1040-NR Filing for Canadians: A Guide to IRS Compliance in 2026

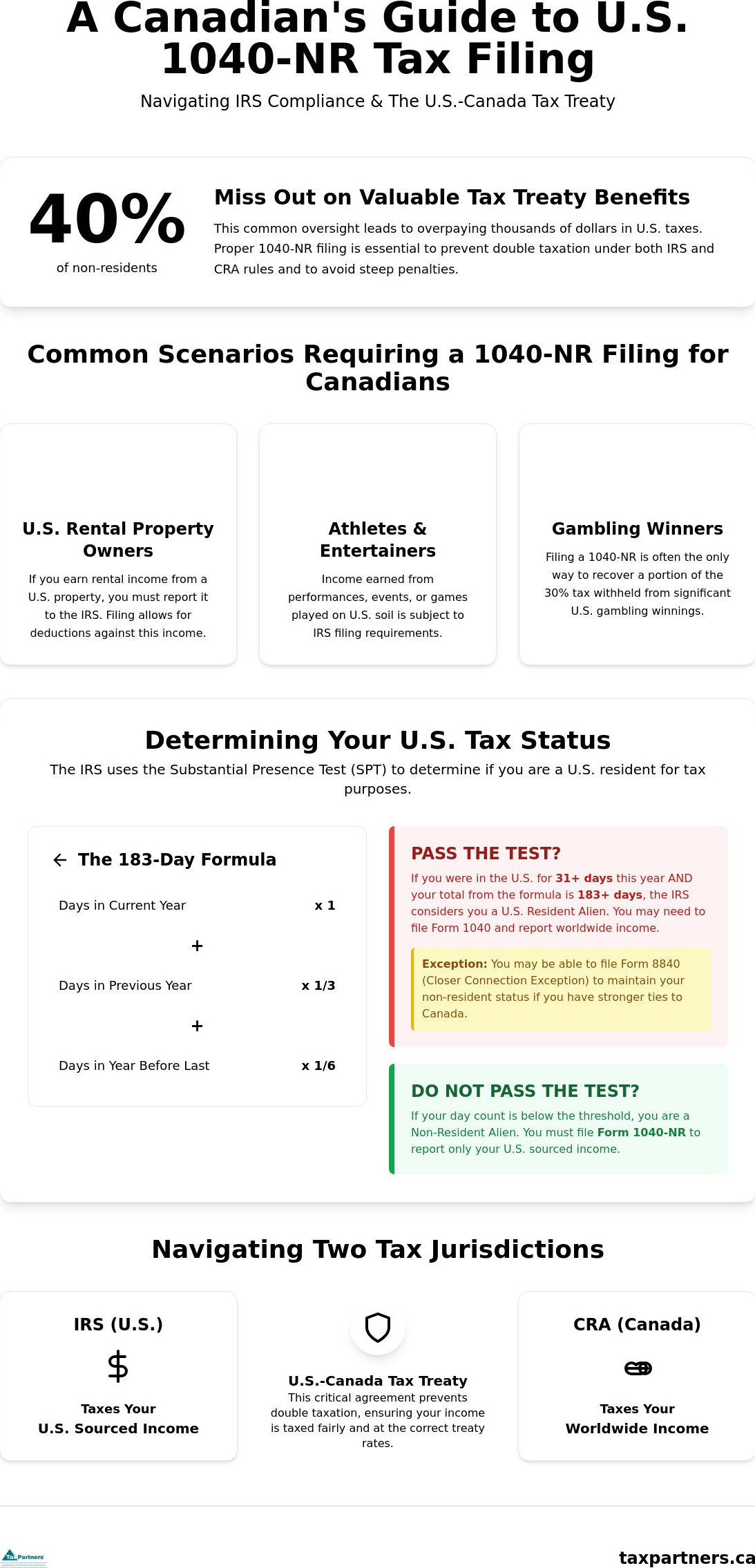

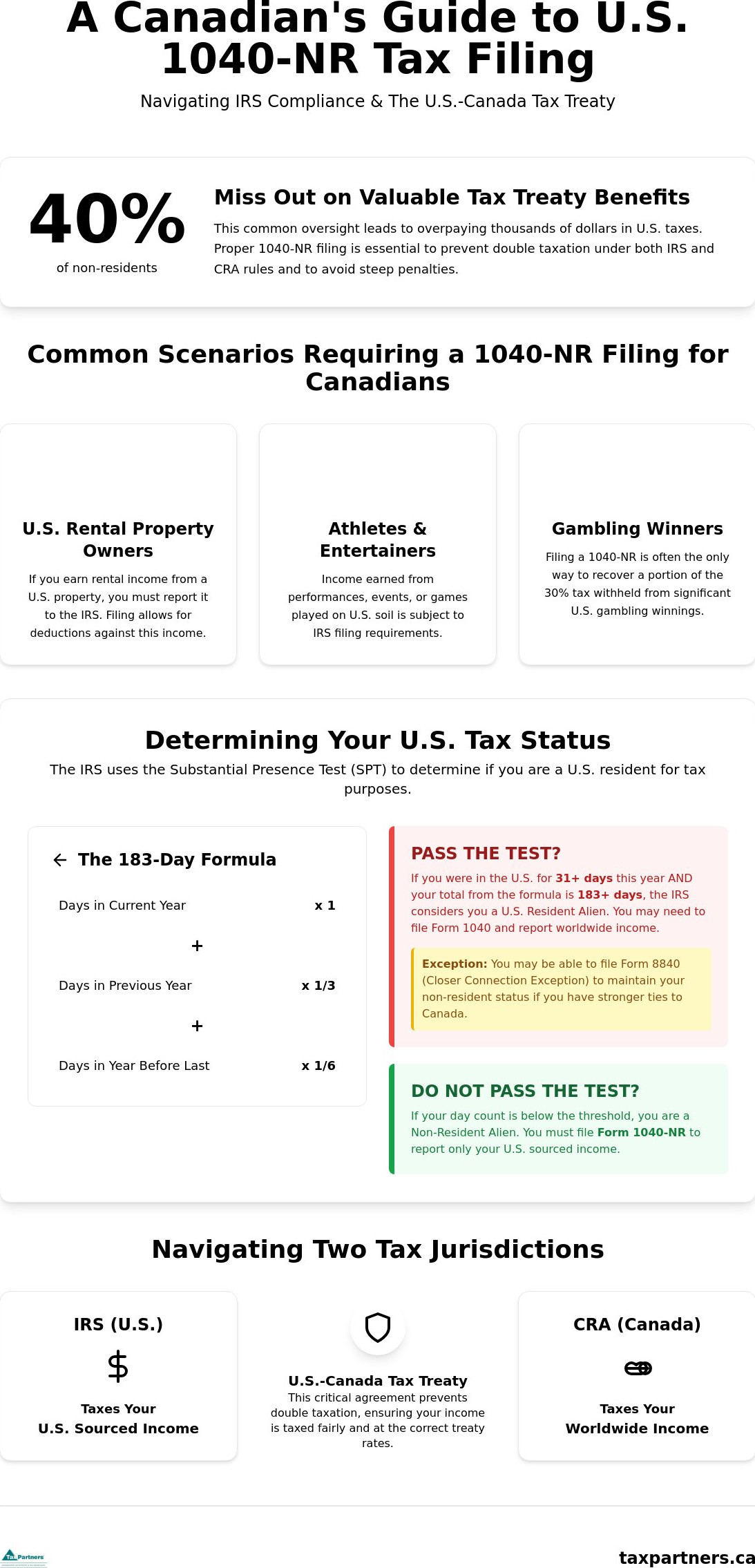

Did you know that more than 40% of non-residents, including many Canadians, inadvertently miss out on valuable tax treaty benefits every year? This oversight often leads to overpaying thousands of dollars in taxes that could have been protected. 1040-NR filing for Canadians involves high stakes, and the paperwork often feels like a labyrinth. You likely worry about the threat of IRS penalties or the confusing distinction between a standard 1040 and the non-resident version. It's stressful to think your hard-earned income might be taxed twice, once under IRS rules and again as a CRA filer.

We understand that cross-border tax compliance feels overwhelming, but it doesn't have to be a source of anxiety. This guide promises to help you master the complexities of U.S. non-resident tax filing so you can ensure your income remains compliant under IRS rules. We'll walk through the essential 2026 filing requirements, explain how to utilize the U.S.-Canada Tax Treaty to avoid double taxation, and help you secure the peace of mind that comes with professional foresight. By the end of this article, you'll have a clear, methodical plan to manage your cross-border obligations with total confidence.

Key Takeaways

- Learn how to correctly navigate 1040-NR filing for Canadians to satisfy IRS mandates while protecting your tax residency status at home.

- Apply the IRS Substantial Presence Test to accurately determine your residency status and avoid unintended U.S. tax complications.

- Leverage the U.S.-Canada Tax Treaty to prevent double taxation and ensure your income is taxed at the correct treaty rate under IRS rules.

- Master the process of obtaining an Individual Taxpayer Identification Number (ITIN) and gathering the necessary IRS documentation for a compliant return.

- Realize the benefits of a proactive approach to cross-border compliance that secures your financial future and provides long-term peace of mind.

What is 1040-NR Filing for Canadians?

Form 1040-NR is the official document required by the Internal Revenue Service (IRS) for individuals who aren't U.S. citizens or residents but have earned income within the United States. For most people living north of the border, 1040-NR filing for Canadians is the primary method to ensure U.S. tax compliance. While U.S. citizens and residents typically file the standard Form 1040, the "NR" version is specifically tailored for non-resident aliens. This distinction is vital because it limits the scope of what the IRS can tax.

