Late Tax Filing Assistance: A Guide to Catching Up with the CRA in 2026

What if the mounting pressure of unfiled tax returns didn't have to end in a financial crisis? For many CRA filers, the fear of compounding interest and frozen benefits like the Canada Child Benefit (CCB) creates a cycle of anxiety that only makes the situation worse. You likely realize that the Canada Revenue Agency (CRA) charges a 7% annual interest rate on overdue taxes as of July 2026, and that daily compounding can quickly turn a manageable balance into a significant burden. It's understandable to feel overwhelmed when you're missing original documents or facing a 5% late-filing penalty, but you don't have to face this process alone.

This guide provides the professional late tax filing assistance you need to navigate these complexities, minimize penalties, and restore your financial standing. We will explore how to stop the growth of daily interest, apply for relief through the Voluntary Disclosures Program (VDP), and organize your records to get back into good standing. By taking proactive steps today, you can move from a state of uncertainty toward total control over your tax obligations.

Key Takeaways

- Understand the financial consequences of missing CRA deadlines, including daily compounded interest and the risk of losing essential benefits like the Canada Child Benefit (CCB).

- Learn why filing your return as soon as possible is the most effective strategy to stop the accumulation of monthly late-filing penalties for CRA filers.

- Discover how professional late tax filing assistance can help you leverage the Voluntary Disclosures Program (VDP) to fix past errors before any enforcement action begins.

- Identify the specific steps needed to organize missing tax slips and receipts to restore your standing with the CRA and regain control over your financial future.

- Explore how a seasoned CPA acts as a proactive guardian, using institutional wisdom to negotiate on your behalf and apply for potential penalty and interest relief.

