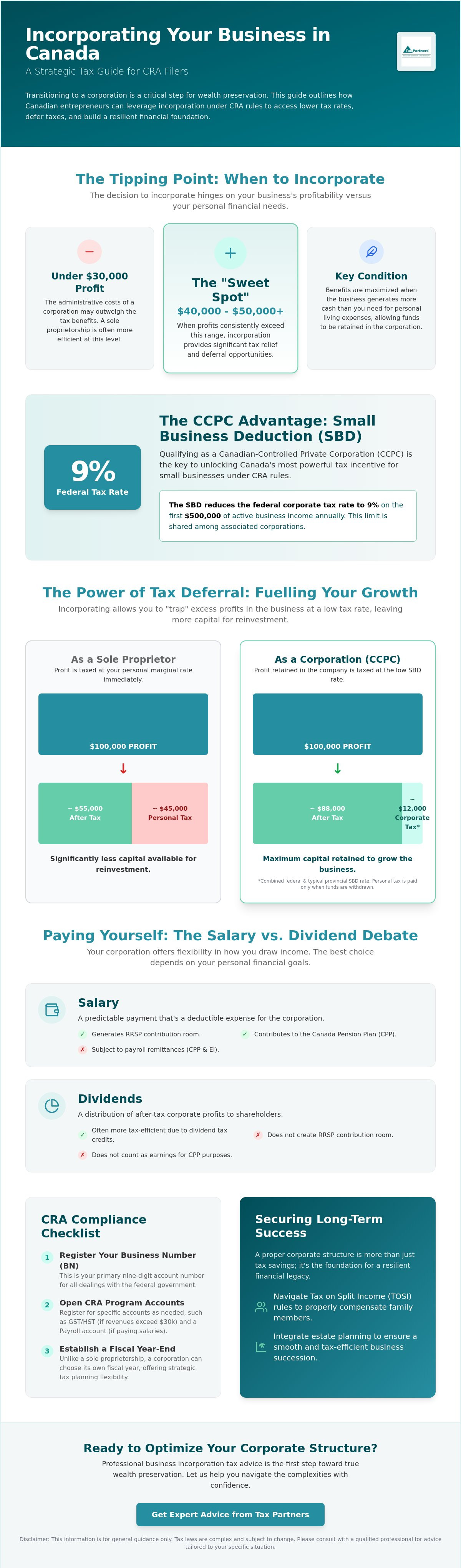

Determining When to Incorporate for Tax Benefits

Deciding the right moment to transition from a sole proprietorship to a corporation is a pivotal decision for any growing enterprise. For CRA filers, the primary driver is often the significant gap between personal marginal tax rates and the preferential rates available to small businesses. While every situation is unique, most financial professionals suggest that incorporation begins to offer tangible benefits when annual profits consistently exceed the $40,000 to $50,000 range. If your earnings remain below $30,000, the added administrative complexity and annual filing costs may not yet be justified. You need a steady hand at the helm to guide this transition.

Effective business incorporation tax advice focuses on the concept of tax integration. This principle ensures that the total tax paid, whether through a corporation or personally, remains relatively consistent. However, the true power of a corporation lies in its ability to act as a tax-deferred savings vehicle. By utilizing the Small Business Deduction (SBD), Canadian-controlled private corporations (CCPCs) can access a federal tax rate of just 9% on the first $500,000 of active business income in 2026. When combined with provincial rates, such as the Ontario rate scheduled to decrease to 2.2% in July 2026, the total tax burden on retained earnings is remarkably low. You can find more details on how these figures vary by province by reviewing current Corporate tax rates in Canada.

The Tipping Point: Income vs. Living Expenses

The financial advantage of incorporating hinges on your ability to leave "excess" profit within the business entity. If you require every dollar the business earns to cover your personal mortgage, groceries, and lifestyle, incorporation will offer limited tax relief. You'll simply pay personal tax on everything you withdraw. The strategy becomes effective when your business generates more cash than you need for daily life. By "trapping" these funds inside the corporation, you only pay the low corporate rate, allowing you to reinvest more capital back into your growth or a corporate investment portfolio. This foresight allows you to realize long-term wealth far more quickly than as a sole proprietor.

