Tax Optimization for Business Owners: A Strategic Canadian Guide

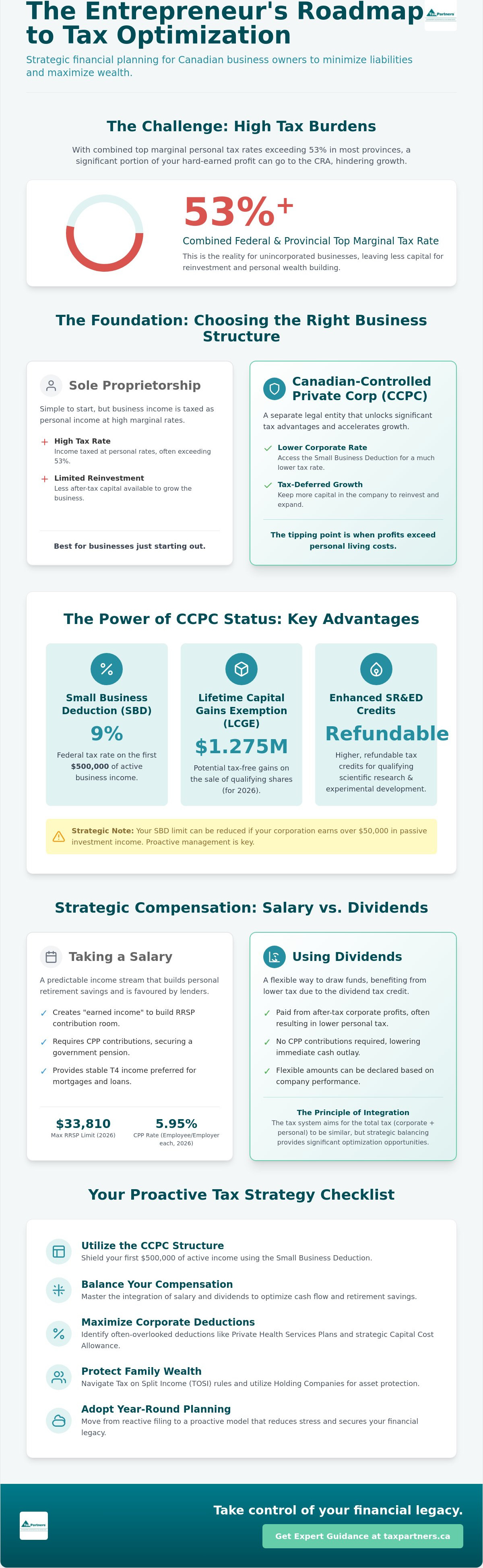

With combined federal and provincial top marginal personal tax rates exceeding 53 percent in most provinces, many entrepreneurs realize that tax optimization for business owners is the difference between stagnation and significant growth. It's a frustrating reality when you've dedicated years to building a profitable enterprise only to see the CRA take a substantial portion. You likely feel the pressure of ever-changing regulations and the delicate balance of maintaining personal cash flow while keeping corporate tax efficiency high. The fear of an audit often looms over complex planning, making it difficult to feel truly confident in your financial direction.

This guide provides a strategic roadmap for your finances, showing you how to integrate corporate and personal strategies to minimize liabilities and maximize long-term wealth. You'll gain a clear understanding of the salary versus dividend debate and how to leverage the $1.275 million lifetime capital gains exemption. We will move from the uncertainty of annual filings toward a state of total control over your financial legacy and succession planning.

Key Takeaways

- Understand how a Canadian-Controlled Private Corporation (CCPC) structure shields your first $500,000 of active income through the Small Business Deduction.

- Balance your compensation by mastering the integration of salary and dividends to optimize personal cash flow and retirement savings.

- Identify often-overlooked deductions like Private Health Services Plans and strategic Capital Cost Allowance to enhance tax optimization for business owners.

- Protect your family’s wealth by navigating Tax on Split Income (TOSI) rules and utilizing Holding Companies for inter-corporate dividend security.

- Transition to a proactive, year-round planning model that reduces the stress of CRA audits while securing your long-term financial legacy.

The Foundation: Choosing the Right Business Structure for Optimization

The path to effective tax optimization for business owners begins long before you file your annual return. It starts with the very architecture of your enterprise. While many entrepreneurs begin as sole proprietors for simplicity, there comes a moment where this structure becomes a financial anchor rather than a sail. Transitioning to a Canadian-Controlled Private Corporation (CCPC) is often the most significant move you can make to protect your earnings and accelerate growth.

