CPA for Medical Professionals: Strategic Accounting for Canadian Healthcare

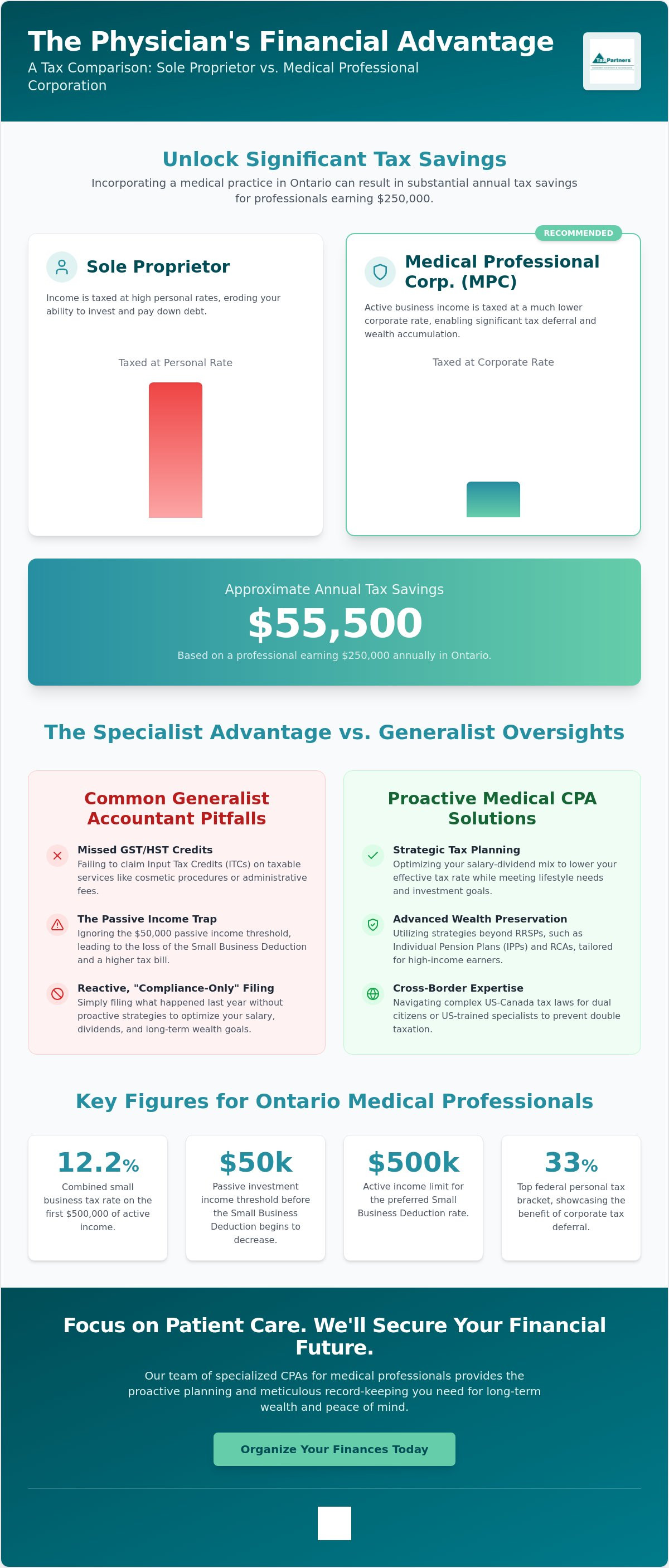

Did you know that incorporating a medical practice in Ontario can save a professional earning $250,000 approximately $55,500 in taxes annually compared to operating as a sole proprietor? You likely entered medicine to focus on patient outcomes, not to spend your limited free time deciphering the complexities of medical billing or the nuances of GST/HST exemptions. It's often overwhelming to balance a demanding clinical schedule while worrying if your high personal tax bracket is eroding your ability to pay down student debt or invest for the future. Finding a specialized CPA for medical professionals is the first step toward reclaiming your time and your financial peace of mind.

We understand that your financial needs are as unique as your clinical practice. This guide will show you how to transform your accounting from a simple year-end filing task into a proactive strategy that protects your assets and significantly lowers your effective tax rate. We'll explore the strategic use of professional corporations under 2026 tax regulations and provide a clear roadmap for your retirement and eventual succession. By the end of this article, you'll have the clarity needed to organize your corporate records and secure your long-term wealth with confidence.

Key Takeaways

- Learn why a generalist accountant might overlook critical deductions and how a specialized CPA for medical professionals provides proactive planning to lower your effective tax rate.

