Navigating the Voluntary Disclosure Program (VDP): A Guide to CRA Tax Amnesty

What if you could hand the Canada Revenue Agency a list of your past tax mistakes and, instead of facing criminal prosecution, receive a clear path to resolution? The voluntary disclosure program CRA offers exactly this opportunity, yet for many Canadians, the realization of an unfiled return or an overlooked asset still feels like an inescapable weight. You likely worry that coming forward will only accelerate a dreaded audit or trigger crushing gross negligence penalties. We understand that this anxiety is profound, but it shouldn't paralyze your financial future or your peace of mind.

This guide provides a professional, step-by-step roadmap to navigating the redesigned application process and the new RC199 requirements. By utilizing the updated unprompted track that came into effect on October 1, 2025, you can correct your records while potentially securing 100% penalty relief. We'll show you how to move from a state of uncertainty toward a feeling of total control, transforming a significant liability into a managed journey toward compliance. Our goal is to provide the clarity you need to resolve past errors with precision and foresight.

Key Takeaways

- Discover how the voluntary disclosure program CRA provides a structured path to correct past tax errors while avoiding criminal prosecution and heavy penalties.

- Learn to distinguish between the unprompted and prompted tracks to maximize your potential for interest and penalty relief.

- Identify the essential eligibility criteria that ensure your submission is considered truly voluntary and comprehensive by the CRA.

- Master the documentation requirements for both domestic and offshore assets to ensure your application is complete and defensible.

- Understand the strategic advantages of professional oversight in securing a successful outcome under the latest 2025 regulatory changes.