Personal Liability vs. Tax Flexibility

Beyond the well-known benefit of limited liability, a corporation introduces a distinct tax personality. Unlike a sole proprietorship, which must follow the calendar year, a corporation allows you to select a custom fiscal year-end. This flexibility is a powerful tool for tax planning. It lets you time the receipt of bonuses or dividends across different personal tax years to minimize your bracket. You gain the autonomy to choose between different types of income, such as salary or dividends, to optimize your personal cash flow while ensuring your corporate structure remains fully compliant with CRA regulations. This customized approach transforms your business from a simple job into a sophisticated financial engine.

Understanding the CCPC Advantage and Tax Deferral

To unlock the most significant advantages of the Canadian tax system, your business must qualify as a Canadian-Controlled Private Corporation (CCPC). Under CRA rules, a CCPC is generally a private corporation resident in Canada that isn't controlled by non-residents or public corporations. This status is the gateway to specialized business incorporation tax advice because it allows you to access the Small Business Deduction (SBD). Without this designation, your business income would be taxed at the general corporate rate, which is substantially higher. Protecting your CCPC status is a proactive step toward securing a more favourable financial outcome.

The Small Business Deduction (SBD) Explained

The SBD is a tax credit that reduces the federal portion of your corporate tax to 9% on the first $500,000 of active business income. Provinces also provide their own versions of this deduction to support local growth. For example, in 2026, Ontario is scheduled to lower its small business rate to 2.2% on July 1. It's vital to recognize that the $500,000 limit must be shared among associated corporations. If you own multiple businesses, you can't simply multiply the deduction. The CRA requires these entities to allocate the limit between them, ensuring the benefit remains targeted at genuine small enterprises.

How Tax Deferral Fuels Business Growth

Tax deferral is perhaps the most compelling reason to incorporate. Imagine your business earns $100,000 in profit that you don't need for personal expenses. If you're a sole proprietor in a high tax bracket, you might lose nearly half of that to personal income tax immediately. By contrast, a CCPC only pays the low small business rate, leaving roughly $88,000 available for reinvestment. This allows you to purchase inventory, upgrade equipment, or hire staff using dollars that would otherwise have gone to the CRA. You can explore the broader tax benefits of incorporation to see how these savings compound over time.

You must remain mindful of the passive income rules. The CRA limits the amount of investment income, such as interest or rent, a corporation can earn before the SBD begins to decrease. If your passive income exceeds $50,000 in a year, your access to the low small business rate starts to vanish. Managing this balance requires foresight and precision. If you're concerned about how these limits might impact your growth, it's wise to speak with a professional advisor to ensure your investments don't inadvertently trigger a higher tax bill.

Navigating the Salary vs. Dividend Debate

Choosing how to pay yourself is a fundamental part of business incorporation tax advice. The CRA views salary and dividends through the lens of "integration," a concept designed to ensure an individual pays roughly the same amount of tax regardless of the income's form. While the total tax bill might look similar on paper, the practical implications for your long-term wealth vary significantly. You're not just choosing a payment method; you're deciding on your retirement strategy and your immediate cash flow needs. Understanding corporate structure and tax obligations is essential here, as the corporation is a separate legal person that must account for these payments differently than a sole proprietorship.

One of the biggest factors in this debate is the Canada Pension Plan (CPP). When you pay yourself a salary, both you and your corporation must contribute to the CPP. This adds a layer of cost that many entrepreneurs find frustrating. However, salary is considered "earned income," which is the only way to generate Registered Retirement Savings Plan (RRSP) contribution room. If you plan to use an RRSP as a primary vehicle for retirement, a salary is non-negotiable. It provides a steady hand at the helm of your personal financial future.

The Case for a Regular Salary

A salary acts as a deductible expense for your corporation, reducing its taxable income. This is a straightforward way to manage your corporate tax bracket while ensuring you have a steady, predictable personal income. Because it's employment income, it also makes it easier to qualify for personal disability insurance or mortgages. You'll need to stay organized with source deductions and annual T4 filings to remain compliant with CRA payroll requirements. It's a more formal path, but it provides a sense of security and long-term structure for those who value stability.