- Discover how to maximize the tax deferral benefits of a Medical Professional Corporation while remaining compliant with evolving Tax on Split Income (TOSI) regulations.

- Navigate the intricate cross-border filing requirements for US-trained specialists and dual citizens to ensure you are fully protected from double taxation.

- Explore advanced wealth preservation strategies beyond the RRSP, such as Individual Pension Plans (IPPs) and Retirement Compensation Arrangements (RCAs), tailored for high-income earners.

- Understand the value of a steady, experienced hand in managing your corporate records, allowing you to focus on patient care while your long-term financial roadmap is secured.

Why Generalist Accounting Often Fails Medical Professionals

A generalist accountant often views your practice through the same lens as a retail shop or a small consultancy. While they might handle the basics of your annual return, they frequently miss the specific nuances of the Canadian healthcare sector. A specialized CPA for medical professionals acts as a strategic partner, understanding that your financial health is tied to specific regulatory frameworks and complex billing systems. They don't just record what happened; they anticipate what's coming. This proactive stance is the difference between simply filing taxes and building a resilient financial legacy.

One of the most significant oversights involves the initial setup and ongoing management of a Professional Corporation. If this structure is poorly organized, you risk losing the flexibility needed to manage your income effectively. Generalists often focus on "compliance only," which means they ensure you follow the basic rules but don't necessarily optimize your position within them. In contrast, proactive planning involves looking at your debt levels, lifestyle needs, and long-term wealth goals to decide exactly how much to pay out in salary versus dividends. Missing these opportunities can lead to thousands of dollars in unnecessary tax leakage every year.

The Complexity of Medical Billing and GST/HST

Healthcare billing is rarely straightforward. Most medical services are exempt from GST/HST, but many modern practices offer taxable supplies like cosmetic procedures, administrative fees, or certain medical reports. If your bookkeeping doesn't synchronize perfectly with your provincial billing cycles, you're likely missing out on Input Tax Credits (ITCs). These credits allow you to recover the GST/HST paid on expenses related to your taxable activities. For travelling specialists, "place of supply" rules become vital. If you provide services across provincial borders, the tax rates and reporting requirements change. Precision in these areas is non-negotiable for maintaining clean corporate records.

The High-Income Trap: Moving Beyond Basic Tax Filing

High-earning physicians are frequently flagged for CRA audits, especially regarding the blurred lines between personal and business expenses. Whether it's a home office claim or travel for a conference, a specialized CPA for medical professionals ensures every deduction is defensible and documented. This reduces the stress of potential scrutiny and keeps your focus on patient care.

Perhaps the most dangerous pitfall is the passive income threshold. Once your corporation's passive investment income exceeds $50,000, your Small Business Deduction begins to decrease. At $150,000, it's eliminated entirely. This "grind-down" can increase your corporate tax bill significantly if not managed with foresight. A generalist might only notice this after the year-end, whereas a specialist monitors these levels throughout the year. Ultimately, the right advisor protects your time as much as your money. You shouldn't be reconciling spreadsheets after a twelve-hour shift; you should be resting or with your family while your financial guardian handles the details.

Maximizing the Benefits of a Medical Professional Corporation (MPC)

Incorporating your practice isn't just a legal formality; it's a strategic move that fundamentally changes your wealth trajectory. A Medical Professional Corporation (MPC) allows you to separate your personal finances from your practice's active business income. This separation is crucial because the tax rates applied to corporations are significantly lower than those for high-earning individuals. In 2026, the Ontario combined small business tax rate sits at just 12.2% on the first $500,000 of active income. Compare this to the top federal personal tax bracket of 33% for income over $258,482, and the advantage becomes clear. By working with a specialized CPA for medical professionals, you can ensure your MPC is structured to capture these savings while protecting your personal assets from general commercial liabilities.

While an MPC offers robust protection for business debts or lease obligations, it doesn't shield you from professional malpractice claims. However, the ability to retain earnings within the company provides a financial buffer that sole proprietors lack. The Small Business Deduction alone can save an Ontario medical practice up to $85,000 in taxes annually. These are funds that can be used to pay down practice-related debt or expand your clinic's capabilities. Navigating the strict Tax on Split Income (TOSI) rules is also essential, as the CRA continues to rigorously limit the ability to sprinkle income to family members who aren't actively involved in the business.

Tax Deferral: Your Most Powerful Wealth-Building Tool

Tax deferral remains the primary engine for growth within an MPC. When you earn income personally, you pay tax at your marginal rate before you can invest the remainder. Inside a corporation, you only pay the low corporate rate, leaving significantly more capital available to grow. This can result in tax savings of approximately 30% to 40% annually compared to a sole proprietorship. Tax integration ensures that the total tax paid by a corporation and its shareholder is roughly equal to the tax paid if the income was earned personally, preventing double taxation while allowing for strategic timing advantages.