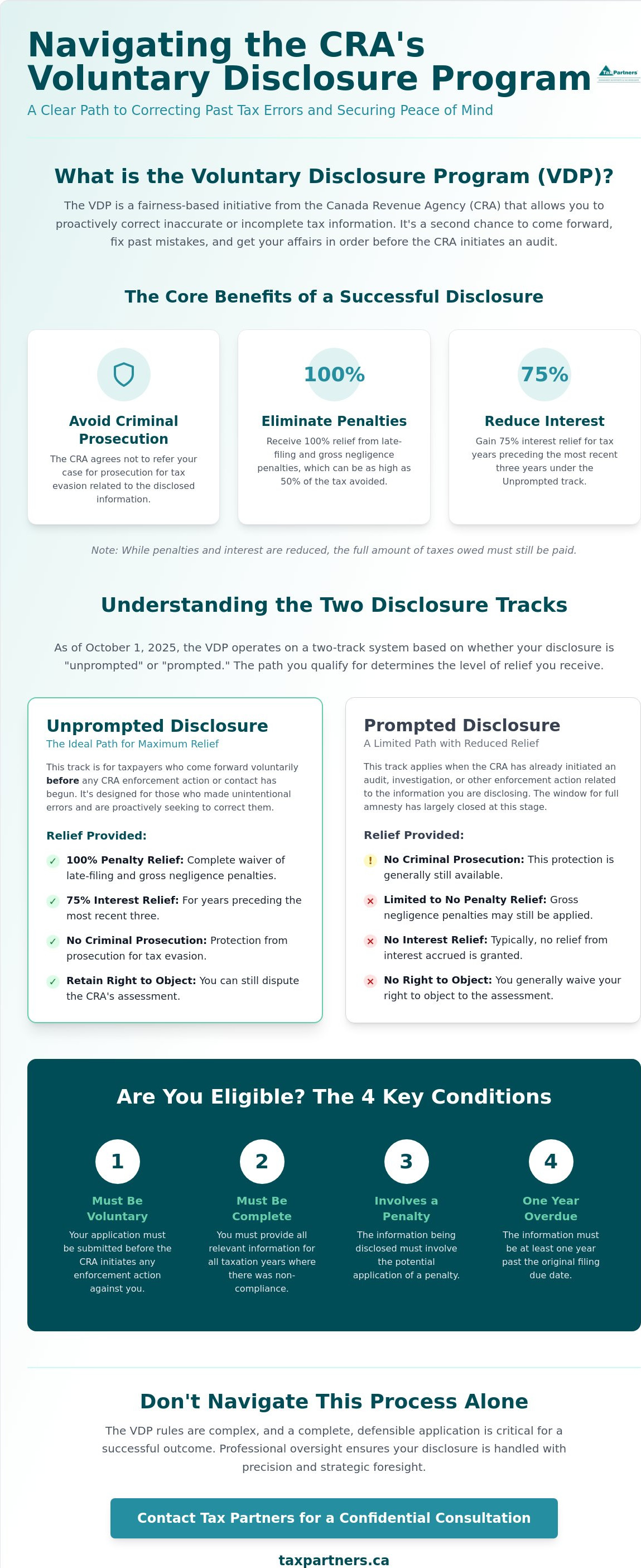

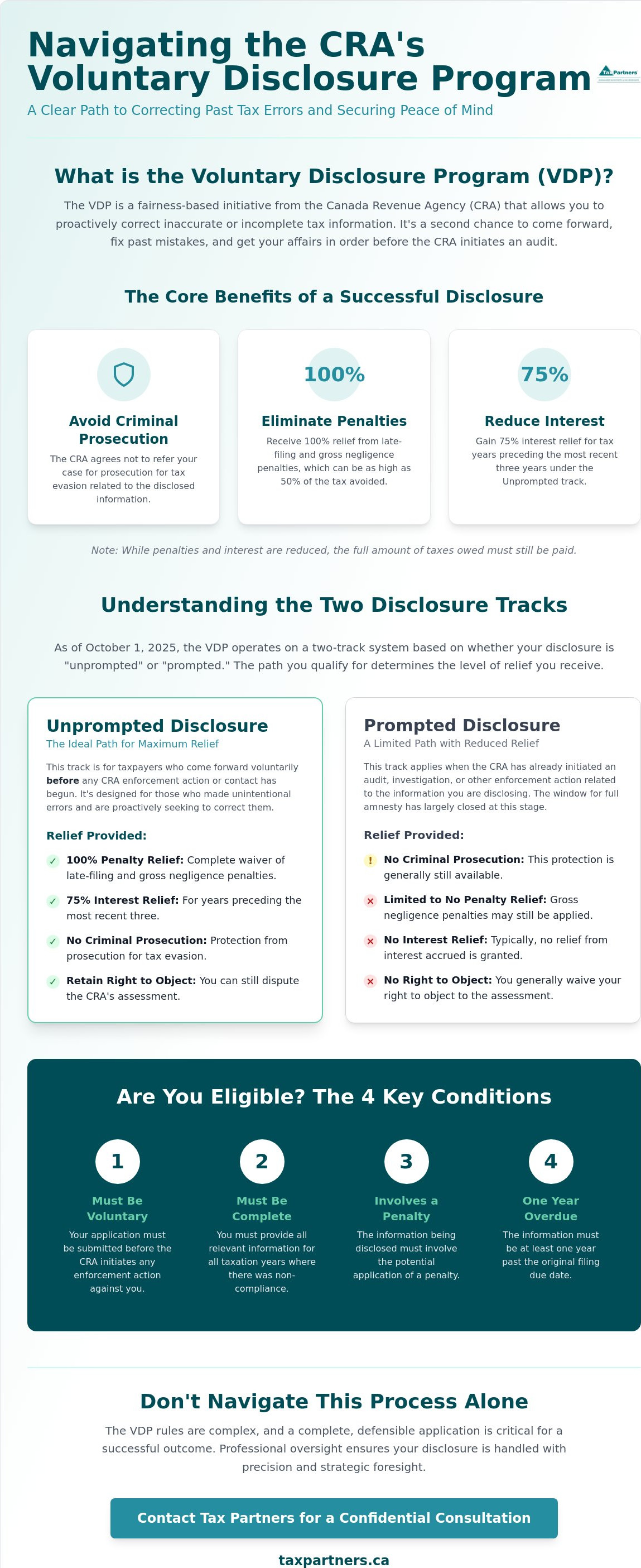

What is the CRA Voluntary Disclosure Program?

The Canada Revenue Agency (CRA) operates on a system of self-assessment, which relies heavily on the honesty and accuracy of every taxpayer. But mistakes happen. Whether it's an overlooked offshore account, a misunderstood rental income rule, or years of unfiled returns, the weight of non-compliance can be overwhelming. The voluntary disclosure program CRA exists as a fairness-based relief initiative designed to help you correct these errors before they escalate into legal or financial crises. It's an invitation to come forward and settle your affairs with a level of transparency that the CRA rewards with significant leniency.

On October 1, 2025, the CRA introduced significant updates to the program to provide better clarity for those seeking to realize their tax obligations. These changes replaced the old "General" and "Limited" tracks with a more intuitive system based on whether your disclosure is "unprompted" or "prompted." This shift reflects a modern approach to tax administration, prioritizing cooperative behaviour over confrontation. By offering a structured path to resolution, the CRA aims to bring taxpayers back into the fold of compliance, ensuring the tax system remains equitable for all. This proactive guardian approach allows you to move from uncertainty toward a feeling of total control.