The Benefits of Issuing Dividends

Dividends offer a simpler alternative for many business owners. Since they're paid from after-tax profits, the corporation doesn't get a deduction, but you don't have to deal with CPP contributions or payroll remittances. This can save several thousand dollars in annual costs depending on your income level. To prevent double taxation, the CRA provides a "Dividend Tax Credit" on your personal return, reflecting the tax the corporation has already paid. This makes dividends an attractive option for those who already have significant RRSP room or prefer to invest their "tax savings" into their own corporate growth.

Steps to Organize Your Corporation for CRA Compliance

Setting up the legal entity is only the first step. To maintain the integrity of your new structure, you must organize your corporate affairs with precision. For CRA filers, this begins with obtaining a 9-digit Business Number (BN), which serves as your corporation's permanent identity. You also need a dedicated corporate bank account. This isn't just for convenience; it's a critical requirement to maintain the "corporate veil," ensuring the CRA and the courts recognize the business as a distinct entity from your personal life. Mixing funds is a common pitfall that can invite unwanted scrutiny during an audit.

Choosing a fiscal year-end is another area where business incorporation tax advice provides a competitive edge. Unlike individuals who must follow the calendar year, a corporation can choose any 12-month period for its first year. This allows you to time your corporate year-end to align with your business cycle or to defer personal tax on dividends and bonuses. It's a proactive way to manage cash flow and secure a better outcome. Implementing a digital bookkeeping system today ensures you're not just reacting to requirements but are actively looking ahead to secure your financial foundation.

Registering for Essential CRA Program Accounts

Every corporation needs specific program accounts to interact with the CRA. If your revenue exceeds $30,000, you must register for a GST/HST (RT) account. Even if you haven't hit that threshold, voluntary registration often makes sense so you can claim Input Tax Credits on your startup costs. If you've decided to pay yourself a salary as discussed earlier, you'll also need a Payroll (RP) account. Registering these accounts promptly ensures you don't face late-filing penalties or interest charges.

Establishing a Robust Record-Keeping System

The CRA requires you to maintain "adequate records" that clearly support your income and expenses. In 2026, a digital bookkeeping system is the gold standard for transparency. It allows you to track every deductible expense with ease. A deductible expense is any reasonable cost incurred to earn income. Keeping personal and business receipts strictly separate is the best way to alleviate the stress of a potential review. If you need help setting up these accounts or choosing a year-end, get in touch with our team for expert guidance.

Securing Long-Term Success with Professional Tax Planning

Incorporation is not a one-time event; it is the beginning of a multi-year financial journey. While the initial setup provides immediate relief, the true value of a corporation is realized through sophisticated strategies that evolve as your revenue grows. For CRA filers, one of the most complex areas to navigate is the "Tax on Split Income," commonly known as TOSI. These rules are designed to prevent business owners from shifting income to family members in lower tax brackets. Without a proactive guardian at your side, you could inadvertently trigger taxes at the highest marginal rate on those payments. Expert business incorporation tax advice ensures your family remains protected while staying fully compliant with these intricate regulations.

Another critical area of focus is the risk of being designated a Personal Service Business (PSB). If the CRA determines that your corporation is acting as an "incorporated employee" rather than an independent entity, you lose access to the Small Business Deduction. This leads to a significantly higher tax burden and limited expense deductions. We look ahead to analyze your service contracts and operational structure to mitigate these risks. By integrating estate planning and succession strategies into your corporate framework today, you realize a more stable transition for the next generation. It is about keeping more of what you earn through disciplined foresight.

Proactive Strategies for Sustainable Growth

Regular financial reviews are the best way to prevent stressful year-end tax surprises. These check-ins allow for "income smoothing," where you balance your income draws over multiple years to stay within lower tax brackets. This steady approach prevents the spikes in personal tax that often hit successful entrepreneurs. We encourage you to utilize specialized tax optimization for business owners to ensure every decision aligns with your long-term wealth goals. This level of customization transforms your tax return from a mere requirement into a strategic asset.