Understanding the Impact of Late Tax Filing for CRA Filers

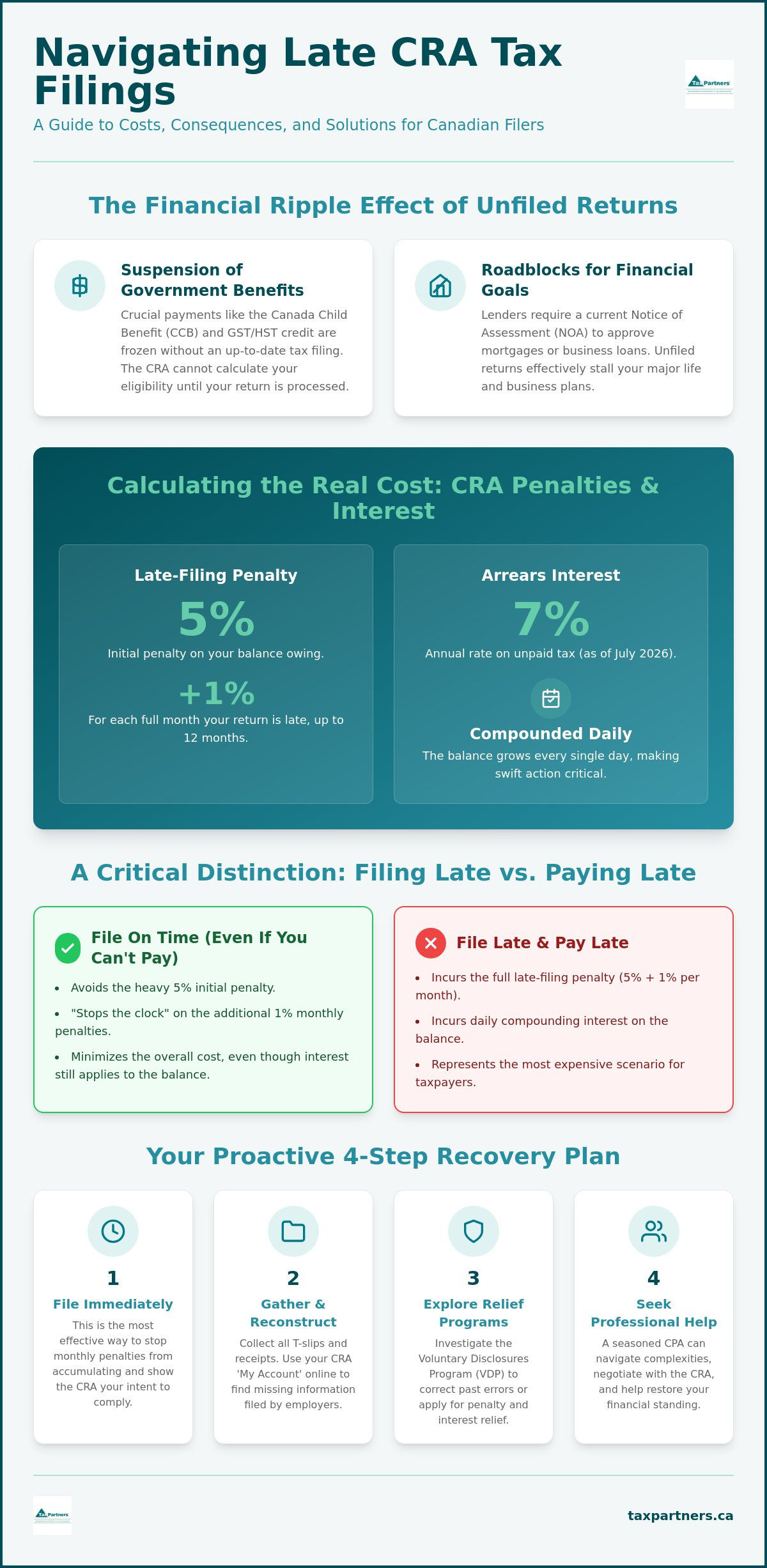

Missing a tax deadline within the Canadian tax system is more than a simple clerical error. For CRA filers, late filing occurs the moment you pass the prescribed deadline for your specific category without submitting your return. The Canada Revenue Agency (CRA) prioritizes compliance because your tax return serves as the primary data source for the "Notice of Assessment" (NOA). This document is far more than just a receipt; it's a financial passport. Without a current NOA, your financial life can effectively stall.

The impact often creates a ripple effect that touches your daily budget. Government benefits, such as the Canada Child Benefit (CCB) or the GST/HST credit, rely on your latest income data. If you haven't filed, the CRA cannot calculate your eligibility, which frequently leads to a total suspension of these payments until the records are updated. Beyond benefits, unfiled returns are a major red flag for lenders. If you're trying to secure a mortgage or a business loan in 2026, a bank will almost certainly demand your most recent NOAs to verify your income. Seeking professional late tax filing assistance early can prevent these systemic roadblocks before they become permanent financial hurdles.

The Distinction Between Filing Late and Paying Late

It's a common misconception that you should wait to file until you have the money to pay. In reality, filing the return and paying the balance are two separate legal obligations. Filing on time allows you to avoid the initial 5% late-filing penalty, even if you can't pay the full balance immediately. If you miss the deadline and owe a balance, the CRA applies "arrears interest." This is essentially a daily compounded charge on any unpaid tax from the day after the return was due. As of July 2026, this rate sits at 7%, making it a costly expense that grows every single day.

Impact on Self-Employed Individuals and SMEs

Self-employed individuals often feel a false sense of security due to the June 15th filing deadline. While you have more time to submit the paperwork, the CRA requires any balance owing to be paid by April 30th. Missing this date triggers interest charges immediately. For small business owners, the risks extend to GST/HST filings. Late submissions here can lead to aggressive collection actions and jeopardize your business's reputation with regulators. For those managing more complex structures, understanding Canadian corporate tax compliance is vital to ensuring that personal filing delays don't bleed into your company's regulatory standing.

Immediate Steps to Take When You Miss the CRA Deadline

Discovering that you've missed a tax deadline can trigger an immediate sense of panic. However, the most effective way to manage the situation is through swift, decisive action. Your priority should be gathering all available documentation, including T4 slips for employment income, T5 slips for investment income, and any receipts for deductible expenses. Even if you feel your records are incomplete, starting the consolidation process immediately allows you to assess the scope of your filing requirements for the CRA.

The urgency to file cannot be overstated. The CRA applies a late-filing penalty of 5% on any balance owing, but the real financial drain often comes from the additional 1% charged for each full month the return is late, up to 12 months. By filing as soon as possible, you effectively "stop the clock" on these escalating monthly charges. Professional late tax filing assistance can help you navigate this high-pressure window, ensuring that your prior-year returns are prepared accurately to avoid further scrutiny or future audits. Communicating your intent to comply with the CRA early often demonstrates a proactive attitude, which is beneficial if you later need to request relief.

What to Do if You Are Missing Tax Slips

If you don't have all your original documents, you can often retrieve missing information through the CRA "My Account" portal. This digital service provides access to most tax slips that have been filed by employers or financial institutions on your behalf. In cases where slips are entirely unavailable, a CPA can assist by reconstructing your financial history through professional bookkeeping and bank statement analysis. It's often better to file an estimated return to meet a deadline than to provide no information at all, as you can always adjust the return once the final data is secured.