The Core Concept of Tax Amnesty in Canada

True tax amnesty is a rare opportunity in the Canadian regulatory landscape. It's vital to distinguish a voluntary disclosure from a prompted audit. An audit is a reactive process where the CRA has already flagged your file for investigation; at that point, the window for amnesty has largely closed. The Canada Revenue Agency's Voluntary Disclosures Program is a proactive mechanism to rectify non-compliance before the CRA initiates contact. This program is rooted in the "Fairness to Canadians" principle, rewarding those who take responsibility to organize their affairs before enforcement begins.

Types of Relief Available

The primary incentive for coming forward is the substantial relief from the most severe consequences of tax non-compliance. Under the current rules, successful applicants can secure several layers of protection:

- Relief from criminal prosecution: The CRA agrees not to refer your case for prosecution for tax evasion related to the disclosed information.

- Elimination of penalties: You may receive 100% relief from late-filing and gross negligence penalties, which can otherwise reach 50% of the tax avoided.

- Interest relief: For "unprompted" disclosures, you may receive 75% interest relief for years preceding the most recent three years of filings.

While you must still pay the full tax owed, these reductions make the path to resolution far more manageable. It's a strategic move to secure your financial future while ensuring your tax records are perfectly accurate. By acting now, you replace the fear of a potential audit with the certainty of a settled account.

General vs. Limited Relief: Navigating the Two Tracks

Understanding the mechanics of the voluntary disclosure program CRA requires a clear grasp of its two-track structure. The CRA doesn't apply a one-size-fits-all approach to every application. Instead, they evaluate the circumstances surrounding your non-compliance to decide whether you qualify for General or Limited relief. As of the regulatory updates in October 2025, these tracks are now primarily categorized as "unprompted" and "prompted" disclosures. This distinction fundamentally changes the financial and legal outcome of your submission. It's the difference between a full reset and a restricted settlement.

The General Program: The Ideal Outcome

The General Program, or the unprompted track, represents the most favourable path for taxpayers. It's designed for those who made unintentional errors and come forward before any CRA contact occurs. Typical scenarios include a taxpayer forgetting to file a T1135 for a foreign inheritance or a small business owner making a genuine bookkeeping mistake. If you're accepted into this track, you receive the highest level of protection. This includes 100% relief from penalties and 75% relief on interest for years preceding the most recent three years of filings. Most importantly, you retain your legal right to object to the CRA’s assessment. Recent research on the Voluntary Disclosures Program highlights that this track is the primary goal for most applicants due to its comprehensive nature and the preservation of taxpayer rights.

The Limited Program: When Relief is Restricted

The Limited track, often associated with prompted disclosures, is reserved for situations where the CRA identifies "gross negligence" or deliberate tax avoidance. Sophistication plays a major role here. If you used complex offshore structures or ignored general educational letters from the agency, the CRA will likely restrict your relief. While you still avoid criminal prosecution, you'll still face significant penalties. A critical downside is the requirement to waive your right to appeal or object to the specific issues in your disclosure. This effectively means you must accept the CRA's final calculation without question.

Corporate size also dictates these tracks. Large businesses with gross annual revenues exceeding $250 million are almost always directed to the Limited track. The CRA expects these organizations to have rigorous internal controls, making any errors harder to justify as unintentional. Navigating these nuances requires a steady hand and a proactive approach. Engaging with Canadian accounting and tax services early in the process helps you build a defensible case for the General track. We act as your proactive guardian, ensuring your disclosure is framed accurately to minimize costs and maximize your peace of mind.

Eligibility Criteria: Can You Apply for the VDP?

While the program offers a fresh start, it's not an open door for every taxpayer. The CRA applies rigorous standards to filter out those attempting to use the program as a shield once they suspect they've been caught. To qualify for the voluntary disclosure program CRA, your application must meet specific conditions that prove your intent is genuine and your disclosure is exhaustive. This isn't merely about filling out a form; it's about demonstrating a commitment to transparency and future compliance. We view this stage as the foundation of your resolution, where precision and honesty are your most valuable assets.

The Four Pillars of a Valid Disclosure

A successful application rests on four mandatory requirements. First, the submission must be "voluntary." This means you must come forward before the CRA initiates any enforcement action or audit against you. Interestingly, under the rules effective since October 2025, receiving a general educational letter doesn't automatically bar you from the program, but an active investigation definitely does. Second, your disclosure must be "complete." You can't cherry-pick which errors to fix. You must disclose every instance of non-compliance across all tax years. For Canadian-sourced income, this typically means the last six years, while foreign-sourced assets require ten years of documentation to satisfy the CRA Voluntary Disclosures Program standards.