Why Professional Oversight Outperforms DIY Software

Tax software is often static and reactive. It can process numbers, but it cannot offer the dynamic advice of a seasoned mentor who understands your unique industry. A professional advisor provides deep-seated reliability by identifying opportunities that an algorithm might miss. From representing you during a CRA audit to adjusting your strategy for emerging sectors, our role is to act as your proactive guardian. This partnership offers a sense of total control and understanding, allowing you to focus on growing your business while we manage the regulatory complexities. You gain a steady hand at the helm, combining institutional wisdom with a modern outlook on your financial health.

Empower Your Business Future

Transitioning to a corporate structure is a powerful move that shifts your focus from mere survival to intentional growth. By mastering the CCPC advantage and choosing the right mix of salary and dividends, you create a resilient financial framework under CRA rules. The goal is to maximize your tax deferrals so you can reinvest in your vision today while securing your retirement for tomorrow. You deserve a partner who views your success with the same dedication you do.

Getting specialized business incorporation tax advice is essential to ensure every step you take is both compliant and optimized for your specific goals. With over 40 years of Canadian tax expertise and more than 495,000 returns filed with the CRA, we provide the steady hand you need to navigate complex regulations. Our 1,390+ five-star Google reviews reflect our commitment to being a proactive guardian for every entrepreneur we serve.

Book a consultation with Tax Partners to optimize your incorporation strategy. You've worked hard to build your business; now it's time to ensure your corporate structure works just as hard for you. We're here to help you realize your long-term goals with confidence and clarity.

Frequently Asked Questions

Is it better to pay myself a salary or dividends from my corporation?

The choice depends on your need for RRSP contribution room and your desire to participate in the Canada Pension Plan (CPP). Salaries are a deductible expense for the corporation and provide "earned income" for retirement planning. Dividends are paid from after-tax profits and don't require CPP contributions, which can save you money in the short term. Many owners use a combination of both to balance their personal cash flow and tax obligations.

How much money should my business earn before I decide to incorporate?

Most entrepreneurs find that incorporation becomes tax-efficient once annual profits consistently exceed the $40,000 to $50,000 range. If your business earns less than $30,000, the annual filing requirements and administrative costs often outweigh the tax benefits. You should only incorporate when you can afford to leave "excess" profit inside the corporation to take advantage of the lower small business tax rates under CRA rules.

What are the main tax deadlines for Canadian corporations under CRA rules?

Your T2 corporate income tax return must be filed within six months of your fiscal year-end. However, any taxes owing are typically due either two or three months after your year-end, depending on your corporation's specific status and income. Missing these deadlines can result in significant interest charges and penalties. It's vital to have a steady hand at the helm to track these dates throughout the year.

Can I deduct my incorporation costs on my first corporate tax return?

Yes, you can generally deduct a portion of your initial setup costs, such as legal and registration fees, as a business expense. Under CRA rules, these are often treated as capital expenditures with specific limits on how much can be claimed in the first year. Seeking professional business incorporation tax advice ensures you maximize these startup deductions while remaining compliant with current regulations. Always keep your receipts for these initial investments.

What happens if the CRA designates my corporation as a Personal Service Business?

If your corporation is designated as a Personal Service Business (PSB), you lose access to the Small Business Deduction and many standard expense claims. This results in your income being taxed at a much higher rate, effectively removing the tax advantages of incorporation. This designation often occurs if the owner would be considered an employee of the client if the corporation didn't exist. We help you structure your contracts to mitigate this risk.

How does the Small Business Deduction actually reduce my tax rate?

The Small Business Deduction (SBD) is a credit that lowers the federal corporate tax rate to 9% on the first $500,000 of active business income. This is a core component of business incorporation tax advice because it allows you to retain more capital for reinvestment. When you combine this with provincial rates, the total tax burden is significantly lower than personal tax brackets. This preferential treatment is designed specifically to help Canadian small businesses grow.

Do I need to register for GST/HST as soon as I incorporate?