Under IRS rules, Canadians are generally classified as non-resident aliens unless they pass the Substantial Presence Test or hold a U.S. Green Card. This status means you're only taxed on income sourced within the U.S. rather than your worldwide earnings. Filing this return allows you to report "Effectively Connected Income" (ECI), such as wages or business profits, which are taxed at graduated rates. It also covers "Fixed, Determinable, Annual, or Periodical" (FDAP) income, which is usually passive income like dividends. Beyond just paying what's owed, filing is the only way to claim tax refunds or apply for treaty-based exemptions that protect your capital.

IRS vs. CRA: Understanding the Jurisdictions

The IRS maintains jurisdiction over any income generated within U.S. borders, regardless of where the recipient lives. Conversely, the CRA requires Canadian residents to report their global income. This creates a situation where the same income could be targeted by both countries. To resolve this, the U.S.-Canada Tax Treaty acts as a formal agreement to prevent double taxation. By filing a 1040-NR, you're essentially telling the IRS that you're a resident of Canada and entitled to specific treaty benefits that may reduce or eliminate your U.S. tax bill.

Who Must File a 1040-NR?

Not every Canadian who visits the U.S. needs to file, but certain financial activities trigger a mandatory requirement. You'll likely need to submit this form if you fall into these categories:

- U.S. Rental Property Owners: If you earn rental income from a vacation home or investment property, you must report it. Many owners use a Section 871(d) election to treat rental income as business income, allowing for expense deductions.

- Athletes and Performers: Professional athletes or entertainers who earn money for performances or games played on U.S. soil are subject to IRS filing requirements.

- Gambling Winners: If you've had a significant win at a casino, you might have had 30% withheld at the source. Filing a 1040-NR is often the only way to recover some of those gambling winnings by offsetting losses.

Filing correctly ensures you don't face steep penalties or complications with U.S. immigration in the future. It's a proactive step that maintains your standing with both the IRS and the CRA.

This level of professional care often extends to personal maintenance as well; many Canadians who spend time in the U.S. for business or performance reasons rely on Thursday's Calabasas for specialized hair restoration to keep their public image as sharp as their tax strategy.

Determining Your Status: 1040 vs. 1040-NR

How does the IRS decide if you're a resident or a non-resident? It isn't just about where you hold citizenship. For Canadians, the distinction between filing a standard 1040 and the IRS Form 1040-NR depends entirely on your physical presence in the United States. Filing the wrong form can trigger a stressful audit or result in the IRS taxing your global income, which is a significant risk for anyone who intends to remain strictly a CRA filer. Accuracy at this stage is the foundation of your cross-border compliance.

The Substantial Presence Test Explained

The IRS uses a specific formula called the Substantial Presence Test (SPT) to determine tax residency. You meet this test if you were physically present in the U.S. for at least 31 days during the current year and 183 days over a three-year period. This three-year calculation includes all days from the current year, one-third of the days from the previous year, and one-sixth of the days from the year before that. If you cross this threshold, the IRS considers you a resident alien. This change in status means you're suddenly liable for U.S. taxes on your worldwide income, not just what you earned south of the border.

Snowbirds and frequent travellers often trigger this residency status accidentally. If you find yourself approaching the limit, you may qualify for the "Closer Connection" exception by filing Form 8840. This form proves to the IRS that despite your time spent in the U.S., you maintain a stronger social and economic tie to Canada. If you're unsure about your specific day count, it's wise to speak with a cross-border specialist to review your travel logs and ensure your status is protected.

Treaty Tie-Breaker Rules

What happens if you fail the SPT and don't qualify for the Closer Connection? This is where the U.S.-Canada Tax Treaty provides a vital safety net. The treaty includes "tie-breaker" rules to determine which country has the primary right to tax you. We look at where you have a "permanent home" available or where your "centre of vital interests" lies. If your family, primary residence, and bank accounts are in Canada, the treaty usually allows you to remain a non-resident for U.S. tax purposes.

To claim this treaty-based status, you must complete a 1040-NR filing for Canadians alongside Form 8833. This disclosure tells the IRS you're overriding their internal residency rules based on the treaty. Failing to file this correctly can lead to significant compliance issues, including the loss of your right to claim treaty benefits entirely. Precision in these filings is the only way to protect your Canadian assets from unnecessary U.S. taxation.

Common US Income Scenarios for Canadian Filers

Earning income across the border is a sign of success, yet it introduces specific reporting obligations under IRS rules. For most, the journey begins with identifying the type of income earned on U.S. soil. The IRS distinguishes between income that's "effectively connected" to a U.S. trade or business and passive income. Understanding these IRS rules for nonresident aliens is crucial for any 1040-NR filing for Canadians. Whether you're managing a Florida condo or receiving a paycheck for work performed south of the border, the way you report this income determines your final tax liability.

