The Comprehensive Guide to Canadian Corporate Tax Compliance in 2026

Most business owners view a CRA tax notice as a burden to be endured, but what if your filing process was actually your most powerful tool for long-term financial growth? It's a common sentiment to feel overwhelmed by the sheer volume of paperwork and the persistent fear of a surprise audit. We recognize the pressure of tracking multiple filing deadlines while attempting to integrate complex international operations. Managing Canadian corporate tax compliance often feels like a high-stakes balancing act that peaks with a stressful year-end preparation.

You deserve a more stable path forward. This guide empowers you to master the complexities of CRA regulations and demonstrates how to transform tax compliance into a strategic advantage for your Canadian business. By the end of this article, you'll understand the essential 2026 federal and provincial rates, learn how to organize your financial records for maximum efficiency, and discover how proactive planning can significantly reduce your tax liability. We'll provide a clear roadmap to help you move from a state of uncertainty toward total control over your regulatory standing.

Key Takeaways

- Recognize your obligation as a resident corporation to report worldwide income to the CRA, ensuring full adherence to the Income Tax Act.

- Distinguish between your T2 return filing deadline and your balance due date to effectively manage cash flow and avoid interest charges.

- Shift toward a continuous compliance mindset that uses technology to create a transparent, audit-ready record for your business.

- Master Canadian corporate tax compliance by accurately managing high-frequency touchpoints like payroll and employee taxable benefits.

- Learn how integrating corporate tax planning with your personal estate goals can protect your financial legacy and long-term stability.

Navigating the Landscape of Canadian Corporate Tax Compliance in 2026

Adherence to the Canadian corporate tax system involves much more than just annual filings. It represents a rigorous commitment to the Income Tax Act and the specific regulations set by the Canada Revenue Agency (CRA). In 2026, precision is paramount. The CRA is increasingly utilizing advanced data analytics and AI-driven tools to identify discrepancies, which means even minor errors can trigger unwanted scrutiny. Maintaining high standards for Canadian corporate tax compliance is no longer a seasonal task; it is a fundamental pillar of a healthy, resilient business.

The role of a professional accountant has evolved alongside these technological shifts. Rather than simply reacting to deadlines, a seasoned CPA acts as a proactive mentor, helping you anticipate regulatory changes before they impact your bottom line. This partnership provides a steady hand at the helm, ensuring your records remain transparent and your business stays on the right side of evolving CRA expectations.