You must register for a GST/HST account once your business revenue exceeds $30,000 in a single calendar year or over four consecutive quarters. However, many entrepreneurs choose to register voluntarily as soon as they incorporate. This allows you to claim Input Tax Credits (ITCs) on your startup expenses, effectively recovering the sales tax you paid on business equipment and services. It's a proactive way to manage your initial cash flow.

Can I use my corporate funds for personal expenses if I pay them back?

Using corporate funds for personal use creates a "shareholder loan," which can lead to serious tax consequences if not handled correctly. Under CRA rules, if the loan isn't repaid within one year after the end of the corporation's taxation year, the amount must be included in your personal income. It's much safer to pay yourself a formal salary or dividend. This maintains a clear corporate veil and prevents unnecessary audits or penalties.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Frequently Asked Questions

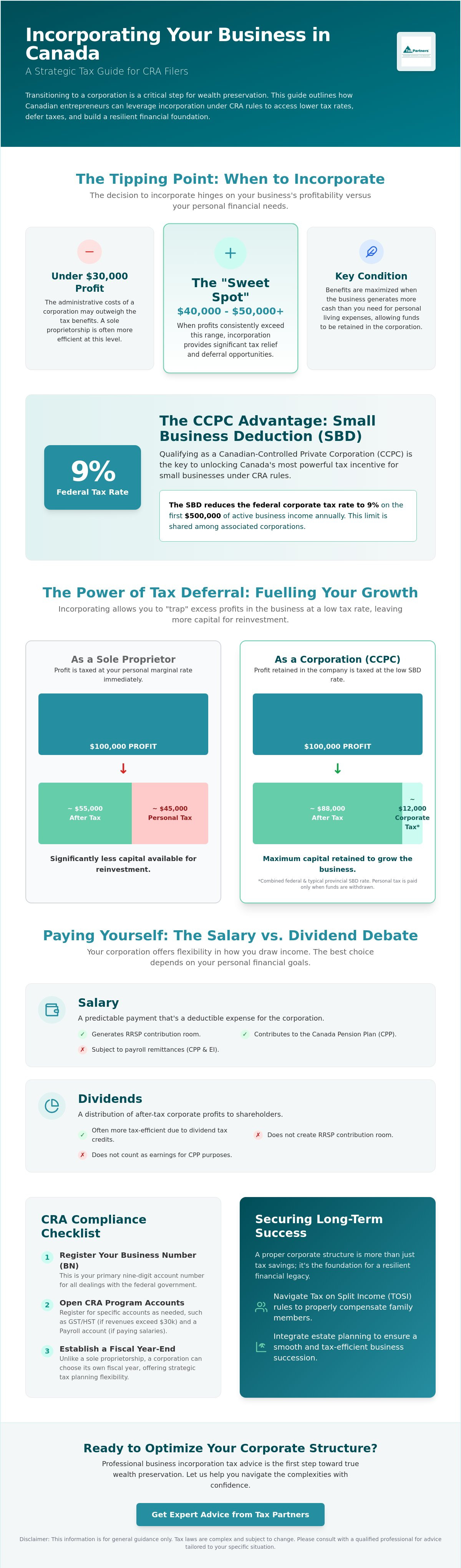

The Tipping Point: Income vs. Living Expenses

The financial advantage of incorporating hinges on your ability to leave "excess" profit within the business entity. If you require every dollar the business earns to cover your personal mortgage, groceries, and lifestyle, incorporation will offer limited tax relief. You'll simply pay personal tax on everything you withdraw. The strategy becomes effective when your business generates more cash than you need for daily life. By "trapping" these funds inside the corporation, you only pay the low corporate rate, allowing you to reinvest more capital back into your growth or a corporate investment portfolio. This foresight allows you to realize long-term wealth far more quickly than as a sole proprietor.