Setting Up a CRA Payment Arrangement

If you find yourself with a balance you cannot pay in full, the CRA offers a "payment arrangement." This is a formal agreement where you commit to paying your tax debt over a specific period through manageable installments. While setting up an arrangement helps you stay in good standing and prevents aggressive collection actions, it's vital to remember that interest continues to accrue. As of July 2026, the CRA charges a 7% annual interest rate on overdue taxes, compounded daily. Understanding the full scope of CRA penalties and interest is the first step toward creating a realistic repayment plan that protects your long-term financial health.

Calculating the Real Cost: CRA Penalties and Interest Explained

Understanding the financial consequences of a missed deadline is essential for every taxpayer. For CRA filers who owe a balance, the immediate penalty is 5% of the total amount owing. This is just the starting point. The CRA then adds an additional 1% for every full month the return remains unfiled, up to a maximum of 12 months. While these percentages might seem small in isolation, they represent a significant surcharge on your existing debt. If you are struggling to quantify these costs, seeking professional late tax filing assistance can provide the clarity needed to stop the financial bleeding.

The situation becomes considerably more severe for those the CRA identifies as repeat late filers. If the Agency has issued a demand to file for any of the previous three tax years, the penalties effectively double. In these instances, the initial late-filing penalty jumps to 10% of the balance owing. The monthly increase also rises to 2% for each full month the return is late, extending to a maximum of 20 months. This aggressive structure is designed to discourage chronic non-compliance, but it can quickly lead to a debt spiral that feels impossible to escape without expert intervention.

There is a small measure of relief for those expecting a refund. Generally, if you don't owe any tax to the federal government, the CRA does not apply a penalty for filing your return late. However, delaying your submission still carries the "ripple effect" mentioned earlier, such as the suspension of essential benefits. It's always better to file and confirm your standing than to leave your accounts in a state of uncertainty.

How the CRA Compounds Interest Daily

Daily compounding interest is a calculation method where the CRA applies interest to both the principal tax amount and the total accumulated interest and penalties from all previous days. This means your debt grows every 24 hours. The Agency also charges interest on the late-filing penalties themselves, not just the tax you originally owed. As of the third quarter of 2026, the annual interest rate on overdue taxes is 7%. Because these rates are set quarterly by the federal government, you should check the official CRA website or consult with a professional to confirm the most current figures.

The Risk of Arbitrary Assessments

If you remain non-compliant for too long, the CRA may invoke Section 152(7) of the Income Tax Act to issue an "arbitrary assessment." This occurs when the Agency files a return on your behalf based on their own estimates of your income. Because the CRA doesn't have access to your specific deductions or expenses, these assessments are almost always significantly higher than what you would actually owe. Correcting an arbitrary assessment is a complex process that often requires detailed CRA audit help to ensure your actual financial situation is accurately reflected and the inflated debt is reduced.

Strategic Relief: The Voluntary Disclosure Program (VDP)

For many CRA filers, the realization that they are years behind on their taxes feels like a dead end. However, the Voluntary Disclosure Program (VDP) serves as a strategic "second chance" to correct past omissions before the Agency discovers them. This program is a proactive tool designed to encourage compliance by offering significant relief to those who come forward. If you qualify, the CRA may grant 100% penalty relief and up to 75% interest relief for unprompted applications received on or after October 1, 2025. This is a powerful mechanism for anyone seeking late tax filing assistance to wipe the slate clean and avoid the threat of prosecution or the maximum repeat-filer penalties discussed earlier.

The defining characteristic of this program is the "voluntary" requirement. You must submit your application before the CRA initiates any enforcement action or contacts you regarding the specific tax issue. Once the Agency has prompted a disclosure, the level of relief drops. For prompted disclosures, you may still receive up to 100% penalty relief, but interest relief is typically capped at 25%. This distinction underscores why acting quickly is the most effective way to protect your wealth and your reputation with the federal government. Waiting for the CRA to find the error removes your best opportunity for financial mercy.

Eligibility Requirements for VDP

To be accepted into the program, your application must meet four specific criteria. First, it must be voluntary. Second, it must be complete, meaning you disclose all previously omitted information for all relevant tax years. Third, the disclosure must involve a penalty. Finally, the information being provided must be at least one year past the filing deadline. Because the CRA scrutinizes these applications strictly, professional representation is highly recommended. A seasoned CPA ensures your submission is comprehensive and framed correctly to maximize your chances of acceptance.