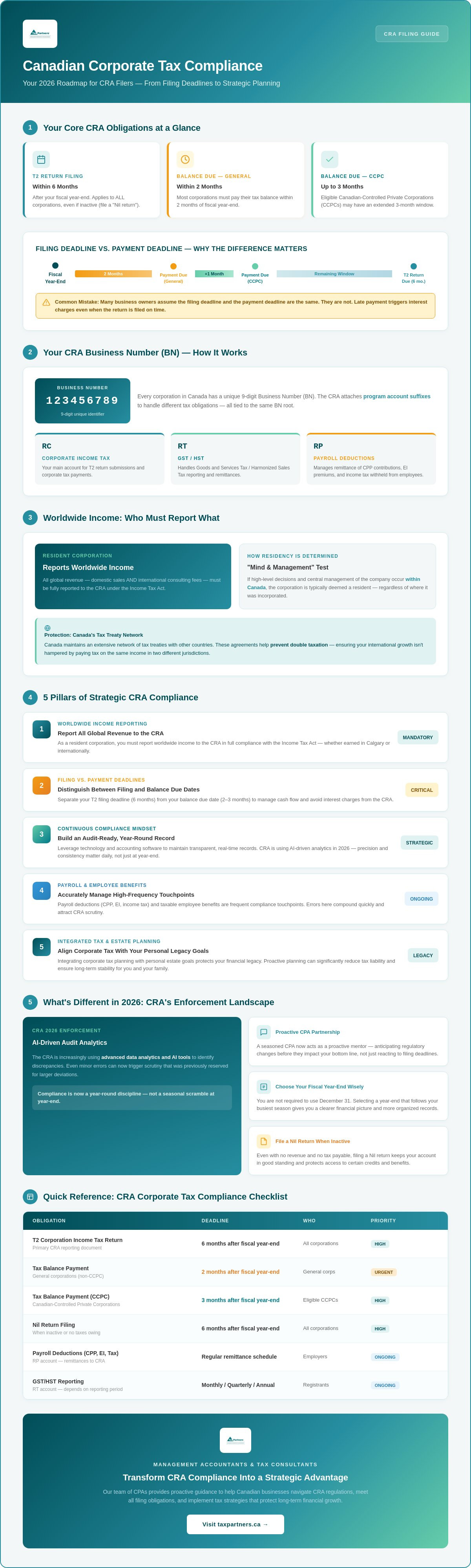

The Business Number and Program Accounts

Every corporation in Canada requires a 9-digit Business Number (BN). Think of this as your entity’s unique fingerprint for all interactions with the federal government. While the base nine digits identify your business, the CRA attaches specific suffixes to create program accounts for different tax obligations. For example, your corporate income tax account uses the "RC" identifier, while "RT" is reserved for GST/HST and "RP" handles payroll deductions. The Business Number serves as the foundational identifier for all federal and provincial tax interactions.

Understanding Worldwide Income Obligations

For CRA filers, the scope of taxation is remarkably broad. If your company is considered a resident corporation, you are responsible for reporting and paying tax on worldwide income. This rule applies to Canadian-controlled private corporations (CCPCs) regardless of where the revenue was originally generated. Whether you are earning domestic sales in Calgary or international consulting fees from abroad, the CRA expects a full accounting of those global earnings.

Determining residency isn't always as simple as looking at where you incorporated. The CRA often applies the "mind and management" test to establish residency. If the high-level decisions and central management of the company occur within Canada, the corporation is typically deemed a resident for tax purposes. To protect businesses with international revenue streams, Canada maintains an extensive network of tax treaties. These agreements are essential tools for preventing double taxation, ensuring that your international growth isn't hampered by paying tax on the same income in two different jurisdictions.

The Essential Filing Requirements for Canadian Private Corporations

Meeting the requirements for Canadian corporate tax compliance involves a disciplined approach to timing. Many entrepreneurs assume that the date they file their paperwork is the same date they must pay their taxes. This is a costly misconception. While the Canada Revenue Agency (CRA) allows a generous window for filing, the deadline for settling your balance is significantly tighter. Precision in these early stages prevents unnecessary interest charges and sets a professional tone for your relationship with the tax authorities.

Even if your corporation is currently inactive or has no taxes payable, you must still file what is known as a "Nil return." This keeps your account in good standing and ensures you don't lose access to certain credits or benefits. Selecting an appropriate fiscal year-end is equally critical. You aren't tethered to the calendar year; choosing a date that follows your busiest season allows for a clearer financial picture and more organized record-keeping. If you find these choices daunting, engaging with professional Canadian tax services can provide the clarity needed to align your tax cycle with your business goals.

The T2 Corporate Income Tax Return

For CRA filers, the T2 Corporation Income Tax Return is the primary reporting document. It must be submitted within six months of your fiscal year-end. However, the deadline to pay your tax balance is much earlier. Most corporations must pay within two months, though eligible Canadian-controlled private corporations (CCPCs) may have up to three months. A central component of this package is Schedule 1. This schedule is used to reconcile your accounting income with your taxable income, adjusting for items like depreciation that are treated differently under the Income Tax Act.