The third pillar requires that the disclosure involves a potential penalty. If you're simply correcting a minor typo that wouldn't have resulted in a fine, the CRA will direct you toward a routine adjustment instead. Finally, for information returns like the T1135, the "one year past due" rule applies. Your filing must be at least one year late to be considered for relief under this program. These pillars ensure that the system remains fair for those who have always complied while providing a steady hand for those ready to organize their affairs correctly.

Common Disqualifiers to Avoid

Many taxpayers stumble because they wait too long. If the CRA has already flagged your file or started an audit on a related business entity, your application will likely be rejected. Another common pitfall is submitting a disclosure that provides no "new" information. If the CRA already knows about your offshore account through international data exchange agreements, your disclosure isn't truly voluntary. Verifying your status is a delicate process. You need to ensure no enforcement action is pending before you sign your name to a confession. This is where foresight and professional oversight become critical. By conducting a thorough internal review before filing, you ensure your disclosure is both defensible and strategically sound, moving you from a state of uncertainty toward total control.

How to Apply for Voluntary Disclosure: A Step-by-Step Guide

Applying for the voluntary disclosure program CRA requires a methodical approach that prioritizes precision over speed. It's a structured journey that transforms a complex liability into a manageable resolution. By following a clear sequence of steps, you ensure your submission is not only complete but also resilient against CRA scrutiny. This isn't just about filing paperwork; it's about building a defensible case that demonstrates your commitment to transparency.

The process begins with a rigorous internal review. You'll need to examine all past years where non-compliance occurred, typically reaching back six years for Canadian income and ten years for foreign assets. Once the scope is clear, you must gather every supporting document, from offshore bank statements to digital asset transaction logs. This preparation leads to the completion of Form RC199, the official application for the voluntary disclosure program CRA. Alongside this form, you'll provide a narrative that contextualizes the errors and submit everything for a review period that requires patience and responsiveness. We act as your proactive guardian during this time, managing the dialogue with the agency to ensure a smooth progression.

Preparing Your Documentation

Your documentation must be "ready-to-file" the moment you submit your application. The CRA expects to see completed tax returns or amended filings that reflect the corrected information in full. It's also vital to calculate the estimated tax owing to demonstrate your transparency and readiness to settle the account. In a modern regulatory environment, this includes organizing records for cryptocurrency and other digital assets. These records must be clear and verifiable to prevent the CRA from questioning the completeness of your disclosure. Providing these details upfront shows that you're not just reacting but are actively looking ahead to secure a better outcome.

The Narrative Statement: Telling Your Story

The narrative statement is perhaps the most critical component of your filing because it provides the "why" behind the "what." The narrative statement must clearly demonstrate why the error was unintentional to secure the General track. When drafting this document, maintain an honest, transparent, and professional tone that reflects your dedication to future compliance. You should avoid "red flag" language that might suggest sophisticated tax planning or deliberate concealment, as these terms can inadvertently trigger the Limited stream. Instead, focus on the specific life events or misunderstandings that led to the oversight.

Managing this process alone can feel overwhelming, but you don't have to face the CRA without a steady hand at the helm. Our Canadian accounting and tax services provide the expertise and foresight required to prepare a successful application. We help you move from a state of potential uncertainty toward a feeling of total control and understanding, ensuring your disclosure is handled with the personalized care it deserves.

Protecting Your Interests with Professional Tax Partners

Attempting a DIY submission for the voluntary disclosure program CRA often feels like a logical way to save costs, but it frequently results in the opposite outcome. Without a deep understanding of how the CRA interprets "sophistication" or "negligence," unrepresented taxpayers often inadvertently say or provide things that relegate their file to the Limited track. This mistake can cost thousands in avoidable penalties and lead to a permanent loss of appeal rights. We believe that true financial redemption requires more than just filling out forms; it requires a strategic partnership with a proactive guardian who understands the nuances of the system.

Our firm brings over 40 years of institutional wisdom to every case, providing a level of reliability that only decades of experience can foster. We don't just react to CRA requirements. We look ahead to secure the best possible outcome for your specific situation. By moving from a state of potential uncertainty toward a feeling of total control, you replace anxiety with a clear, professional roadmap. This transition is about more than just settling a debt. It's about reclaiming your peace of mind and ensuring your financial future is built on a foundation of steadfast compliance.

The Advantage of Strategic Representation

A successful disclosure begins long before the CRA receives your application. We conduct a rigorous analysis of your financial history to identify and mitigate audit risks that you might not even realize exist. During this process, we maintain strict professional confidentiality, ensuring your sensitive information is handled with the highest ethical standards. When it comes time for the case-by-case review, we act as your seasoned mentor in negotiations with CRA officers. We know how to frame the narrative of your non-compliance to highlight its unintentional nature, which is the key to securing the General track relief you deserve. This precision ensures that your disclosure is not just accepted, but accepted on the most favourable terms possible.