Extraordinary Circumstances and Fairness

Outside of the VDP, the CRA also provides "Taxpayer Relief Provisions" for those who missed deadlines due to factors beyond their control. This program allows you to request the cancellation of interest and penalties if you've faced extraordinary circumstances. These include serious illness, a death in the immediate family, or natural disasters such as floods or fires. There is a 10-year limitation period for these requests, and the CRA maintains full discretion to grant or deny them based on the evidence provided. If you believe your situation warrants this level of fairness, contact our team for late tax filing assistance to begin building your case for relief.

How Professional Late Tax Filing Assistance Simplifies Recovery

Recovery is possible. When you face years of unfiled returns, the most valuable asset you can have is a steady hand at the helm. At Tax Partners, we bring over 40 years of institutional wisdom to every case, having filed more than 495,000 returns for CRA filers. This deep-seated experience allows us to act as a proactive guardian between you and the tax authorities. By positioning a CPA as your primary point of contact, you create a professional buffer that alleviates the stress of direct CRA correspondence. Our role is to ensure that every interaction is handled with precision, protecting your interests while restoring your standing.

Accuracy is the foundation of a successful recovery. Filing "back taxes" isn't just about submitting old forms; it's about doing so in a way that avoids future "red flags" and potential audits. We take a mentor-like approach, offering non-judgmental support to individuals who have fallen behind. Our team has saved clients over $87M by ensuring that every return is optimized and compliant. This level of late tax filing assistance transforms a daunting legal obligation into a manageable step-by-step process, moving you quickly from uncertainty to a sense of total control.

A Methodical Approach to Back Taxes

Reconstructing years of financial history requires professional precision. We don't just guess at figures; we use a methodical process to gather data and verify every line item. This often involves integrating professional bookkeeping to ensure that your records are not only caught up but organized for future compliance. During this reconstruction, we frequently identify missed deductions and credits that the CRA's arbitrary assessments often ignore. These discoveries can significantly lower the balance you owe, making your total debt much more manageable than you originally feared.

Beyond Filing: Long-Term Financial Health

The journey doesn't end with a single submission. Once your accounts are in good standing, you gain the freedom to focus on tax-efficient wealth management and long-term security. Total regulatory adherence provides a unique kind of peace of mind, allowing you to apply for mortgages, secure business loans, and receive government benefits without the constant fear of a CRA intervention. We remain invested in your success well after the initial crisis has passed, acting as a long-term partner in your financial stability. Contact Tax Partners today for a confidential consultation and let us help you secure a better outcome.

Secure Your Financial Standing with Confidence

Navigating unfiled returns for CRA filers doesn't have to be a source of permanent stress. Recovery is possible. By filing as soon as possible, you stop the accumulation of monthly penalties and prevent the CRA from issuing arbitrary assessments that often inflate your debt. Whether you're applying for the Voluntary Disclosure Program or seeking relief from daily compounded interest, taking action today is the only way to restore your access to essential government benefits and clear your path toward future wealth management.

Our team at Tax Partners provides the sophisticated late tax filing assistance you need to resolve complex regulatory hurdles. With over 495,000 returns filed and more than $87M saved for our clients, we bring deep-seated reliability to every case. Our 1,390+ five-star Google reviews reflect our commitment to acting as a non-judgmental mentor during difficult financial times. Don't let tax debt define your future when a better outcome is within reach. Get expert late tax filing assistance from Tax Partners and regain total control over your financial life today.

Frequently Asked Questions

What happens if I don't file my Canadian taxes for several years?

If you don't file for several years, the CRA may issue an arbitrary assessment under Section 152(7) of the Income Tax Act. This is an estimation of your income that usually results in a higher tax bill than necessary because it doesn't account for your specific deductions or credits. Daily compounded interest and monthly penalties will continue to grow on these estimated amounts until the returns are officially settled and corrected.

Can I go to jail for filing my taxes late in Canada?

Filing late is generally treated as a civil matter, but you can face criminal prosecution and potential jail time if you ignore a formal requirement to file or commit tax evasion. The CRA prioritizes compliance through financial penalties first. Engaging with professional late tax filing assistance early helps you enter programs like the Voluntary Disclosures Program (VDP), which can protect you from criminal charges and prosecution.

Will the CRA freeze my bank account if I have unfiled returns?

The CRA has the legal authority to freeze your bank account or garnish your wages to recover unpaid tax debts. These aggressive collection actions usually happen after the Agency has issued multiple notices or assessments that have been ignored. Filing your returns and establishing a formal payment arrangement is the most effective way to prevent these legal seizures and maintain control over your finances.

How far back can I file my taxes with the CRA?

You can technically file your taxes for any previous year, but the CRA generally limits Taxpayer Relief and refund claims to the last 10 calendar years. If you're filing to catch up on a long history of non-compliance, it's vital to prioritize the most recent years first. This strategy helps restore your eligibility for current benefits and ensures you are meeting the most urgent regulatory requirements.