GST/HST and Provincial Sales Tax Obligations

Registration for GST/HST is mandatory once your business earns more than $30,000 in taxable supplies over four consecutive calendar quarters. Many businesses choose to register voluntarily before reaching this limit. This allows you to claim Input Tax Credits (ITCs), which let you recover the GST/HST paid on business expenses like rent, equipment, and professional fees. Be mindful of provincial variations. While many provinces use the Harmonized Sales Tax (HST), others like British Columbia, Saskatchewan, and Manitoba require separate Provincial Sales Tax (PST) or Retail Sales Tax (RST) filings. Quebec operates its own system, the Quebec Sales Tax (QST), which requires a distinct approach for those with a permanent establishment in that province.

Beyond the Basics: Strategic Compliance for Modern SMEs

While the annual T2 filing is a major milestone, Canadian corporate tax compliance is truly won or lost in the day-to-day operations of your business. Every payroll run and every cross-border sale carries its own set of regulatory obligations. Precision in these smaller, high-frequency tasks ensures that your year-end preparation remains a smooth, predictable process rather than a frantic scramble. High-quality bookkeeping serves as the essential fuel for this engine. Without accurate records, even the most sophisticated tax strategy will falter under CRA scrutiny. We view compliance not as a static requirement, but as a dynamic process that reflects the health and integrity of your entire operation.

Managing Payroll and Taxable Benefits

Payroll management is one of the most frequent touchpoints with the CRA. It involves much more than just issuing cheques; it requires the diligent collection and remittance of Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and federal income tax withholdings. For CRA filers, accuracy is vital when reporting taxable benefits. These are non-cash perks, such as the personal use of a company vehicle or employer-paid health premiums, that must be added to an employee's income. Miscalculating these leads to incorrect T4 and T4A slips, which can trigger audits for both the corporation and the individual team members. You can find more details on these specific requirements through Official Canadian Tax Information. Ensuring these slips align with personal tax filings is a hallmark of an organized and respectful employer.

The Impact of US and Cross-Border Operations

Expanding your reach into the United States is an exciting milestone, but it introduces a new layer of complexity for Canadian businesses. Under US tax rules, even if you don't have a physical office south of the border, your activities might meet the "Permanent Establishment" threshold. This triggers the need to file Form 1120-F with the IRS. Fortunately, the US-Canada Tax Treaty exists to protect Canadian SMEs from redundant taxation, allowing you to claim relief on income that would otherwise be taxed in both countries. For owners with dual interests, compliance may also extend to specialized ITIN (Individual Taxpayer Identification Number) applications or FBAR (Foreign Bank and Financial Accounts) reporting. Navigating these waters requires a proactive guardian who understands the nuances of both jurisdictions to ensure your international growth isn't hampered by avoidable penalties.

Establishing an Audit-Ready Framework for Your Business

Viewing tax season as a single, stressful event in the calendar is a risk most businesses can't afford to take. True security comes from a "continuous compliance" mindset, where every transaction is recorded with the expectation that it may one day be reviewed. Maintaining a high standard of Canadian corporate tax compliance requires a shift in perspective. It's about building a transparent, verifiable audit trail that exists long before the CRA sends a notice of assessment. When your records are organized and accessible, the fear of an audit transforms into the confidence of being prepared.

Proactive planning reduces the likelihood of "red flags" that often trigger CRA reviews, such as inconsistent profit margins or unusual expense claims. By documenting the business purpose of every significant transaction as it happens, you create a narrative that is difficult to challenge later. If you are ready to move beyond the year-end scramble, our team provides the Canadian accounting and tax services you need to build a resilient, audit-proof business.

Digital Record-Keeping and Data Integrity

The CRA has clear expectations for record-keeping, and in 2026, those expectations are increasingly digital. To meet these standards, follow these three essential steps:

- Step 1: Implement cloud-based accounting software to centralize all financial transactions. This ensures your data is accessible to your professional advisors in real time.

- Step 2: Use digital receipt capture tools to link source documents directly to ledger entries. This eliminates the "shoebox" method and provides an immediate link between a deduction and its proof of purchase.