Beyond Disclosure: Long-Term Compliance

Resolving your past errors is only the first step in a successful long-term partnership. Once your disclosure is settled, we help you implement robust bookkeeping and payroll services to ensure that similar errors never recur. This proactive approach extends to wealth management and financial planning, where we help you protect and grow your newly compliant assets. We aim to move you from a state of worry to a feeling of total understanding and control over your tax future. Our support is seamless and end-to-end, providing a steady hand at the helm as you navigate the complexities of the Canadian tax system.

Speak with a Tax Partners expert today to start your voluntary disclosure and take the first step toward a secure, compliant future.

Secure Your Financial Fresh Start

The weight of past tax errors shouldn't define your financial trajectory. Correcting your records through the voluntary disclosure program CRA is a decisive step toward lasting peace of mind. This process allows you to replace the anxiety of potential audits with a structured, professional resolution. By choosing the unprompted track and ensuring your documentation is complete, you protect your assets and your reputation from the most severe consequences of non-compliance.

Our firm brings over 40 years of institutional wisdom to your side. We've successfully filed more than 495,000 tax returns and saved our clients over $87M in taxes and penalties. This proven track record allows us to act as a proactive guardian for your interests, ensuring every detail of your disclosure is handled with precision and personalized care. We offer a steady hand to help you navigate these complexities with confidence and foresight.

Contact Tax Partners for a confidential VDP consultation today to organize your affairs and regain total control over your tax future. Your path to resolution starts with a single, secure conversation.

Frequently Asked Questions

Is the Voluntary Disclosure Program the same as tax amnesty?

Yes, it's essentially a form of tax amnesty, though the CRA officially describes it as a fairness-based relief program. By coming forward, you avoid criminal prosecution and secure relief from significant penalties. This mechanism encourages voluntary compliance by rewarding honesty with leniency. It's a proactive way to organize your affairs before the agency identifies the errors through their own enforcement channels, providing a clear path to financial resolution.

Can I apply for the VDP if the CRA has already sent me a letter?

Yes, you can apply even if you've received a letter, provided it's a general educational notice or a summary of non-compliance. Your application is only disqualified if a specific audit or investigation has already been initiated. However, if the CRA's contact prompted your disclosure, you'll likely be placed in the prompted track. This means your interest relief will be reduced compared to a truly unprompted, voluntary submission.

What happens if the CRA denies my VDP application?

You'll be assessed for the full tax amount, interest, and all applicable penalties if your application is denied. This includes gross negligence penalties that can reach 50% of the tax avoided. If you believe the denial was unfair, you can request a second-level administrative review within 30 days. It's vital to ensure your initial submission is bulletproof, as a denial removes the shield against criminal prosecution for the disclosed issues.

Will I still have to pay interest on the taxes I owe?

Yes, you'll always remain responsible for the full tax principal and a portion of the interest. Under the voluntary disclosure program CRA, the level of relief depends on your track. Unprompted applicants can receive 75% interest relief for years older than the three most recent filings. Prompted applicants receive much less, usually capped at 25% relief. This structure prioritizes those who act with foresight before the agency initiates contact.

Can I disclose offshore bank accounts through the VDP?

Yes, disclosing foreign assets and offshore bank accounts is one of the most common applications of the program. You must provide a comprehensive ten-year history of documentation for foreign-sourced income to satisfy the CRA's requirements. This process is a strategic way to rectify unfiled T1135 forms and avoid the heavy penalties associated with offshore non-compliance. It's a proactive step to secure your global financial interests.

How long does the CRA take to process a VDP application in 2026?

Processing typically takes between six and twelve months in the current 2026 regulatory environment. While the CRA has introduced simplified forms and online callback options to streamline the journey, multi-year disclosures require thorough verification. The agency must review your documentation against their internal records to ensure the disclosure is truly complete. Having a steady hand at the helm helps manage this period by ensuring all follow-up requests are handled with precision and speed.

Do I need a lawyer or a CPA for a voluntary disclosure?

You aren't legally required to hire a professional, but a CPA provides the strategic oversight needed to secure the best possible outcome. Professional representation ensures your narrative statement is framed accurately to qualify for the General track rather than the restricted Limited stream. We act as a proactive guardian, managing the complex documentation and negotiations required. This foresight often pays for itself by maximizing penalty relief and ensuring a smooth, defensible process.

Can businesses apply for the VDP, or is it only for individuals?