Strategic Salary vs. Dividend Mix

Choosing how to pay yourself requires a delicate balance between immediate cash flow and long-term security. A common strategy involves paying a salary high enough to maximize your RRSP contribution limit, which is $33,810 for 2026. This approach requires paying into the Canada Pension Plan (CPP), which builds a guaranteed retirement base but increases current expenses. Alternatively, you might take the remaining required income as dividends to avoid excess CPP contributions and manage your personal tax brackets more effectively. Our team at Tax Partners can help you model these compensation scenarios to find the precise mix that supports your lifestyle and your future. A specialized CPA for medical professionals ensures these decisions are made with foresight, keeping your effective tax rate as low as possible.

Cross-Border Tax Challenges for Doctors and Specialists

The path of a medical career often crosses international borders, whether through residency in the US on a J-1 visa or pursuing a fellowship under an H-1B status. While these opportunities advance your clinical expertise, they create a complex web of tax obligations that a standard accountant might struggle to untangle. If you are a US citizen practicing in Canada, or a Canadian specialist with US-based income, your filing requirements don't stop at the border. A specialized CPA for medical professionals is essential to navigate the interaction between the IRS and the CRA, ensuring you remain compliant in both jurisdictions without paying more than your fair share.

The US-Canada Tax Treaty serves as your primary defence against double taxation, allowing you to claim foreign tax credits for professional fees earned. However, for US citizens owning a Canadian professional corporation, the rules are particularly treacherous. Your corporation may be classified as a Controlled Foreign Corporation (CFC), potentially triggering complex US tax implications under Subpart F or GILTI rules. Additionally, certain corporate investments, like Canadian mutual funds, can be labelled as Passive Foreign Investment Companies (PFICs) by the IRS. This classification leads to punitive tax rates and arduous reporting requirements that can quickly erode your investment gains if not managed with foresight.

FBAR and FATCA Compliance for Medical Professionals

Compliance is a matter of precision, not just paperwork. If you are a US person, you must file a Report of Foreign Bank and Financial Accounts (FBAR) if the aggregate value of your foreign accounts, including your corporate practice accounts, exceeds $10,000 USD at any point during the year. FATCA reporting on Form 8938 carries even higher stakes for dual citizens with significant assets. For 2026, the FBAR filing deadline is April 15, with an automatic extension to October 15. The penalties for non-compliance are severe, often starting at $10,000 USD per violation, making it vital to have a steady hand at the helm of your cross-border strategy.

Managing US Source Income from Research or Speaking

Specialists are frequently sought after for their expertise, receiving honorariums or consulting fees from US-based pharmaceutical or medical device companies. To receive these payments without a 30% automatic withholding, you typically need an Individual Taxpayer Identification Number (ITIN). We assist you in obtaining this number and ensure that any US source income is reported correctly on both your T1 and your 1040. By optimizing your foreign tax credits, a CPA for medical professionals ensures that your global contributions to medicine don't result in a global tax headache. This proactive approach allows you to focus on your research and speaking engagements while we secure your financial interests.

Advanced Wealth Preservation: Beyond the Corporation

Establishing a professional corporation is only the first step in a lifelong financial journey. As your practice matures, the focus shifts from simple tax deferral to sophisticated wealth preservation. An expert CPA for medical professionals looks past the current tax year to see the horizon of your career, identifying vehicles that offer superior growth and protection compared to standard retail investment products. Transitioning from a high-earning associate to a practice owner requires a shift in mindset, where you begin to view your corporation as a multi-generational wealth engine rather than just a repository for billings.

High-earning specialists often find that traditional tools like RRSPs aren't enough to support their desired retirement lifestyle. For these individuals, a Retirement Compensation Arrangement (RCA) can act as a powerful supplement, allowing the corporation to set aside significant funds for future use. Additionally, permanent life insurance held within the corporation serves a dual purpose. It provides a tax-free death benefit to your heirs through the Capital Account and offers a stable, tax-sheltered environment for corporate surplus. When balanced with a strategic approach to debt, such as weighing the low interest on medical school loans against the higher potential returns of corporate investing, these advanced tools create a fortress around your financial future.