- Step 3: Ensure all records are backed up and maintained for the mandatory six-year period required for CRA filers. This applies to both digital and physical documents.

Proactive Tax Planning vs. Year-End Scrambling

Reactive filing is simply recording history. Proactive planning is about writing it. While a reactive approach focuses on what already happened, a proactive strategy allows you to shape the financial outcome. We recommend quarterly reviews to estimate your tax liabilities. This practice allows you to adjust your instalments and avoid the shock of a large balance due at the end of the year. Furthermore, it provides the opportunity to optimize the owner’s total tax position through strategic remuneration. Deciding between a salary or dividends isn't a one-time choice; it's a dynamic decision that should reflect your current cash flow needs and long-term wealth goals. This foresight ensures you aren't just meeting requirements, but actively securing a better outcome for your business legacy.

Securing Your Business Legacy Through Expert Tax Partnership

Achieving a high standard of Canadian corporate tax compliance is not merely a box-ticking exercise; it's the first essential step toward comprehensive wealth preservation. For over 40 years, we've served as a steady hand for Canadian business owners, guiding them through shifting regulatory tides with institutional wisdom and a modern, forward-thinking outlook. Your business is more than just an entity. It represents your life's work and the foundation of your family’s future legacy. We believe that a proactive guardian doesn't just react to current requirements but actively looks ahead to secure a better outcome for the years to come.

Stability and ethical steadfastness form the core of a successful long-term partnership. When you move beyond the stress of annual filings, you gain the clarity needed to make bold, informed decisions about your company's future. Our rhythmic approach to financial management ensures that you're never rushed or caught off guard by new CRA expectations. Instead, you're led on a guided journey from potential uncertainty toward a state of total control and understanding.

Why Boutique Expertise Surpasses Generalist Solutions

Large, distant institutions often lack the personalized touch required to understand the nuances of your specific industry. Our boutique firm provides "Big Four" level expertise while maintaining the warm, direct relationship you expect from a dedicated partner. Whether you operate in healthcare, real estate, or specialized emerging sectors, deep industry knowledge leads to superior tax outcomes. You'll work directly with senior partners who understand your business history, allowing us to identify risks and opportunities that a generalist might overlook. This bespoke approach ensures that your tax strategy is as unique as your business itself, providing a level of precision that generalist firms simply cannot match.

Integrating Wealth Management with Corporate Compliance

A corporation that maintains impeccable records is a far more effective vehicle for long-term wealth accumulation. When your Canadian corporate tax compliance is beyond reproach, you're in a much stronger position to integrate corporate earnings with personal estate and succession planning. This alignment is vital when considering the eventual sale or transition of your business. Buyers and successors look for a clean history of transparency and reliability. By treating compliance as a strategic asset, you ensure that your business remains a valuable, transferable legacy. Our goal is to move you quickly from the problems of the present to a permanent sense of resolution. To take the next step in your financial journey, Partner with Tax Partners to realize your business’s full financial potential.

Empower Your Financial Future

Mastering the landscape of Canadian corporate tax compliance is more than a regulatory necessity; it's a strategic move that protects your business's integrity and value. By shifting from a reactive year-end scramble to a proactive, digital-first framework, you ensure that every transaction serves your long-term goals. We've explored how precise bookkeeping, strategic remuneration, and a continuous compliance mindset turn complex CRA requirements into a clear path for growth.

With over 40 years of Canadian and cross-border tax expertise, our team has filed more than 495,000 returns with unwavering precision. This dedication to excellence is reflected in more than 1,390 five-star reviews from business owners who trust us as their proactive guardians. Ready to transform your approach? Secure your business’s future with expert Canadian corporate tax services.

You don't have to navigate these complexities alone. With a steady hand at the helm, you can focus on what you do best while we ensure your business remains resilient and ready for whatever the future holds.

Frequently Asked Questions

What is the corporate tax filing deadline in Canada for 2026?