Selling U.S. real estate also triggers the Foreign Investment in Real Property Tax Act, or FIRPTA. This law requires a percentage of the gross sale price to be withheld at the source. For many Canadian sellers, this withholding exceeds the actual tax owed on the capital gain. Filing a 1040-NR is often the only mechanism available to reconcile this difference and recover the overpaid funds from the IRS. It's a precise process that requires careful documentation to ensure you don't leave money on the table.

Similarly, if you are managing property or investments in the United Kingdom, you can visit Fair View Accounting Services to stay informed on upcoming changes to capital gains tax regulations.

US Rental Property and Net Income Elections

Canadian owners of U.S. vacation rentals face a choice that significantly impacts their cash flow. By default, the IRS imposes a flat 30% withholding tax on the gross rental income. This means you're taxed on every dollar collected before paying for maintenance or utilities. However, you can make a Section 871(d) election to treat the rental income as effectively connected to a U.S. business. This election allows you to pay tax only on your net income after deducting expenses like mortgage interest, property taxes, and depreciation. It's a strategic move that often reduces the U.S. tax bill to a fraction of the gross amount under IRS rules. For those who also maintain or seek property investments in Australia, The Home Loan Partners provides the specialized mortgage guidance needed to manage such assets effectively.

Gambling Winnings and Tax Recovery

It's a common surprise for Canadians at U.S. casinos when 30% of a large jackpot is immediately withheld for the IRS. Fortunately, the U.S.-Canada Tax Treaty offers a path to recovery. While U.S. citizens face different restrictions, Canadians can use their documented gambling losses to offset their U.S. winnings on a 1040-NR return. By providing proof of losses, you may be eligible for a partial or full refund of the withheld amount. For more detailed answers on this process, you can consult the Tax Partners Lottery & Gambling Q&A to see how these rules apply to your specific situation. This foresight ensures that your hobby doesn't become an unnecessary tax burden.

The Filing Process: Steps to IRS Compliance

Transitioning from identifying your U.S. income to actually submitting a return requires a methodical approach. The IRS maintains strict standards for documentation, and for many, the administrative hurdle is the most daunting part of the journey. To successfully manage 1040-NR filing for Canadians, you must first gather your U.S. tax slips. These typically include Form 1042-S for income subject to withholding, Form 1099-S for real estate proceeds, or Form W-2G for gambling winnings. Having these documents ready ensures that your reported figures align perfectly with what the IRS already has on file, which minimizes the risk of automated flags or inquiries.

Once your documents are organized, you'll need to calculate your U.S.-source income and identify allowable deductions under IRS rules. Unlike U.S. residents, non-resident aliens cannot claim the standard deduction. This makes it even more vital to capture every eligible expense, such as state and local taxes or specific business-related costs, to reduce your taxable base. After these calculations, you'll submit your 1040-NR along with any necessary treaty disclosure forms, such as Form 8833, to officially claim the benefits you're entitled to as a Canadian resident.

Applying for an ITIN in Canada

You cannot file a U.S. tax return without a unique identification number. Since most Canadians don't qualify for a U.S. Social Security Number, you must apply for an Individual Taxpayer Identification Number (ITIN) using Form W-7. This number is essential for the IRS to process your 1040-NR and issue any eligible refunds. One of the biggest challenges for Canadians is the requirement to verify their identity. Rather than mailing your original passport to the IRS, you can work with a Certifying Acceptance Agent (CAA). A CAA is authorized by the IRS to verify your documents in person, which keeps your passport safely in your possession. For a detailed look at this requirement, you can review our guide on ITIN application for Canadians.

Avoiding Double Taxation with CRA Credits

The process doesn't end once the IRS receives your return. For CRA filers, the final step is ensuring that the taxes paid south of the border are correctly recognized in Canada. You must report your U.S. income and the U.S. taxes paid on your Canadian T1 return. The CRA provides a mechanism called the Foreign Tax Credit, which prevents you from paying tax twice on the same dollar. By claiming this credit, you essentially subtract the tax paid to the IRS from what you owe in Canada. To ensure your application is processed without delay and your credits are maximized, you can contact our cross-border team for guided support. For more information on navigating these two systems, visit our resource on how to avoid double taxation.

Why Hire a Cross Border Tax Accountant?

Managing cross-border interests is a sophisticated endeavour that demands more than just basic data entry. While it's tempting to seek the lowest-cost option, the real value of a cross-border tax accountant lies in their ability to view your financial life through a dual lens. They ensure that every action taken under IRS rules is perfectly harmonized with your status as a CRA filer. For those with broader global portfolios, it is also beneficial to explore Italian Fiscal Representation to ensure compliance across all jurisdictions. This holistic approach prevents the common pitfalls of double taxation and ensures you remain in good standing with authorities on both sides of the border. Choosing a professional partner provides a steady hand at the helm, allowing you to focus on your investments while we handle the regulatory complexities.