Personal Liability vs. Tax Flexibility

Beyond the well-known benefit of limited liability, a corporation introduces a distinct tax personality. Unlike a sole proprietorship, which must follow the calendar year, a corporation allows you to select a custom fiscal year-end. This flexibility is a powerful tool for tax planning. It lets you time the receipt of bonuses or dividends across different personal tax years to minimize your bracket. You gain the autonomy to choose between different types of income, such as salary or dividends, to optimize your personal cash flow while ensuring your corporate structure remains fully compliant with CRA regulations. This customized approach transforms your business from a simple job into a sophisticated financial engine. To unlock the most significant advantages of the Canadian tax system, your business must qualify as a Canadian-Controlled Private Corporation (CCPC). Under CRA rules, a CCPC is generally a private corporation resident in Canada that isn't controlled by non-residents or public corporations. This status is the gateway to specialized business incorporation tax advice because it allows you to access the Small Business Deduction (SBD). Without this designation, your business income would be taxed at the general corporate rate, which is substantially higher. Protecting your CCPC status is a proactive step toward securing a more favourable financial outcome.

The Small Business Deduction (SBD) Explained

The SBD is a tax credit that reduces the federal portion of your corporate tax to 9% on the first $500,000 of active business income. Provinces also provide their own versions of this deduction to support local growth. For example, in 2026, Ontario is scheduled to lower its small business rate to 2.2% on July 1. It's vital to recognize that the $500,000 limit must be shared among associated corporations. If you own multiple businesses, you can't simply multiply the deduction. The CRA requires these entities to allocate the limit between them, ensuring the benefit remains targeted at genuine small enterprises.

How Tax Deferral Fuels Business Growth

Tax deferral is perhaps the most compelling reason to incorporate. Imagine your business earns $100,000 in profit that you don't need for personal expenses. If you're a sole proprietor in a high tax bracket, you might lose nearly half of that to personal income tax immediately. By contrast, a CCPC only pays the low small business rate, leaving roughly $88,000 available for reinvestment. This allows you to purchase inventory, upgrade equipment, or hire staff using dollars that would otherwise have gone to the CRA. You can explore the broader tax benefits of incorporation to see how these savings compound over time. You must remain mindful of the passive income rules. The CRA limits the amount of investment income, such as interest or rent, a corporation can earn before the SBD begins to decrease. If your passive income exceeds $50,000 in a year, your access to the low small business rate starts to vanish. Managing this balance requires foresight and precision. If you're concerned about how these limits might impact your growth, it's wise to speak with a professional advisor to ensure your investments don't inadvertently trigger a higher tax bill. Choosing how to pay yourself is a fundamental part of business incorporation tax advice. The CRA views salary and dividends through the lens of "integration," a concept designed to ensure an individual pays roughly the same amount of tax regardless of the income's form. While the total tax bill might look similar on paper, the practical implications for your long-term wealth vary significantly. You're not just choosing a payment method; you're deciding on your retirement strategy and your immediate cash flow needs. Understanding corporate structure and tax obligations is essential here, as the corporation is a separate legal person that must account for these payments differently than a sole proprietorship. One of the biggest factors in this debate is the Canada Pension Plan (CPP). When you pay yourself a salary, both you and your corporation must contribute to the CPP. This adds a layer of cost that many entrepreneurs find frustrating. However, salary is considered "earned income," which is the only way to generate Registered Retirement Savings Plan (RRSP) contribution room. If you plan to use an RRSP as a primary vehicle for retirement, a salary is non-negotiable. It provides a steady hand at the helm of your personal financial future.

The Case for a Regular Salary

A salary acts as a deductible expense for your corporation, reducing its taxable income. This is a straightforward way to manage your corporate tax bracket while ensuring you have a steady, predictable personal income. Because it's employment income, it also makes it easier to qualify for personal disability insurance or mortgages. You'll need to stay organized with source deductions and annual T4 filings to remain compliant with CRA payroll requirements. It's a more formal path, but it provides a sense of security and long-term structure for those who value stability.