Under CRA rules, your T2 Corporation Income Tax Return is due within six months of your fiscal year-end. However, you must pay any balance owing much earlier. For most corporations, the payment deadline is two months after the year-end, though eligible CCPCs may have three months to settle their balance. Missing these dates leads to immediate interest charges on the outstanding amount.

Do I need to file a corporate tax return if my business made no money this year?

Yes, every resident corporation must file a T2 return for each taxation year, even if there is no tax payable or the business is inactive. These are often called "Nil returns." Filing ensures your account remains in good standing with the CRA and allows you to carry forward losses that could reduce your future tax liability when the business becomes profitable again.

How long must I keep my corporate tax records for the CRA?

You are required to maintain all financial records and supporting documents for a period of six years from the end of the last tax year to which they relate. This includes digital receipts, ledger entries, and bank statements. Keeping these records organized is a fundamental part of maintaining Canadian corporate tax compliance and ensures you are ready for any potential review or audit.

What is the difference between a CCPC and other types of corporations?

A Canadian-Controlled Private Corporation (CCPC) is a private company that is not controlled by non-resident persons or public corporations. These entities enjoy a lower federal tax rate of 9% on the first $500,000 of active business income. Other corporations, such as public or non-resident-controlled entities, are subject to the general federal tax rate, which is currently 15% after federal abatements and reductions.

Can I change my corporation’s fiscal year-end after it has been established?

Yes, you can request a change to your fiscal year-end, but it generally requires written approval from the CRA. You must provide a valid business reason for the change, such as aligning with a new parent company or a significant shift in your seasonal business cycle. Changes made solely for the purpose of minimizing taxes are typically not approved by the tax authorities.

What happens if I miss the deadline for paying my corporate tax balance?

Missing the payment deadline triggers immediate interest charges, which the CRA calculates at the prescribed interest rate plus 4%. If you also fail to file your return on time, you'll face a late-filing penalty of 5% of the balance owing, plus an additional 1% for each full month the return is late. These costs can escalate quickly, especially for repeated late filers who face even higher penalties.

Does my Canadian corporation need to file taxes in the US if I have American customers?

Having American customers doesn't automatically trigger a US tax filing, but having a "Permanent Establishment" south of the border usually does. Under IRS rules, you may be required to file Form 1120-F. It's essential to consult the US-Canada Tax Treaty to determine if your specific activities, such as having a physical office or employees in the US, create a formal filing obligation.

How can I reduce the risk of a CRA audit for my small business?

Reducing audit risk starts with maintaining high standards of Canadian corporate tax compliance through meticulous record-keeping and consistent reporting. Avoid "red flags" like large discrepancies between your GST/HST filings and reported income or unusual expense claims that don't align with industry norms. Engaging a professional CPA to review your returns before submission provides an added layer of scrutiny that identifies potential issues early.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

The Business Number and Program Accounts

Every corporation in Canada requires a 9-digit Business Number (BN). Think of this as your entity’s unique fingerprint for all interactions with the federal government. While the base nine digits identify your business, the CRA attaches specific suffixes to create program accounts for different tax obligations. For example, your corporate income tax account uses the "RC" identifier, while "RT" is reserved for GST/HST and "RP" handles payroll deductions. The Business Number serves as the foundational identifier for all federal and provincial tax interactions.