The Individual Pension Plan (IPP) Advantage

For incorporated physicians over the age of 40, an Individual Pension Plan (IPP) often serves as a superior alternative to an RRSP. While the 2026 RRSP contribution limit is capped at $33,810, an IPP allows for significantly higher annual contributions that increase as you age. These contributions are fully tax-deductible for your corporation, effectively lowering your active business income and helping you stay below the passive income thresholds that trigger tax "grind-downs." Beyond the tax benefits, an IPP is a formal pension structure, offering a level of creditor protection that personal investment accounts simply cannot match. It's a steady, predictable way to realize your retirement goals while maximizing corporate tax efficiency.

Succession and Exit Planning for Private Practices

Preparing your practice for an eventual sale or transition requires years of foresight. Whether you're moving toward a family holding company or selling to a group of associates, understanding your clinic's valuation is vital. We look at more than just patient lists, analyzing your EBITDA and operational efficiency to ensure you receive full value for your life's work. A key component of this exit strategy is the Lifetime Capital Gains Exemption (LCGE), which in 2026 remains over $1 million for qualified small business corporation shares. Proper structuring today ensures you can claim this exemption when you're ready to step away. Our specialists at Tax Partners can design a custom wealth preservation strategy that protects your hard-earned assets and secures your legacy. A dedicated CPA for medical professionals ensures that your transition from active practice is as rewarding as the years you spent building it.

The Tax Partners Approach: 40 Years of Medical CPA Expertise

For four decades, Tax Partners has operated as a dedicated financial guardian for the Canadian medical community. While our experience spans over 20 diverse industries, we have cultivated a deep, specialized focus on the unique challenges facing healthcare providers. Choosing a CPA for medical professionals shouldn't feel like hiring a distant institution; it should feel like gaining a seasoned mentor who is genuinely invested in your success. Our 'Guardian' model of service is built on this proactive philosophy. We don't simply react to tax deadlines or CRA inquiries. Instead, we look ahead to identify potential risks and opportunities, ensuring your practice remains compliant and optimized at every turn.

One of our most distinct advantages is the integration of US and Canadian tax expertise under a single roof. As we explored in the previous sections regarding cross-border complexities, having a unified team prevents the communication gaps that often lead to double taxation or missed disclosures. This seamless coordination provides a level of precision and foresight that generalist firms simply cannot match. We understand that your time is your most valuable asset, and our goal is to protect it with the same rigour that we apply to your wealth.

A Seamless Transition for New Associates and Partners

Whether you are just starting your residency or joining a private clinic as a partner, the administrative burden of setting up your professional life can be daunting. We handle the heavy lifting, from the initial incorporation of your practice to the complexities of CRA registration. Our approach is defined by clarity; we employ a 'no-jargon' policy to ensure you fully understand your tax optimizations without feeling overwhelmed by technical terminology. This commitment to transparency and support is reflected in the 1,390+ five-star reviews we have received from fellow professionals who trust us to manage their corporate records and financial roadmaps. We make the transition into practice ownership smooth, allowing you to focus on your clinical responsibilities from day one.

Book Your Consultation Today

Your corporate structure should evolve alongside your career. We invite you to join us for a personalized strategy session to review your current setup and identify areas where you can further minimize tax liabilities and protect your assets. Our focus is simple: we want you to keep more of what you earn through meticulous, precision planning. By aligning your clinical goals with a robust financial strategy, you can secure a future that is as stable as it is rewarding. Take the first step toward total financial control and secure your financial future with a specialized medical CPA from Tax Partners. Let us provide the steady hand at the helm while you focus on what matters most: the health of your patients.

Secure Your Financial Legacy Today

Your career in medicine is dedicated to the care of others, but your own financial well-being deserves the same level of specialized attention. We have explored how strategic incorporation and advanced wealth preservation tools like IPPs can fundamentally shift your wealth trajectory. Navigating cross-border compliance and maximizing corporate tax deferrals are not just administrative tasks; they are the building blocks of your long-term security. Choosing a dedicated CPA for medical professionals ensures that every financial decision is made with the foresight required to protect your hard-earned assets.

At Tax Partners, we bring over 40 years of experience in Canadian and US tax law to your practice. With more than 495,000 returns filed and over $87M in client savings, our specialized expertise in healthcare professional accounting and incorporation is designed to help you thrive. Don't leave your financial future to chance. Request a tailored tax strategy session for medical professionals to review your corporate structure and start your journey toward total financial clarity. We look forward to being the steady hand that helps you build a prosperous and lasting legacy.

Frequently Asked Questions

Can a medical professional corporation (MPC) pay dividends to family members?

An MPC can pay dividends to family members, but it's now strictly governed by the Tax on Split Income (TOSI) rules. Unless your family member is actively engaged in the practice for at least 20 hours per week or meets specific age and share ownership criteria, these dividends will be taxed at the highest marginal rate. It's vital to consult a CPA for medical professionals to ensure your distribution strategy doesn't inadvertently trigger these punitive taxes.