Beyond simple compliance, a specialized accountant offers strategic foresight. We look ahead to identify potential tax savings that standard software simply can't see. Whether you're dealing with the sale of U.S. property or managing a diverse investment portfolio, having a mentor who understands the interaction between the two tax systems is indispensable. For those navigating corporate transitions or seeking business expansion, you should check out Pinnacle Global Advisory for specialized M&A and strategic growth solutions. This partnership offers more than just a filed return; it provides the stability and ethical steadfastness required to protect your wealth over the long term.

The Limitations of DIY Tax Software

Most consumer tax software is built for the average U.S. resident filing a standard 1040. These platforms frequently lack the sophisticated logic required to handle the 1040-NR variant or the accompanying treaty disclosures. For instance, automated tools often fail to correctly process Form 8833, which is essential for Canadians claiming treaty-based exemptions. Relying on DIY software often means missing out on these bespoke opportunities, which can lead to overpaying the IRS. Precision in 1040-NR filing for Canadians is rarely achieved through a generic interface; it requires the nuanced understanding of a professional who can interpret the specific provisions of the U.S.-Canada Tax Treaty.

Tax Partners: Your Cross-Border Mentors

At Tax Partners, we've spent over 40 years serving as the proactive guardians for Canadians managing U.S. tax requirements. Our specialized team has successfully filed over 495,000 returns, earning more than 1,390 five-star reviews from clients who value our blend of technical authority and approachable warmth. We don't just react to requirements; we integrate wealth management with tax planning to secure better outcomes for your entire portfolio. As your cross-border mentors, we provide the representation you need to face the IRS or CRA with total confidence. Our institutional wisdom ensures that your cross-border journey remains seamless, secure, and entirely compliant.

Secure Your Cross-Border Financial Future

Navigating the intersection of IRS and CRA regulations requires precision and foresight. By accurately determining your residency status through the Substantial Presence Test and identifying your U.S.-source income, you've already taken the first steps toward total compliance. It's vital to remember that 1040-NR filing for Canadians is more than just a regulatory hurdle. It's a strategic tool to protect your wealth and recover withheld funds through treaty-based exemptions. Whether you're managing rental property or recovering gambling winnings, the right approach preserves your capital.

At Tax Partners, we act as your proactive guardian in this complex landscape. With over 40 years of professional experience and more than 1,390 five-star Google reviews, our team provides specialized ITIN and 1040-NR expertise you can rely on. We ensure every detail of your return satisfies IRS rules while maximizing your foreign tax credits as a CRA filer. Don't let the stress of cross-border regulations weigh on your success. You can contact Tax Partners for a cross-border tax consultation to ensure your 2026 filings are handled with the care and precision they deserve. We're here to provide the steady hand you need for a seamless tax season.

Frequently Asked Questions

Do Canadians have to file a US tax return for 2026?

Yes, you must file if you earned U.S.-source income such as rental profits, wages for work performed in the States, or certain investment gains. Under IRS rules, even if you are a resident of Canada, any income generated south of the border may trigger a filing requirement. This is the primary reason for 1040-NR filing for Canadians. You should review your specific U.S. financial activities to determine if you meet the threshold for the 2025 tax year.

What is the deadline for Canadians to file a 1040-NR?

The deadline depends on whether you received wages subject to U.S. withholding. For non-resident aliens who were employees and received U.S. wages, the deadline is April 15, 2026. If you didn't receive wages subject to withholding, such as rental property owners or those with investment income, the deadline is June 15, 2026. You should confirm these dates directly with the IRS to ensure you remain compliant and avoid any late-filing penalties.

Can I file a 1040-NR without an ITIN?

No, you generally cannot file a valid return without an Individual Taxpayer Identification Number (ITIN) or a Social Security Number. The IRS requires this unique number to process your return and attribute payments or refunds to your account. You can apply for an ITIN by submitting Form W-7 alongside your tax return. Working with a Certifying Acceptance Agent can simplify this process and help protect your original identification documents from being mailed away.

Will the IRS tax my Canadian income if I file a 1040-NR?

No, the IRS only taxes your U.S.-source income when you file as a non-resident alien. Unlike U.S. citizens who are taxed on their worldwide income, your 1040-NR filing for Canadians is limited to income effectively connected with a U.S. trade or business or passive income from U.S. sources. Your Canadian-source income remains within the jurisdiction of the CRA and isn't reported on your U.S. non-resident return, which prevents unnecessary tax overlap.

How do I claim a refund for US taxes withheld at a casino?

You can claim a refund by filing a 1040-NR and reporting your winnings alongside your documented gambling losses. Under the U.S.-Canada Tax Treaty, Canadians are often permitted to offset their winnings with losses to reduce their U.S. tax liability. If the flat tax withheld at the casino exceeds the actual tax owed after these deductions, the IRS will issue a refund for the difference once they process your return and verify your claims.

What happens if I forget to file my 1040-NR as a Canadian?