Understanding Worldwide Income Obligations

For CRA filers, the scope of taxation is remarkably broad. If your company is considered a resident corporation, you are responsible for reporting and paying tax on worldwide income. This rule applies to Canadian-controlled private corporations (CCPCs) regardless of where the revenue was originally generated. Whether you are earning domestic sales in Calgary or international consulting fees from abroad, the CRA expects a full accounting of those global earnings. Determining residency isn't always as simple as looking at where you incorporated. The CRA often applies the "mind and management" test to establish residency. If the high-level decisions and central management of the company occur within Canada, the corporation is typically deemed a resident for tax purposes. To protect businesses with international revenue streams, Canada maintains an extensive network of tax treaties. These agreements are essential tools for preventing double taxation, ensuring that your international growth isn't hampered by paying tax on the same income in two different jurisdictions. Meeting the requirements for Canadian corporate tax compliance involves a disciplined approach to timing. Many entrepreneurs assume that the date they file their paperwork is the same date they must pay their taxes. This is a costly misconception. While the Canada Revenue Agency (CRA) allows a generous window for filing, the deadline for settling your balance is significantly tighter. Precision in these early stages prevents unnecessary interest charges and sets a professional tone for your relationship with the tax authorities. Even if your corporation is currently inactive or has no taxes payable, you must still file what is known as a "Nil return." This keeps your account in good standing and ensures you don't lose access to certain credits or benefits. Selecting an appropriate fiscal year-end is equally critical. You aren't tethered to the calendar year; choosing a date that follows your busiest season allows for a clearer financial picture and more organized record-keeping. If you find these choices daunting, engaging with professional Canadian tax services can provide the clarity needed to align your tax cycle with your business goals.

The T2 Corporate Income Tax Return

For CRA filers, the T2 Corporation Income Tax Return is the primary reporting document. It must be submitted within six months of your fiscal year-end. However, the deadline to pay your tax balance is much earlier. Most corporations must pay within two months, though eligible Canadian-controlled private corporations (CCPCs) may have up to three months. A central component of this package is Schedule 1. This schedule is used to reconcile your accounting income with your taxable income, adjusting for items like depreciation that are treated differently under the Income Tax Act.

GST/HST and Provincial Sales Tax Obligations

Registration for GST/HST is mandatory once your business earns more than $30,000 in taxable supplies over four consecutive calendar quarters. Many businesses choose to register voluntarily before reaching this limit. This allows you to claim Input Tax Credits (ITCs), which let you recover the GST/HST paid on business expenses like rent, equipment, and professional fees. Be mindful of provincial variations. While many provinces use the Harmonized Sales Tax (HST), others like British Columbia, Saskatchewan, and Manitoba require separate Provincial Sales Tax (PST) or Retail Sales Tax (RST) filings. Quebec operates its own system, the Quebec Sales Tax (QST), which requires a distinct approach for those with a permanent establishment in that province. While the annual T2 filing is a major milestone, Canadian corporate tax compliance is truly won or lost in the day-to-day operations of your business. Every payroll run and every cross-border sale carries its own set of regulatory obligations. Precision in these smaller, high-frequency tasks ensures that your year-end preparation remains a smooth, predictable process rather than a frantic scramble. High-quality bookkeeping serves as the essential fuel for this engine. Without accurate records, even the most sophisticated tax strategy will falter under CRA scrutiny. We view compliance not as a static requirement, but as a dynamic process that reflects the health and integrity of your entire operation.

Managing Payroll and Taxable Benefits

Payroll management is one of the most frequent touchpoints with the CRA. It involves much more than just issuing cheques; it requires the diligent collection and remittance of Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and federal income tax withholdings. For CRA filers, accuracy is vital when reporting taxable benefits. These are non-cash perks, such as the personal use of a company vehicle or employer-paid health premiums, that must be added to an employee's income. Miscalculating these leads to incorrect T4 and T4A slips, which can trigger audits for both the corporation and the individual team members. You can find more details on these specific requirements through Official Canadian Tax Information. Ensuring these slips align with personal tax filings is a hallmark of an organized and respectful employer.