How does the CRA define "passive income" for incorporated doctors?

The CRA defines passive income as earnings from investments that aren't directly related to your active medical services. This includes interest from savings, corporate dividends, rental income, and capital gains. If your corporation's passive income exceeds $50,000 in a year, the CRA begins to reduce your Small Business Deduction. At $150,000 of passive income, the deduction is eliminated entirely, which can increase your corporate tax bill by tens of thousands of dollars.

Is an Individual Pension Plan (IPP) better than an RRSP for a physician?

An Individual Pension Plan (IPP) is often superior to an RRSP for physicians over age 40 who earn a consistent salary. Unlike an RRSP, an IPP allows for higher contribution limits that increase as you age, and all contributions are fully deductible for your corporation. Additionally, an IPP provides robust creditor protection and allows for "past service" contributions. This can provide a significant one-time tax deduction for your practice that a standard RRSP cannot match.

Do I need a US CPA if I am a Canadian doctor with US medical school debt?

You don't strictly need a US CPA just to manage medical school debt, but it's highly recommended if you have US citizenship or earn US-based income. The interaction between Canadian tax credits and US interest deductions is incredibly complex. A cross-border specialist ensures that your debt repayment strategy aligns with both IRS and CRA regulations. This prevents missed opportunities to optimize your global tax position while you're paying down significant student loans from your residency years.

What medical expenses can I actually deduct through my corporation?

You can deduct any expense incurred to earn professional income. This includes malpractice insurance, professional dues, licensing fees, and office overhead like rent and staff salaries. Additionally, travel for continuing medical education, specialized equipment, and home office expenses are deductible if they meet specific CRA criteria. Proper documentation is the key to ensuring these deductions stand up to scrutiny during a routine audit of your professional corporation, keeping your corporate records clean and defensible.

How often should a medical professional review their corporate tax strategy?

You should review your corporate tax strategy at least once a year, typically well before your fiscal year-end. However, significant life events like buying a home, marriage, or a major increase in billing should trigger an immediate consultation. Regular reviews with a CPA for medical professionals allow you to adjust your salary-dividend mix and investment strategies in response to evolving tax laws. This proactive approach ensures you never miss a chance to defer taxes or protect your assets.

What is the Lifetime Capital Gains Exemption (LCGE) for medical practices?

The Lifetime Capital Gains Exemption (LCGE) allows you to realize a tax-free gain on the sale of qualified small business corporation shares. For 2026, this exemption is valued at over $1 million. To qualify, your medical practice must meet specific asset tests, including the requirement that 90% of the corporation's assets were used in active business at the time of the sale. This makes long-term planning for passive income vital if you intend to sell your clinic one day.

Can I use my medical corporation to buy real estate?

Yes, you can use your medical corporation to purchase real estate, but the strategy must be carefully managed to avoid tax pitfalls. Buying your clinic space can be a wise move, as the rent paid to yourself remains within your corporate structure. However, using corporate funds for residential or recreational property triggers "shareholder benefit" rules and contributes to your passive income threshold. This can lead to double taxation if the property isn't handled as a legitimate business investment.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

The Complexity of Medical Billing and GST/HST

Healthcare billing is rarely straightforward. Most medical services are exempt from GST/HST, but many modern practices offer taxable supplies like cosmetic procedures, administrative fees, or certain medical reports. If your bookkeeping doesn't synchronize perfectly with your provincial billing cycles, you're likely missing out on Input Tax Credits (ITCs). These credits allow you to recover the GST/HST paid on expenses related to your taxable activities. For travelling specialists, "place of supply" rules become vital. If you provide services across provincial borders, the tax rates and reporting requirements change. Precision in these areas is non-negotiable for maintaining clean corporate records.