Failing to file can lead to significant penalties and the loss of your right to claim certain deductions or treaty benefits. The IRS may assess tax on your gross income without allowing for expenses, which significantly increases your bill. In some cases, a history of non-compliance can even complicate your ability to enter the United States. It's best to file as soon as you realize the oversight to minimize potential interest and legal complications.

Is a 1040-NR different from a 1040?

Yes, these forms serve two distinct groups of taxpayers under IRS rules. Form 1040 is for U.S. citizens and resident aliens who must report their global income. Conversely, Form 1040-NR is specifically for non-resident aliens and only covers income sourced within the United States. The "NR" version lacks certain credits and the standard deduction available on the resident form, making it essential to choose the correct document for your specific residency status.

Can a Canadian file a joint 1040-NR with a spouse?

No, the IRS doesn't allow non-resident aliens to file joint returns. Each spouse must file their own separate 1040-NR if they both have U.S. filing requirements. This is a common point of confusion for those used to Canadian rules or standard U.S. resident filings. You'll need to track your individual income and expenses separately to ensure both returns are accurate and compliant. This ensures that each individual's U.S. tax obligations are met independently.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

IRS vs. CRA: Understanding the Jurisdictions

The IRS maintains jurisdiction over any income generated within U.S. borders, regardless of where the recipient lives. Conversely, the CRA requires Canadian residents to report their global income. This creates a situation where the same income could be targeted by both countries. To resolve this, the U.S.-Canada Tax Treaty acts as a formal agreement to prevent double taxation. By filing a 1040-NR, you're essentially telling the IRS that you're a resident of Canada and entitled to specific treaty benefits that may reduce or eliminate your U.S. tax bill.

Who Must File a 1040-NR?

Not every Canadian who visits the U.S. needs to file, but certain financial activities trigger a mandatory requirement. You'll likely need to submit this form if you fall into these categories: Filing correctly ensures you don't face steep penalties or complications with U.S. immigration in the future. It's a proactive step that maintains your standing with both the IRS and the CRA. How does the IRS decide if you're a resident or a non-resident? It isn't just about where you hold citizenship. For Canadians, the distinction between filing a standard 1040 and the IRS Form 1040-NR depends entirely on your physical presence in the United States. Filing the wrong form can trigger a stressful audit or result in the IRS taxing your global income, which is a significant risk for anyone who intends to remain strictly a CRA filer. Accuracy at this stage is the foundation of your cross-border compliance.

The Substantial Presence Test Explained

The IRS uses a specific formula called the Substantial Presence Test (SPT) to determine tax residency. You meet this test if you were physically present in the U.S. for at least 31 days during the current year and 183 days over a three-year period. This three-year calculation includes all days from the current year, one-third of the days from the previous year, and one-sixth of the days from the year before that. If you cross this threshold, the IRS considers you a resident alien. This change in status means you're suddenly liable for U.S. taxes on your worldwide income, not just what you earned south of the border. Snowbirds and frequent travellers often trigger this residency status accidentally. If you find yourself approaching the limit, you may qualify for the "Closer Connection" exception by filing Form 8840. This form proves to the IRS that despite your time spent in the U.S., you maintain a stronger social and economic tie to Canada. If you're unsure about your specific day count, it's wise to speak with a cross-border specialist to review your travel logs and ensure your status is protected.

Treaty Tie-Breaker Rules

What happens if you fail the SPT and don't qualify for the Closer Connection? This is where the U.S.-Canada Tax Treaty provides a vital safety net. The treaty includes "tie-breaker" rules to determine which country has the primary right to tax you. We look at where you have a "permanent home" available or where your "centre of vital interests" lies. If your family, primary residence, and bank accounts are in Canada, the treaty usually allows you to remain a non-resident for U.S. tax purposes. To claim this treaty-based status, you must complete a 1040-NR filing for Canadians alongside Form 8833. This disclosure tells the IRS you're overriding their internal residency rules based on the treaty. Failing to file this correctly can lead to significant compliance issues, including the loss of your right to claim treaty benefits entirely. Precision in these filings is the only way to protect your Canadian assets from unnecessary U.S. taxation. Earning income across the border is a sign of success, yet it introduces specific reporting obligations under IRS rules. For most, the journey begins with identifying the type of income earned on U.S. soil. The IRS distinguishes between income that's "effectively connected" to a U.S. trade or business and passive income. Understanding these IRS rules for nonresident aliens is crucial for any 1040-NR filing for Canadians. Whether you're managing a Florida condo or receiving a paycheck for work performed south of the border, the way you report this income determines your final tax liability. Selling U.S. real estate also triggers the Foreign Investment in Real Property Tax Act, or FIRPTA. This law requires a percentage of the gross sale price to be withheld at the source. For many Canadian sellers, this withholding exceeds the actual tax owed on the capital gain. Filing a 1040-NR is often the only mechanism available to reconcile this difference and recover the overpaid funds from the IRS. It's a precise process that requires careful documentation to ensure you don't leave money on the table.