Both businesses and individuals are fully eligible to utilize the program to correct past tax errors. The CRA evaluates each case based on the taxpayer's sophistication and the nature of the non-compliance. While large corporations with revenues over $250 million are typically directed to the Limited track, small businesses can often secure General relief for unintentional bookkeeping mistakes. It's an essential tool for any entity looking to realize its tax obligations accurately.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

The Core Concept of Tax Amnesty in Canada

True tax amnesty is a rare opportunity in the Canadian regulatory landscape. It's vital to distinguish a voluntary disclosure from a prompted audit. An audit is a reactive process where the CRA has already flagged your file for investigation; at that point, the window for amnesty has largely closed. The Canada Revenue Agency's Voluntary Disclosures Program is a proactive mechanism to rectify non-compliance before the CRA initiates contact. This program is rooted in the "Fairness to Canadians" principle, rewarding those who take responsibility to organize their affairs before enforcement begins.

Types of Relief Available

The primary incentive for coming forward is the substantial relief from the most severe consequences of tax non-compliance. Under the current rules, successful applicants can secure several layers of protection: While you must still pay the full tax owed, these reductions make the path to resolution far more manageable. It's a strategic move to secure your financial future while ensuring your tax records are perfectly accurate. By acting now, you replace the fear of a potential audit with the certainty of a settled account. Understanding the mechanics of the voluntary disclosure program CRA requires a clear grasp of its two-track structure. The CRA doesn't apply a one-size-fits-all approach to every application. Instead, they evaluate the circumstances surrounding your non-compliance to decide whether you qualify for General or Limited relief. As of the regulatory updates in October 2025, these tracks are now primarily categorized as "unprompted" and "prompted" disclosures. This distinction fundamentally changes the financial and legal outcome of your submission. It's the difference between a full reset and a restricted settlement.

The General Program: The Ideal Outcome

The General Program, or the unprompted track, represents the most favourable path for taxpayers. It's designed for those who made unintentional errors and come forward before any CRA contact occurs. Typical scenarios include a taxpayer forgetting to file a T1135 for a foreign inheritance or a small business owner making a genuine bookkeeping mistake. If you're accepted into this track, you receive the highest level of protection. This includes 100% relief from penalties and 75% relief on interest for years preceding the most recent three years of filings. Most importantly, you retain your legal right to object to the CRA’s assessment. Recent research on the Voluntary Disclosures Program highlights that this track is the primary goal for most applicants due to its comprehensive nature and the preservation of taxpayer rights.

The Limited Program: When Relief is Restricted

The Limited track, often associated with prompted disclosures, is reserved for situations where the CRA identifies "gross negligence" or deliberate tax avoidance. Sophistication plays a major role here. If you used complex offshore structures or ignored general educational letters from the agency, the CRA will likely restrict your relief. While you still avoid criminal prosecution, you'll still face significant penalties. A critical downside is the requirement to waive your right to appeal or object to the specific issues in your disclosure. This effectively means you must accept the CRA's final calculation without question. Corporate size also dictates these tracks. Large businesses with gross annual revenues exceeding $250 million are almost always directed to the Limited track. The CRA expects these organizations to have rigorous internal controls, making any errors harder to justify as unintentional. Navigating these nuances requires a steady hand and a proactive approach. Engaging with Canadian accounting and tax services early in the process helps you build a defensible case for the General track. We act as your proactive guardian, ensuring your disclosure is framed accurately to minimize costs and maximize your peace of mind. While the program offers a fresh start, it's not an open door for every taxpayer. The CRA applies rigorous standards to filter out those attempting to use the program as a shield once they suspect they've been caught. To qualify for the voluntary disclosure program CRA, your application must meet specific conditions that prove your intent is genuine and your disclosure is exhaustive. This isn't merely about filling out a form; it's about demonstrating a commitment to transparency and future compliance. We view this stage as the foundation of your resolution, where precision and honesty are your most valuable assets.

The Four Pillars of a Valid Disclosure

A successful application rests on four mandatory requirements. First, the submission must be "voluntary." This means you must come forward before the CRA initiates any enforcement action or audit against you. Interestingly, under the rules effective since October 2025, receiving a general educational letter doesn't automatically bar you from the program, but an active investigation definitely does. Second, your disclosure must be "complete." You can't cherry-pick which errors to fix. You must disclose every instance of non-compliance across all tax years. For Canadian-sourced income, this typically means the last six years, while foreign-sourced assets require ten years of documentation to satisfy the CRA Voluntary Disclosures Program standards. The third pillar requires that the disclosure involves a potential penalty. If you're simply correcting a minor typo that wouldn't have resulted in a fine, the CRA will direct you toward a routine adjustment instead. Finally, for information returns like the T1135, the "one year past due" rule applies. Your filing must be at least one year late to be considered for relief under this program. These pillars ensure that the system remains fair for those who have always complied while providing a steady hand for those ready to organize their affairs correctly.