The High-Income Trap: Moving Beyond Basic Tax Filing

High-earning physicians are frequently flagged for CRA audits, especially regarding the blurred lines between personal and business expenses. Whether it's a home office claim or travel for a conference, a specialized CPA for medical professionals ensures every deduction is defensible and documented. This reduces the stress of potential scrutiny and keeps your focus on patient care. Perhaps the most dangerous pitfall is the passive income threshold. Once your corporation's passive investment income exceeds $50,000, your Small Business Deduction begins to decrease. At $150,000, it's eliminated entirely. This "grind-down" can increase your corporate tax bill significantly if not managed with foresight. A generalist might only notice this after the year-end, whereas a specialist monitors these levels throughout the year. Ultimately, the right advisor protects your time as much as your money. You shouldn't be reconciling spreadsheets after a twelve-hour shift; you should be resting or with your family while your financial guardian handles the details. Incorporating your practice isn't just a legal formality; it's a strategic move that fundamentally changes your wealth trajectory. A Medical Professional Corporation (MPC) allows you to separate your personal finances from your practice's active business income. This separation is crucial because the tax rates applied to corporations are significantly lower than those for high-earning individuals. In 2026, the Ontario combined small business tax rate sits at just 12.2% on the first $500,000 of active income. Compare this to the top federal personal tax bracket of 33% for income over $258,482, and the advantage becomes clear. By working with a specialized CPA for medical professionals, you can ensure your MPC is structured to capture these savings while protecting your personal assets from general commercial liabilities. While an MPC offers robust protection for business debts or lease obligations, it doesn't shield you from professional malpractice claims. However, the ability to retain earnings within the company provides a financial buffer that sole proprietors lack. The Small Business Deduction alone can save an Ontario medical practice up to $85,000 in taxes annually. These are funds that can be used to pay down practice-related debt or expand your clinic's capabilities. Navigating the strict Tax on Split Income (TOSI) rules is also essential, as the CRA continues to rigorously limit the ability to sprinkle income to family members who aren't actively involved in the business.

Tax Deferral: Your Most Powerful Wealth-Building Tool

Tax deferral remains the primary engine for growth within an MPC. When you earn income personally, you pay tax at your marginal rate before you can invest the remainder. Inside a corporation, you only pay the low corporate rate, leaving significantly more capital available to grow. This can result in tax savings of approximately 30% to 40% annually compared to a sole proprietorship. Tax integration ensures that the total tax paid by a corporation and its shareholder is roughly equal to the tax paid if the income was earned personally, preventing double taxation while allowing for strategic timing advantages.

Strategic Salary vs. Dividend Mix

Choosing how to pay yourself requires a delicate balance between immediate cash flow and long-term security. A common strategy involves paying a salary high enough to maximize your RRSP contribution limit, which is $33,810 for 2026. This approach requires paying into the Canada Pension Plan (CPP), which builds a guaranteed retirement base but increases current expenses. Alternatively, you might take the remaining required income as dividends to avoid excess CPP contributions and manage your personal tax brackets more effectively. Our team at Tax Partners can help you model these compensation scenarios to find the precise mix that supports your lifestyle and your future. A specialized CPA for medical professionals ensures these decisions are made with foresight, keeping your effective tax rate as low as possible. The path of a medical career often crosses international borders, whether through residency in the US on a J-1 visa or pursuing a fellowship under an H-1B status. While these opportunities advance your clinical expertise, they create a complex web of tax obligations that a standard accountant might struggle to untangle. If you are a US citizen practicing in Canada, or a Canadian specialist with US-based income, your filing requirements don't stop at the border. A specialized CPA for medical professionals is essential to navigate the interaction between the IRS and the CRA, ensuring you remain compliant in both jurisdictions without paying more than your fair share. The US-Canada Tax Treaty serves as your primary defence against double taxation, allowing you to claim foreign tax credits for professional fees earned. However, for US citizens owning a Canadian professional corporation, the rules are particularly treacherous. Your corporation may be classified as a Controlled Foreign Corporation (CFC), potentially triggering complex US tax implications under Subpart F or GILTI rules. Additionally, certain corporate investments, like Canadian mutual funds, can be labelled as Passive Foreign Investment Companies (PFICs) by the IRS. This classification leads to punitive tax rates and arduous reporting requirements that can quickly erode your investment gains if not managed with foresight.

FBAR and FATCA Compliance for Medical Professionals

Compliance is a matter of precision, not just paperwork. If you are a US person, you must file a Report of Foreign Bank and Financial Accounts (FBAR) if the aggregate value of your foreign accounts, including your corporate practice accounts, exceeds $10,000 USD at any point during the year. FATCA reporting on Form 8938 carries even higher stakes for dual citizens with significant assets. For 2026, the FBAR filing deadline is April 15, with an automatic extension to October 15. The penalties for non-compliance are severe, often starting at $10,000 USD per violation, making it vital to have a steady hand at the helm of your cross-border strategy.