Is there a way to reduce the interest I owe to the CRA?

You can reduce the interest you owe by applying for the Voluntary Disclosures Program (VDP) or submitting a Taxpayer Relief request. As of July 2026, the VDP can provide up to 75% interest relief for unprompted applications. If your delay was caused by extraordinary circumstances like a serious illness or natural disaster, the CRA may cancel the interest and penalties entirely under fairness provisions.

What is the "repeat filer" penalty and how do I avoid it?

The repeat filer penalty is a heavy surcharge that applies if the CRA issued a demand to file for any of the three previous tax years. In these cases, the penalty doubles to 10% of the balance owing plus 2% for each full month the return is late. You can avoid this escalating cost by filing all outstanding returns immediately before the Agency issues another formal demand for information.

Do I still need to file if I don't have the money to pay my tax bill?

You should always file your return on time even if you don't have the money to pay the balance. Filing prevents the 5% late-filing penalty from being applied to your debt, which saves you money immediately. Once the CRA processes your return, you can negotiate a payment arrangement to pay the balance in manageable installments while stopping further aggressive collection actions.

How does late filing affect my Canada Child Benefit (CCB)?

Late filing will cause your Canada Child Benefit (CCB) payments to stop completely. The CRA uses the information from your annual tax return to calculate your benefit entitlement for the following year. If they don't have your updated income data, they cannot issue the payments, which often leads to a significant and stressful gap in your monthly household budget.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26 years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance. Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014. Tax Partners has 44 full-time accountants and over 18,400 clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

What happens if I don't file my Canadian taxes for several years?

If you don't file for several years, the CRA may issue an arbitrary assessment under Section 152(7) of the Income Tax Act. This is an estimation of your income that usually results in a higher tax bill than necessary because it doesn't account for your specific deductions or credits. Daily compounded interest and monthly penalties will continue to grow on these estimated amounts until the returns are officially settled and corrected.

Can I go to jail for filing my taxes late in Canada?

Filing late is generally treated as a civil matter, but you can face criminal prosecution and potential jail time if you ignore a formal requirement to file or commit tax evasion. The CRA prioritizes compliance through financial penalties first. Engaging with professional late tax filing assistance early helps you enter programs like the Voluntary Disclosures Program (VDP), which can protect you from criminal charges and prosecution.

Will the CRA freeze my bank account if I have unfiled returns?

The CRA has the legal authority to freeze your bank account or garnish your wages to recover unpaid tax debts. These aggressive collection actions usually happen after the Agency has issued multiple notices or assessments that have been ignored. Filing your returns and establishing a formal payment arrangement is the most effective way to prevent these legal seizures and maintain control over your finances.

How far back can I file my taxes with the CRA?

You can technically file your taxes for any previous year, but the CRA generally limits Taxpayer Relief and refund claims to the last 10 calendar years. If you're filing to catch up on a long history of non-compliance, it's vital to prioritize the most recent years first. This strategy helps restore your eligibility for current benefits and ensures you are meeting the most urgent regulatory requirements.

Is there a way to reduce the interest I owe to the CRA?

You can reduce the interest you owe by applying for the Voluntary Disclosures Program (VDP) or submitting a Taxpayer Relief request. As of July 2026, the VDP can provide up to 75% interest relief for unprompted applications. If your delay was caused by extraordinary circumstances like a serious illness or natural disaster, the CRA may cancel the interest and penalties entirely under fairness provisions.

What is the "repeat filer" penalty and how do I avoid it?

The repeat filer penalty is a heavy surcharge that applies if the CRA issued a demand to file for any of the three previous tax years. In these cases, the penalty doubles to 10% of the balance owing plus 2% for each full month the return is late. You can avoid this escalating cost by filing all outstanding returns immediately before the Agency issues another formal demand for information.

Do I still need to file if I don't have the money to pay my tax bill?

You should always file your return on time even if you don't have the money to pay the balance. Filing prevents the 5% late-filing penalty from being applied to your debt, which saves you money immediately. Once the CRA processes your return, you can negotiate a payment arrangement to pay the balance in manageable installments while stopping further aggressive collection actions.

How does late filing affect my Canada Child Benefit (CCB)?

Late filing will cause your Canada Child Benefit (CCB) payments to stop completely. The CRA uses the information from your annual tax return to calculate your benefit entitlement for the following year. If they don't have your updated income data, they cannot issue the payments, which often leads to a significant and stressful gap in your monthly household budget.