The Impact of US and Cross-Border Operations

Expanding your reach into the United States is an exciting milestone, but it introduces a new layer of complexity for Canadian businesses. Under US tax rules, even if you don't have a physical office south of the border, your activities might meet the "Permanent Establishment" threshold. This triggers the need to file Form 1120-F with the IRS. Fortunately, the US-Canada Tax Treaty exists to protect Canadian SMEs from redundant taxation, allowing you to claim relief on income that would otherwise be taxed in both countries. For owners with dual interests, compliance may also extend to specialized ITIN (Individual Taxpayer Identification Number) applications or FBAR (Foreign Bank and Financial Accounts) reporting. Navigating these waters requires a proactive guardian who understands the nuances of both jurisdictions to ensure your international growth isn't hampered by avoidable penalties. Viewing tax season as a single, stressful event in the calendar is a risk most businesses can't afford to take. True security comes from a "continuous compliance" mindset, where every transaction is recorded with the expectation that it may one day be reviewed. Maintaining a high standard of Canadian corporate tax compliance requires a shift in perspective. It's about building a transparent, verifiable audit trail that exists long before the CRA sends a notice of assessment. When your records are organized and accessible, the fear of an audit transforms into the confidence of being prepared. Proactive planning reduces the likelihood of "red flags" that often trigger CRA reviews, such as inconsistent profit margins or unusual expense claims. By documenting the business purpose of every significant transaction as it happens, you create a narrative that is difficult to challenge later. If you are ready to move beyond the year-end scramble, our team provides the Canadian accounting and tax services you need to build a resilient, audit-proof business.

Digital Record-Keeping and Data Integrity

The CRA has clear expectations for record-keeping, and in 2026, those expectations are increasingly digital. To meet these standards, follow these three essential steps:

Proactive Tax Planning vs. Year-End Scrambling

Reactive filing is simply recording history. Proactive planning is about writing it. While a reactive approach focuses on what already happened, a proactive strategy allows you to shape the financial outcome. We recommend quarterly reviews to estimate your tax liabilities. This practice allows you to adjust your instalments and avoid the shock of a large balance due at the end of the year. Furthermore, it provides the opportunity to optimize the owner’s total tax position through strategic remuneration. Deciding between a salary or dividends isn't a one-time choice; it's a dynamic decision that should reflect your current cash flow needs and long-term wealth goals. This foresight ensures you aren't just meeting requirements, but actively securing a better outcome for your business legacy. Achieving a high standard of Canadian corporate tax compliance is not merely a box-ticking exercise; it's the first essential step toward comprehensive wealth preservation. For over 40 years, we've served as a steady hand for Canadian business owners, guiding them through shifting regulatory tides with institutional wisdom and a modern, forward-thinking outlook. Your business is more than just an entity. It represents your life's work and the foundation of your family’s future legacy. We believe that a proactive guardian doesn't just react to current requirements but actively looks ahead to secure a better outcome for the years to come. Stability and ethical steadfastness form the core of a successful long-term partnership. When you move beyond the stress of annual filings, you gain the clarity needed to make bold, informed decisions about your company's future. Our rhythmic approach to financial management ensures that you're never rushed or caught off guard by new CRA expectations. Instead, you're led on a guided journey from potential uncertainty toward a state of total control and understanding.

Why Boutique Expertise Surpasses Generalist Solutions

Large, distant institutions often lack the personalized touch required to understand the nuances of your specific industry. Our boutique firm provides "Big Four" level expertise while maintaining the warm, direct relationship you expect from a dedicated partner. Whether you operate in healthcare, real estate, or specialized emerging sectors, deep industry knowledge leads to superior tax outcomes. You'll work directly with senior partners who understand your business history, allowing us to identify risks and opportunities that a generalist might overlook. This bespoke approach ensures that your tax strategy is as unique as your business itself, providing a level of precision that generalist firms simply cannot match.