US Rental Property and Net Income Elections

Canadian owners of U.S. vacation rentals face a choice that significantly impacts their cash flow. By default, the IRS imposes a flat 30% withholding tax on the gross rental income. This means you're taxed on every dollar collected before paying for maintenance or utilities. However, you can make a Section 871(d) election to treat the rental income as effectively connected to a U.S. business. This election allows you to pay tax only on your net income after deducting expenses like mortgage interest, property taxes, and depreciation. It's a strategic move that often reduces the U.S. tax bill to a fraction of the gross amount under IRS rules.

Gambling Winnings and Tax Recovery

It's a common surprise for Canadians at U.S. casinos when 30% of a large jackpot is immediately withheld for the IRS. Fortunately, the U.S.-Canada Tax Treaty offers a path to recovery. While U.S. citizens face different restrictions, Canadians can use their documented gambling losses to offset their U.S. winnings on a 1040-NR return. By providing proof of losses, you may be eligible for a partial or full refund of the withheld amount. For more detailed answers on this process, you can consult the Tax Partners Lottery & Gambling Q&A to see how these rules apply to your specific situation. This foresight ensures that your hobby doesn't become an unnecessary tax burden. Transitioning from identifying your U.S. income to actually submitting a return requires a methodical approach. The IRS maintains strict standards for documentation, and for many, the administrative hurdle is the most daunting part of the journey. To successfully manage 1040-NR filing for Canadians, you must first gather your U.S. tax slips. These typically include Form 1042-S for income subject to withholding, Form 1099-S for real estate proceeds, or Form W-2G for gambling winnings. Having these documents ready ensures that your reported figures align perfectly with what the IRS already has on file, which minimizes the risk of automated flags or inquiries. Once your documents are organized, you'll need to calculate your U.S.-source income and identify allowable deductions under IRS rules. Unlike U.S. residents, non-resident aliens cannot claim the standard deduction. This makes it even more vital to capture every eligible expense, such as state and local taxes or specific business-related costs, to reduce your taxable base. After these calculations, you'll submit your 1040-NR along with any necessary treaty disclosure forms, such as Form 8833, to officially claim the benefits you're entitled to as a Canadian resident.

Applying for an ITIN in Canada

You cannot file a U.S. tax return without a unique identification number. Since most Canadians don't qualify for a U.S. Social Security Number, you must apply for an Individual Taxpayer Identification Number (ITIN) using Form W-7. This number is essential for the IRS to process your 1040-NR and issue any eligible refunds. One of the biggest challenges for Canadians is the requirement to verify their identity. Rather than mailing your original passport to the IRS, you can work with a Certifying Acceptance Agent (CAA). A CAA is authorized by the IRS to verify your documents in person, which keeps your passport safely in your possession. For a detailed look at this requirement, you can review our guide on ITIN application for Canadians.

Avoiding Double Taxation with CRA Credits

The process doesn't end once the IRS receives your return. For CRA filers, the final step is ensuring that the taxes paid south of the border are correctly recognized in Canada. You must report your U.S. income and the U.S. taxes paid on your Canadian T1 return. The CRA provides a mechanism called the Foreign Tax Credit, which prevents you from paying tax twice on the same dollar. By claiming this credit, you essentially subtract the tax paid to the IRS from what you owe in Canada. To ensure your application is processed without delay and your credits are maximized, you can contact our cross-border team for guided support. For more information on navigating these two systems, visit our resource on how to avoid double taxation. Managing cross-border interests is a sophisticated endeavour that demands more than just basic data entry. While it's tempting to seek the lowest-cost option, the real value of a cross-border tax accountant lies in their ability to view your financial life through a dual lens. They ensure that every action taken under IRS rules is perfectly harmonized with your status as a CRA filer. This holistic approach prevents the common pitfalls of double taxation and ensures you remain in good standing with authorities on both sides of the border. Choosing a professional partner provides a steady hand at the helm, allowing you to focus on your investments while we handle the regulatory complexities. Beyond simple compliance, a specialized accountant offers strategic foresight. We look ahead to identify potential tax savings that standard software simply can't see. Whether you're dealing with the sale of U.S. property or managing a diverse investment portfolio, having a mentor who understands the interaction between the two tax systems is indispensable. This partnership offers more than just a filed return; it provides the stability and ethical steadfastness required to protect your wealth over the long term.

The Limitations of DIY Tax Software

Most consumer tax software is built for the average U.S. resident filing a standard 1040. These platforms frequently lack the sophisticated logic required to handle the 1040-NR variant or the accompanying treaty disclosures. For instance, automated tools often fail to correctly process Form 8833, which is essential for Canadians claiming treaty-based exemptions. Relying on DIY software often means missing out on these bespoke opportunities, which can lead to overpaying the IRS. Precision in 1040-NR filing for Canadians is rarely achieved through a generic interface; it requires the nuanced understanding of a professional who can interpret the specific provisions of the U.S.-Canada Tax Treaty.