Common Disqualifiers to Avoid

Many taxpayers stumble because they wait too long. If the CRA has already flagged your file or started an audit on a related business entity, your application will likely be rejected. Another common pitfall is submitting a disclosure that provides no "new" information. If the CRA already knows about your offshore account through international data exchange agreements, your disclosure isn't truly voluntary. Verifying your status is a delicate process. You need to ensure no enforcement action is pending before you sign your name to a confession. This is where foresight and professional oversight become critical. By conducting a thorough internal review before filing, you ensure your disclosure is both defensible and strategically sound, moving you from a state of uncertainty toward total control. Applying for the voluntary disclosure program CRA requires a methodical approach that prioritizes precision over speed. It's a structured journey that transforms a complex liability into a manageable resolution. By following a clear sequence of steps, you ensure your submission is not only complete but also resilient against CRA scrutiny. This isn't just about filing paperwork; it's about building a defensible case that demonstrates your commitment to transparency. The process begins with a rigorous internal review. You'll need to examine all past years where non-compliance occurred, typically reaching back six years for Canadian income and ten years for foreign assets. Once the scope is clear, you must gather every supporting document, from offshore bank statements to digital asset transaction logs. This preparation leads to the completion of Form RC199, the official application for the voluntary disclosure program CRA. Alongside this form, you'll provide a narrative that contextualizes the errors and submit everything for a review period that requires patience and responsiveness. We act as your proactive guardian during this time, managing the dialogue with the agency to ensure a smooth progression.

Preparing Your Documentation

Your documentation must be "ready-to-file" the moment you submit your application. The CRA expects to see completed tax returns or amended filings that reflect the corrected information in full. It's also vital to calculate the estimated tax owing to demonstrate your transparency and readiness to settle the account. In a modern regulatory environment, this includes organizing records for cryptocurrency and other digital assets. These records must be clear and verifiable to prevent the CRA from questioning the completeness of your disclosure. Providing these details upfront shows that you're not just reacting but are actively looking ahead to secure a better outcome.

The Narrative Statement: Telling Your Story

The narrative statement is perhaps the most critical component of your filing because it provides the "why" behind the "what." The narrative statement must clearly demonstrate why the error was unintentional to secure the General track. When drafting this document, maintain an honest, transparent, and professional tone that reflects your dedication to future compliance. You should avoid "red flag" language that might suggest sophisticated tax planning or deliberate concealment, as these terms can inadvertently trigger the Limited stream. Instead, focus on the specific life events or misunderstandings that led to the oversight. Managing this process alone can feel overwhelming, but you don't have to face the CRA without a steady hand at the helm. Our Canadian accounting and tax services provide the expertise and foresight required to prepare a successful application. We help you move from a state of potential uncertainty toward a feeling of total control and understanding, ensuring your disclosure is handled with the personalized care it deserves. Attempting a DIY submission for the voluntary disclosure program CRA often feels like a logical way to save costs, but it frequently results in the opposite outcome. Without a deep understanding of how the CRA interprets "sophistication" or "negligence," unrepresented taxpayers often inadvertently say or provide things that relegate their file to the Limited track. This mistake can cost thousands in avoidable penalties and lead to a permanent loss of appeal rights. We believe that true financial redemption requires more than just filling out forms; it requires a strategic partnership with a proactive guardian who understands the nuances of the system. Our firm brings over 40 years of institutional wisdom to every case, providing a level of reliability that only decades of experience can foster. We don't just react to CRA requirements. We look ahead to secure the best possible outcome for your specific situation. By moving from a state of potential uncertainty toward a feeling of total control, you replace anxiety with a clear, professional roadmap. This transition is about more than just settling a debt. It's about reclaiming your peace of mind and ensuring your financial future is built on a foundation of steadfast compliance.

The Advantage of Strategic Representation

A successful disclosure begins long before the CRA receives your application. We conduct a rigorous analysis of your financial history to identify and mitigate audit risks that you might not even realize exist. During this process, we maintain strict professional confidentiality, ensuring your sensitive information is handled with the highest ethical standards. When it comes time for the case-by-case review, we act as your seasoned mentor in negotiations with CRA officers. We know how to frame the narrative of your non-compliance to highlight its unintentional nature, which is the key to securing the General track relief you deserve. This precision ensures that your disclosure is not just accepted, but accepted on the most favourable terms possible.