Managing US Source Income from Research or Speaking

Specialists are frequently sought after for their expertise, receiving honorariums or consulting fees from US-based pharmaceutical or medical device companies. To receive these payments without a 30% automatic withholding, you typically need an Individual Taxpayer Identification Number (ITIN). We assist you in obtaining this number and ensure that any US source income is reported correctly on both your T1 and your 1040. By optimizing your foreign tax credits, a CPA for medical professionals ensures that your global contributions to medicine don't result in a global tax headache. This proactive approach allows you to focus on your research and speaking engagements while we secure your financial interests. Establishing a professional corporation is only the first step in a lifelong financial journey. As your practice matures, the focus shifts from simple tax deferral to sophisticated wealth preservation. An expert CPA for medical professionals looks past the current tax year to see the horizon of your career, identifying vehicles that offer superior growth and protection compared to standard retail investment products. Transitioning from a high-earning associate to a practice owner requires a shift in mindset, where you begin to view your corporation as a multi-generational wealth engine rather than just a repository for billings. High-earning specialists often find that traditional tools like RRSPs aren't enough to support their desired retirement lifestyle. For these individuals, a Retirement Compensation Arrangement (RCA) can act as a powerful supplement, allowing the corporation to set aside significant funds for future use. Additionally, permanent life insurance held within the corporation serves a dual purpose. It provides a tax-free death benefit to your heirs through the Capital Account and offers a stable, tax-sheltered environment for corporate surplus. When balanced with a strategic approach to debt, such as weighing the low interest on medical school loans against the higher potential returns of corporate investing, these advanced tools create a fortress around your financial future.

The Individual Pension Plan (IPP) Advantage

For incorporated physicians over the age of 40, an Individual Pension Plan (IPP) often serves as a superior alternative to an RRSP. While the 2026 RRSP contribution limit is capped at $33,810, an IPP allows for significantly higher annual contributions that increase as you age. These contributions are fully tax-deductible for your corporation, effectively lowering your active business income and helping you stay below the passive income thresholds that trigger tax "grind-downs." Beyond the tax benefits, an IPP is a formal pension structure, offering a level of creditor protection that personal investment accounts simply cannot match. It's a steady, predictable way to realize your retirement goals while maximizing corporate tax efficiency.

Succession and Exit Planning for Private Practices

Preparing your practice for an eventual sale or transition requires years of foresight. Whether you're moving toward a family holding company or selling to a group of associates, understanding your clinic's valuation is vital. We look at more than just patient lists, analyzing your EBITDA and operational efficiency to ensure you receive full value for your life's work. A key component of this exit strategy is the Lifetime Capital Gains Exemption (LCGE), which in 2026 remains over $1 million for qualified small business corporation shares. Proper structuring today ensures you can claim this exemption when you're ready to step away. Our specialists at Tax Partners can design a custom wealth preservation strategy that protects your hard-earned assets and secures your legacy. A dedicated CPA for medical professionals ensures that your transition from active practice is as rewarding as the years you spent building it. For four decades, Tax Partners has operated as a dedicated financial guardian for the Canadian medical community. While our experience spans over 20 diverse industries, we have cultivated a deep, specialized focus on the unique challenges facing healthcare providers. Choosing a CPA for medical professionals shouldn't feel like hiring a distant institution; it should feel like gaining a seasoned mentor who is genuinely invested in your success. Our 'Guardian' model of service is built on this proactive philosophy. We don't simply react to tax deadlines or CRA inquiries. Instead, we look ahead to identify potential risks and opportunities, ensuring your practice remains compliant and optimized at every turn. One of our most distinct advantages is the integration of US and Canadian tax expertise under a single roof. As we explored in the previous sections regarding cross-border complexities, having a unified team prevents the communication gaps that often lead to double taxation or missed disclosures. This seamless coordination provides a level of precision and foresight that generalist firms simply cannot match. We understand that your time is your most valuable asset, and our goal is to protect it with the same rigour that we apply to your wealth.

A Seamless Transition for New Associates and Partners

Whether you are just starting your residency or joining a private clinic as a partner, the administrative burden of setting up your professional life can be daunting. We handle the heavy lifting, from the initial incorporation of your practice to the complexities of CRA registration. Our approach is defined by clarity; we employ a 'no-jargon' policy to ensure you fully understand your tax optimizations without feeling overwhelmed by technical terminology. This commitment to transparency and support is reflected in the 1,390+ five-star reviews we have received from fellow professionals who trust us to manage their corporate records and financial roadmaps. We make the transition into practice ownership smooth, allowing you to focus on your clinical responsibilities from day one.