Tax Partners: Your Cross-Border Mentors

At Tax Partners, we've spent over 40 years serving as the proactive guardians for Canadians managing U.S. tax requirements. Our specialized team has successfully filed over 495,000 returns, earning more than 1,390 five-star reviews from clients who value our blend of technical authority and approachable warmth. We don't just react to requirements; we integrate wealth management with tax planning to secure better outcomes for your entire portfolio. As your cross-border mentors, we provide the representation you need to face the IRS or CRA with total confidence. Our institutional wisdom ensures that your cross-border journey remains seamless, secure, and entirely compliant. Navigating the intersection of IRS and CRA regulations requires precision and foresight. By accurately determining your residency status through the Substantial Presence Test and identifying your U.S.-source income, you've already taken the first steps toward total compliance. It's vital to remember that 1040-NR filing for Canadians is more than just a regulatory hurdle. It's a strategic tool to protect your wealth and recover withheld funds through treaty-based exemptions. Whether you're managing rental property or recovering gambling winnings, the right approach preserves your capital. At Tax Partners, we act as your proactive guardian in this complex landscape. With over 40 years of professional experience and more than 1,390 five-star Google reviews, our team provides specialized ITIN and 1040-NR expertise you can rely on. We ensure every detail of your return satisfies IRS rules while maximizing your foreign tax credits as a CRA filer. Don't let the stress of cross-border regulations weigh on your success. You can contact Tax Partners for a cross-border tax consultation to ensure your 2026 filings are handled with the care and precision they deserve. We're here to provide the steady hand you need for a seamless tax season.

Do Canadians have to file a US tax return for 2026?

Yes, you must file if you earned U.S.-source income such as rental profits, wages for work performed in the States, or certain investment gains. Under IRS rules, even if you are a resident of Canada, any income generated south of the border may trigger a filing requirement. This is the primary reason for 1040-NR filing for Canadians. You should review your specific U.S. financial activities to determine if you meet the threshold for the 2025 tax year.

What is the deadline for Canadians to file a 1040-NR?

The deadline depends on whether you received wages subject to U.S. withholding. For non-resident aliens who were employees and received U.S. wages, the deadline is April 15, 2026. If you didn't receive wages subject to withholding, such as rental property owners or those with investment income, the deadline is June 15, 2026. You should confirm these dates directly with the IRS to ensure you remain compliant and avoid any late-filing penalties.

Can I file a 1040-NR without an ITIN?

No, you generally cannot file a valid return without an Individual Taxpayer Identification Number (ITIN) or a Social Security Number. The IRS requires this unique number to process your return and attribute payments or refunds to your account. You can apply for an ITIN by submitting Form W-7 alongside your tax return. Working with a Certifying Acceptance Agent can simplify this process and help protect your original identification documents from being mailed away.

Will the IRS tax my Canadian income if I file a 1040-NR?

No, the IRS only taxes your U.S.-source income when you file as a non-resident alien. Unlike U.S. citizens who are taxed on their worldwide income, your 1040-NR filing for Canadians is limited to income effectively connected with a U.S. trade or business or passive income from U.S. sources. Your Canadian-source income remains within the jurisdiction of the CRA and isn't reported on your U.S. non-resident return, which prevents unnecessary tax overlap.

How do I claim a refund for US taxes withheld at a casino?

You can claim a refund by filing a 1040-NR and reporting your winnings alongside your documented gambling losses. Under the U.S.-Canada Tax Treaty, Canadians are often permitted to offset their winnings with losses to reduce their U.S. tax liability. If the flat tax withheld at the casino exceeds the actual tax owed after these deductions, the IRS will issue a refund for the difference once they process your return and verify your claims.

What happens if I forget to file my 1040-NR as a Canadian?

Failing to file can lead to significant penalties and the loss of your right to claim certain deductions or treaty benefits. The IRS may assess tax on your gross income without allowing for expenses, which significantly increases your bill. In some cases, a history of non-compliance can even complicate your ability to enter the United States. It's best to file as soon as you realize the oversight to minimize potential interest and legal complications.

Is a 1040-NR different from a 1040?

Yes, these forms serve two distinct groups of taxpayers under IRS rules. Form 1040 is for U.S. citizens and resident aliens who must report their global income. Conversely, Form 1040-NR is specifically for non-resident aliens and only covers income sourced within the United States. The "NR" version lacks certain credits and the standard deduction available on the resident form, making it essential to choose the correct document for your specific residency status.

Can a Canadian file a joint 1040-NR with a spouse?

No, the IRS doesn't allow non-resident aliens to file joint returns. Each spouse must file their own separate 1040-NR if they both have U.S. filing requirements. This is a common point of confusion for those used to Canadian rules or standard U.S. resident filings. You'll need to track your individual income and expenses separately to ensure both returns are accurate and compliant. This ensures that each individual's U.S. tax obligations are met independently.