Beyond Disclosure: Long-Term Compliance

Resolving your past errors is only the first step in a successful long-term partnership. Once your disclosure is settled, we help you implement robust bookkeeping and payroll services to ensure that similar errors never recur. This proactive approach extends to wealth management and financial planning, where we help you protect and grow your newly compliant assets. We aim to move you from a state of worry to a feeling of total understanding and control over your tax future. Our support is seamless and end-to-end, providing a steady hand at the helm as you navigate the complexities of the Canadian tax system. Speak with a Tax Partners expert today to start your voluntary disclosure and take the first step toward a secure, compliant future. The weight of past tax errors shouldn't define your financial trajectory. Correcting your records through the voluntary disclosure program CRA is a decisive step toward lasting peace of mind. This process allows you to replace the anxiety of potential audits with a structured, professional resolution. By choosing the unprompted track and ensuring your documentation is complete, you protect your assets and your reputation from the most severe consequences of non-compliance. Our firm brings over 40 years of institutional wisdom to your side. We've successfully filed more than 495,000 tax returns and saved our clients over $87M in taxes and penalties. This proven track record allows us to act as a proactive guardian for your interests, ensuring every detail of your disclosure is handled with precision and personalized care. We offer a steady hand to help you navigate these complexities with confidence and foresight. Contact Tax Partners for a confidential VDP consultation today to organize your affairs and regain total control over your tax future. Your path to resolution starts with a single, secure conversation.

Is the Voluntary Disclosure Program the same as tax amnesty?

Yes, it's essentially a form of tax amnesty, though the CRA officially describes it as a fairness-based relief program. By coming forward, you avoid criminal prosecution and secure relief from significant penalties. This mechanism encourages voluntary compliance by rewarding honesty with leniency. It's a proactive way to organize your affairs before the agency identifies the errors through their own enforcement channels, providing a clear path to financial resolution.

Can I apply for the VDP if the CRA has already sent me a letter?

Yes, you can apply even if you've received a letter, provided it's a general educational notice or a summary of non-compliance. Your application is only disqualified if a specific audit or investigation has already been initiated. However, if the CRA's contact prompted your disclosure, you'll likely be placed in the prompted track. This means your interest relief will be reduced compared to a truly unprompted, voluntary submission.

What happens if the CRA denies my VDP application?

You'll be assessed for the full tax amount, interest, and all applicable penalties if your application is denied. This includes gross negligence penalties that can reach 50% of the tax avoided. If you believe the denial was unfair, you can request a second-level administrative review within 30 days. It's vital to ensure your initial submission is bulletproof, as a denial removes the shield against criminal prosecution for the disclosed issues.

Will I still have to pay interest on the taxes I owe?

Yes, you'll always remain responsible for the full tax principal and a portion of the interest. Under the voluntary disclosure program CRA, the level of relief depends on your track. Unprompted applicants can receive 75% interest relief for years older than the three most recent filings. Prompted applicants receive much less, usually capped at 25% relief. This structure prioritizes those who act with foresight before the agency initiates contact.

Can I disclose offshore bank accounts through the VDP?

Yes, disclosing foreign assets and offshore bank accounts is one of the most common applications of the program. You must provide a comprehensive ten-year history of documentation for foreign-sourced income to satisfy the CRA's requirements. This process is a strategic way to rectify unfiled T1135 forms and avoid the heavy penalties associated with offshore non-compliance. It's a proactive step to secure your global financial interests.

How long does the CRA take to process a VDP application in 2026?

Processing typically takes between six and twelve months in the current 2026 regulatory environment. While the CRA has introduced simplified forms and online callback options to streamline the journey, multi-year disclosures require thorough verification. The agency must review your documentation against their internal records to ensure the disclosure is truly complete. Having a steady hand at the helm helps manage this period by ensuring all follow-up requests are handled with precision and speed.

Do I need a lawyer or a CPA for a voluntary disclosure?

You aren't legally required to hire a professional, but a CPA provides the strategic oversight needed to secure the best possible outcome. Professional representation ensures your narrative statement is framed accurately to qualify for the General track rather than the restricted Limited stream. We act as a proactive guardian, managing the complex documentation and negotiations required. This foresight often pays for itself by maximizing penalty relief and ensuring a smooth, defensible process.

Can businesses apply for the VDP, or is it only for individuals?

Both businesses and individuals are fully eligible to utilize the program to correct past tax errors. The CRA evaluates each case based on the taxpayer's sophistication and the nature of the non-compliance. While large corporations with revenues over $250 million are typically directed to the Limited track, small businesses can often secure General relief for unintentional bookkeeping mistakes. It's an essential tool for any entity looking to realize its tax obligations accurately.