Integrating Wealth Management with Corporate Compliance

A corporation that maintains impeccable records is a far more effective vehicle for long-term wealth accumulation. When your Canadian corporate tax compliance is beyond reproach, you're in a much stronger position to integrate corporate earnings with personal estate and succession planning. This alignment is vital when considering the eventual sale or transition of your business. Buyers and successors look for a clean history of transparency and reliability. By treating compliance as a strategic asset, you ensure that your business remains a valuable, transferable legacy. Our goal is to move you quickly from the problems of the present to a permanent sense of resolution. To take the next step in your financial journey, Partner with Tax Partners to realize your business’s full financial potential. Mastering the landscape of Canadian corporate tax compliance is more than a regulatory necessity; it's a strategic move that protects your business's integrity and value. By shifting from a reactive year-end scramble to a proactive, digital-first framework, you ensure that every transaction serves your long-term goals. We've explored how precise bookkeeping, strategic remuneration, and a continuous compliance mindset turn complex CRA requirements into a clear path for growth. With over 40 years of Canadian and cross-border tax expertise, our team has filed more than 495,000 returns with unwavering precision. This dedication to excellence is reflected in more than 1,390 five-star reviews from business owners who trust us as their proactive guardians. Ready to transform your approach? Secure your business’s future with expert Canadian corporate tax services. You don't have to navigate these complexities alone. With a steady hand at the helm, you can focus on what you do best while we ensure your business remains resilient and ready for whatever the future holds.

What is the corporate tax filing deadline in Canada for 2026?

Under CRA rules, your T2 Corporation Income Tax Return is due within six months of your fiscal year-end. However, you must pay any balance owing much earlier. For most corporations, the payment deadline is two months after the year-end, though eligible CCPCs may have three months to settle their balance. Missing these dates leads to immediate interest charges on the outstanding amount.

Do I need to file a corporate tax return if my business made no money this year?

Yes, every resident corporation must file a T2 return for each taxation year, even if there is no tax payable or the business is inactive. These are often called "Nil returns." Filing ensures your account remains in good standing with the CRA and allows you to carry forward losses that could reduce your future tax liability when the business becomes profitable again.

How long must I keep my corporate tax records for the CRA?

You are required to maintain all financial records and supporting documents for a period of six years from the end of the last tax year to which they relate. This includes digital receipts, ledger entries, and bank statements. Keeping these records organized is a fundamental part of maintaining Canadian corporate tax compliance and ensures you are ready for any potential review or audit.

What is the difference between a CCPC and other types of corporations?

A Canadian-Controlled Private Corporation (CCPC) is a private company that is not controlled by non-resident persons or public corporations. These entities enjoy a lower federal tax rate of 9% on the first $500,000 of active business income. Other corporations, such as public or non-resident-controlled entities, are subject to the general federal tax rate, which is currently 15% after federal abatements and reductions.

Can I change my corporation’s fiscal year-end after it has been established?

Yes, you can request a change to your fiscal year-end, but it generally requires written approval from the CRA. You must provide a valid business reason for the change, such as aligning with a new parent company or a significant shift in your seasonal business cycle. Changes made solely for the purpose of minimizing taxes are typically not approved by the tax authorities.

What happens if I miss the deadline for paying my corporate tax balance?

Missing the payment deadline triggers immediate interest charges, which the CRA calculates at the prescribed interest rate plus 4%. If you also fail to file your return on time, you'll face a late-filing penalty of 5% of the balance owing, plus an additional 1% for each full month the return is late. These costs can escalate quickly, especially for repeated late filers who face even higher penalties.

Does my Canadian corporation need to file taxes in the US if I have American customers?

Having American customers doesn't automatically trigger a US tax filing, but having a "Permanent Establishment" south of the border usually does. Under IRS rules, you may be required to file Form 1120-F. It's essential to consult the US-Canada Tax Treaty to determine if your specific activities, such as having a physical office or employees in the US, create a formal filing obligation.

How can I reduce the risk of a CRA audit for my small business?

Reducing audit risk starts with maintaining high standards of Canadian corporate tax compliance through meticulous record-keeping and consistent reporting. Avoid "red flags" like large discrepancies between your GST/HST filings and reported income or unusual expense claims that don't align with industry norms. Engaging a professional CPA to review your returns before submission provides an added layer of scrutiny that identifies potential issues early.