The Benefits of Issuing Dividends

Dividends offer a simpler alternative for many business owners. Since they're paid from after-tax profits, the corporation doesn't get a deduction, but you don't have to deal with CPP contributions or payroll remittances. This can save several thousand dollars in annual costs depending on your income level. To prevent double taxation, the CRA provides a "Dividend Tax Credit" on your personal return, reflecting the tax the corporation has already paid. This makes dividends an attractive option for those who already have significant RRSP room or prefer to invest their "tax savings" into their own corporate growth. Setting up the legal entity is only the first step. To maintain the integrity of your new structure, you must organize your corporate affairs with precision. For CRA filers, this begins with obtaining a 9-digit Business Number (BN), which serves as your corporation's permanent identity. You also need a dedicated corporate bank account. This isn't just for convenience; it's a critical requirement to maintain the "corporate veil," ensuring the CRA and the courts recognize the business as a distinct entity from your personal life. Mixing funds is a common pitfall that can invite unwanted scrutiny during an audit. Choosing a fiscal year-end is another area where business incorporation tax advice provides a competitive edge. Unlike individuals who must follow the calendar year, a corporation can choose any 12-month period for its first year. This allows you to time your corporate year-end to align with your business cycle or to defer personal tax on dividends and bonuses. It's a proactive way to manage cash flow and secure a better outcome. Implementing a digital bookkeeping system today ensures you're not just reacting to requirements but are actively looking ahead to secure your financial foundation.

Registering for Essential CRA Program Accounts

Every corporation needs specific program accounts to interact with the CRA. If your revenue exceeds $30,000, you must register for a GST/HST (RT) account. Even if you haven't hit that threshold, voluntary registration often makes sense so you can claim Input Tax Credits on your startup costs. If you've decided to pay yourself a salary as discussed earlier, you'll also need a Payroll (RP) account. Registering these accounts promptly ensures you don't face late-filing penalties or interest charges.

Establishing a Robust Record-Keeping System

The CRA requires you to maintain "adequate records" that clearly support your income and expenses. In 2026, a digital bookkeeping system is the gold standard for transparency. It allows you to track every deductible expense with ease. A deductible expense is any reasonable cost incurred to earn income. Keeping personal and business receipts strictly separate is the best way to alleviate the stress of a potential review. If you need help setting up these accounts or choosing a year-end, get in touch with our team for expert guidance. Incorporation is not a one-time event; it is the beginning of a multi-year financial journey. While the initial setup provides immediate relief, the true value of a corporation is realized through sophisticated strategies that evolve as your revenue grows. For CRA filers, one of the most complex areas to navigate is the "Tax on Split Income," commonly known as TOSI. These rules are designed to prevent business owners from shifting income to family members in lower tax brackets. Without a proactive guardian at your side, you could inadvertently trigger taxes at the highest marginal rate on those payments. Expert business incorporation tax advice ensures your family remains protected while staying fully compliant with these intricate regulations. Another critical area of focus is the risk of being designated a Personal Service Business (PSB). If the CRA determines that your corporation is acting as an "incorporated employee" rather than an independent entity, you lose access to the Small Business Deduction. This leads to a significantly higher tax burden and limited expense deductions. We look ahead to analyze your service contracts and operational structure to mitigate these risks. By integrating estate planning and succession strategies into your corporate framework today, you realize a more stable transition for the next generation. It is about keeping more of what you earn through disciplined foresight.

Proactive Strategies for Sustainable Growth

Regular financial reviews are the best way to prevent stressful year-end tax surprises. These check-ins allow for "income smoothing," where you balance your income draws over multiple years to stay within lower tax brackets. This steady approach prevents the spikes in personal tax that often hit successful entrepreneurs. We encourage you to utilize specialized tax optimization for business owners to ensure every decision aligns with your long-term wealth goals. This level of customization transforms your tax return from a mere requirement into a strategic asset.