Book Your Consultation Today

Your corporate structure should evolve alongside your career. We invite you to join us for a personalized strategy session to review your current setup and identify areas where you can further minimize tax liabilities and protect your assets. Our focus is simple: we want you to keep more of what you earn through meticulous, precision planning. By aligning your clinical goals with a robust financial strategy, you can secure a future that is as stable as it is rewarding. Take the first step toward total financial control and secure your financial future with a specialized medical CPA from Tax Partners. Let us provide the steady hand at the helm while you focus on what matters most: the health of your patients. Your career in medicine is dedicated to the care of others, but your own financial well-being deserves the same level of specialized attention. We have explored how strategic incorporation and advanced wealth preservation tools like IPPs can fundamentally shift your wealth trajectory. Navigating cross-border compliance and maximizing corporate tax deferrals are not just administrative tasks; they are the building blocks of your long-term security. Choosing a dedicated CPA for medical professionals ensures that every financial decision is made with the foresight required to protect your hard-earned assets. At Tax Partners, we bring over 40 years of experience in Canadian and US tax law to your practice. With more than 495,000 returns filed and over $87M in client savings, our specialized expertise in healthcare professional accounting and incorporation is designed to help you thrive. Don't leave your financial future to chance. Request a tailored tax strategy session for medical professionals to review your corporate structure and start your journey toward total financial clarity. We look forward to being the steady hand that helps you build a prosperous and lasting legacy.

Can a medical professional corporation (MPC) pay dividends to family members?

An MPC can pay dividends to family members, but it's now strictly governed by the Tax on Split Income (TOSI) rules. Unless your family member is actively engaged in the practice for at least 20 hours per week or meets specific age and share ownership criteria, these dividends will be taxed at the highest marginal rate. It's vital to consult a CPA for medical professionals to ensure your distribution strategy doesn't inadvertently trigger these punitive taxes.

How does the CRA define "passive income" for incorporated doctors?

The CRA defines passive income as earnings from investments that aren't directly related to your active medical services. This includes interest from savings, corporate dividends, rental income, and capital gains. If your corporation's passive income exceeds $50,000 in a year, the CRA begins to reduce your Small Business Deduction. At $150,000 of passive income, the deduction is eliminated entirely, which can increase your corporate tax bill by tens of thousands of dollars.

Is an Individual Pension Plan (IPP) better than an RRSP for a physician?

An Individual Pension Plan (IPP) is often superior to an RRSP for physicians over age 40 who earn a consistent salary. Unlike an RRSP, an IPP allows for higher contribution limits that increase as you age, and all contributions are fully deductible for your corporation. Additionally, an IPP provides robust creditor protection and allows for "past service" contributions. This can provide a significant one-time tax deduction for your practice that a standard RRSP cannot match.

Do I need a US CPA if I am a Canadian doctor with US medical school debt?

You don't strictly need a US CPA just to manage medical school debt, but it's highly recommended if you have US citizenship or earn US-based income. The interaction between Canadian tax credits and US interest deductions is incredibly complex. A cross-border specialist ensures that your debt repayment strategy aligns with both IRS and CRA regulations. This prevents missed opportunities to optimize your global tax position while you're paying down significant student loans from your residency years.

What medical expenses can I actually deduct through my corporation?

You can deduct any expense incurred to earn professional income. This includes malpractice insurance, professional dues, licensing fees, and office overhead like rent and staff salaries. Additionally, travel for continuing medical education, specialized equipment, and home office expenses are deductible if they meet specific CRA criteria. Proper documentation is the key to ensuring these deductions stand up to scrutiny during a routine audit of your professional corporation, keeping your corporate records clean and defensible.

How often should a medical professional review their corporate tax strategy?

You should review your corporate tax strategy at least once a year, typically well before your fiscal year-end. However, significant life events like buying a home, marriage, or a major increase in billing should trigger an immediate consultation. Regular reviews with a CPA for medical professionals allow you to adjust your salary-dividend mix and investment strategies in response to evolving tax laws. This proactive approach ensures you never miss a chance to defer taxes or protect your assets.

What is the Lifetime Capital Gains Exemption (LCGE) for medical practices?

The Lifetime Capital Gains Exemption (LCGE) allows you to realize a tax-free gain on the sale of qualified small business corporation shares. For 2026, this exemption is valued at over $1 million. To qualify, your medical practice must meet specific asset tests, including the requirement that 90% of the corporation's assets were used in active business at the time of the sale. This makes long-term planning for passive income vital if you intend to sell your clinic one day.

Can I use my medical corporation to buy real estate?

Yes, you can use your medical corporation to purchase real estate, but the strategy must be carefully managed to avoid tax pitfalls. Buying your clinic space can be a wise move, as the rent paid to yourself remains within your corporate structure. However, using corporate funds for residential or recreational property triggers "shareholder benefit" rules and contributes to your passive income threshold. This can lead to double taxation if the property isn't handled as a legitimate business investment.