Why Professional Oversight Outperforms DIY Software

Tax software is often static and reactive. It can process numbers, but it cannot offer the dynamic advice of a seasoned mentor who understands your unique industry. A professional advisor provides deep-seated reliability by identifying opportunities that an algorithm might miss. From representing you during a CRA audit to adjusting your strategy for emerging sectors, our role is to act as your proactive guardian. This partnership offers a sense of total control and understanding, allowing you to focus on growing your business while we manage the regulatory complexities. You gain a steady hand at the helm, combining institutional wisdom with a modern outlook on your financial health. Transitioning to a corporate structure is a powerful move that shifts your focus from mere survival to intentional growth. By mastering the CCPC advantage and choosing the right mix of salary and dividends, you create a resilient financial framework under CRA rules. The goal is to maximize your tax deferrals so you can reinvest in your vision today while securing your retirement for tomorrow. You deserve a partner who views your success with the same dedication you do. Getting specialized business incorporation tax advice is essential to ensure every step you take is both compliant and optimized for your specific goals. With over 40 years of Canadian tax expertise and more than 495,000 returns filed with the CRA, we provide the steady hand you need to navigate complex regulations. Our 1,390+ five-star Google reviews reflect our commitment to being a proactive guardian for every entrepreneur we serve. Book a consultation with Tax Partners to optimize your incorporation strategy. You've worked hard to build your business; now it's time to ensure your corporate structure works just as hard for you. We're here to help you realize your long-term goals with confidence and clarity.

Is it better to pay myself a salary or dividends from my corporation?

The choice depends on your need for RRSP contribution room and your desire to participate in the Canada Pension Plan (CPP). Salaries are a deductible expense for the corporation and provide "earned income" for retirement planning. Dividends are paid from after-tax profits and don't require CPP contributions, which can save you money in the short term. Many owners use a combination of both to balance their personal cash flow and tax obligations.

How much money should my business earn before I decide to incorporate?

Most entrepreneurs find that incorporation becomes tax-efficient once annual profits consistently exceed the $40,000 to $50,000 range. If your business earns less than $30,000, the annual filing requirements and administrative costs often outweigh the tax benefits. You should only incorporate when you can afford to leave "excess" profit inside the corporation to take advantage of the lower small business tax rates under CRA rules.

What are the main tax deadlines for Canadian corporations under CRA rules?

Your T2 corporate income tax return must be filed within six months of your fiscal year-end. However, any taxes owing are typically due either two or three months after your year-end, depending on your corporation's specific status and income. Missing these deadlines can result in significant interest charges and penalties. It's vital to have a steady hand at the helm to track these dates throughout the year.

Can I deduct my incorporation costs on my first corporate tax return?

Yes, you can generally deduct a portion of your initial setup costs, such as legal and registration fees, as a business expense. Under CRA rules, these are often treated as capital expenditures with specific limits on how much can be claimed in the first year. Seeking professional business incorporation tax advice ensures you maximize these startup deductions while remaining compliant with current regulations. Always keep your receipts for these initial investments.

What happens if the CRA designates my corporation as a Personal Service Business?

If your corporation is designated as a Personal Service Business (PSB), you lose access to the Small Business Deduction and many standard expense claims. This results in your income being taxed at a much higher rate, effectively removing the tax advantages of incorporation. This designation often occurs if the owner would be considered an employee of the client if the corporation didn't exist. We help you structure your contracts to mitigate this risk.

How does the Small Business Deduction actually reduce my tax rate?

The Small Business Deduction (SBD) is a credit that lowers the federal corporate tax rate to 9% on the first $500,000 of active business income. This is a core component of business incorporation tax advice because it allows you to retain more capital for reinvestment. When you combine this with provincial rates, the total tax burden is significantly lower than personal tax brackets. This preferential treatment is designed specifically to help Canadian small businesses grow.

Do I need to register for GST/HST as soon as I incorporate?

You must register for a GST/HST account once your business revenue exceeds $30,000 in a single calendar year or over four consecutive quarters. However, many entrepreneurs choose to register voluntarily as soon as they incorporate. This allows you to claim Input Tax Credits (ITCs) on your startup expenses, effectively recovering the sales tax you paid on business equipment and services. It's a proactive way to manage your initial cash flow.

Can I use my corporate funds for personal expenses if I pay them back?

Using corporate funds for personal use creates a "shareholder loan," which can lead to serious tax consequences if not handled correctly. Under CRA rules, if the loan isn't repaid within one year after the end of the corporation's taxation year, the amount must be included in your personal income. It's much safer to pay yourself a formal salary or dividend. This maintains a clear corporate veil and prevents unnecessary audits or penalties.