Sole Proprietorship vs. Incorporation

As a sole proprietor, your business income is your personal income. You're taxed at progressive rates that can quickly exceed 53 percent in most provinces. This leaves little room for reinvestment. Incorporation introduces a distinct legal entity, allowing you to access the lower Corporate tax in Canada. The "tipping point" usually occurs when your business generates more profit than you need for personal living expenses. By keeping excess funds within the corporation, you benefit from tax deferral. You pay a much lower immediate rate and allow more capital to work for you. While incorporation involves higher legal and professional fees, the potential tax savings often justify the investment once your active income consistently exceeds your personal needs.

The Power of the CCPC Status

Achieving CCPC status is like unlocking a premium tier of the Canadian tax system. To qualify, your company must be a private corporation controlled by Canadian residents. This designation grants you access to the Small Business Deduction (SBD). This deduction reduces the federal tax rate to just 9 percent on the first $500,000 of active business income. When combined with provincial rates, the total tax is significantly lower than personal marginal rates. Beyond annual savings, CCPC status provides two vital long-term advantages:

- The Lifetime Capital Gains Exemption (LCGE): For 2026, you can potentially exempt up to $1.275 million in gains from the sale of qualifying shares. This is a cornerstone of tax optimization for business owners.

- Enhanced SR&ED Credits: CCPCs often receive higher, refundable tax credits for research and development activities.

Foresight is required. If your corporation earns more than $50,000 in passive investment income, the CRA begins to reduce your SBD limit. This makes it essential to balance your corporate investments with your active business operations to maintain your preferential tax status. We help you monitor these thresholds to ensure your structure remains an asset rather than a liability.

Strategic Compensation: Salary vs. Dividends and the Owner-Manager Balance

Deciding how to draw money from your business is a pivotal moment in tax optimization for business owners. The Canadian tax system operates on the principle of integration. This concept suggests that the total tax paid should be relatively consistent whether you earn income personally or through a corporation. While perfect integration is rare, understanding this framework helps you avoid double taxation. It allows you to align your compensation with your personal financial goals and the Canada Revenue Agency (CRA) corporate tax information regarding distributions.

The Case for Taking a Salary

Drawing a salary provides a steady, predictable income stream that simplifies personal financial planning. It's classified as "earned income," which is the essential fuel for your Registered Retirement Savings Plan (RRSP). For 2026, the RRSP contribution limit has risen to $33,810, but you can only reach this maximum if you've generated sufficient earned income in previous years. Salary also requires contributions to the Canada Pension Plan (CPP). While this is an added cost, with the 2026 employee and employer rates at 5.95 percent each, it secures a foundational government pension for your future. Lenders also prefer the stability of a T4 salary when you're applying for a personal mortgage or significant credit line.

The Dividend Advantage

Dividends offer a more flexible, often lower-cost alternative to a traditional salary. Because the corporation pays dividends out of after-tax profits, you receive a federal dividend tax credit to compensate for the tax already paid at the corporate level. For 2026, non-eligible dividends are grossed-up by 15 percent with a federal tax credit of 9.03 percent of that grossed-up amount. This often results in a lower immediate personal tax bill. Dividends don't require CPP contributions, which can save a self-employed owner up to $8,460.90 in 2026. However, you must be mindful of the "Tax on Split Income" (TOSI) rules. These regulations generally prevent you from sprinkling dividends to family members who aren't actively involved in the business, taxing that income at the highest marginal rate instead.

The ideal strategy usually isn't an "either-or" choice. It's a calculated blend. Younger owners might prioritize a salary to build RRSP room and CPP credits. Those nearing retirement or with high corporate investment income might lean toward dividends to manage their personal tax brackets more effectively. Finding the right mix requires a deep look at your lifestyle and long-term wealth preservation goals. If you're unsure which path fits your current growth stage, professional tax planning can provide the clarity you need to move forward with confidence.

Maximizing Corporate Deductions and Modern Tax Credits

Operational efficiency is just as vital as your corporate structure. True tax optimization for business owners involves scouring your ledger for every legitimate deduction the CRA permits. This isn't about aggressive loopholes; it's about utilizing specific incentives designed to stimulate Canadian business growth. From depreciating assets to claiming innovation credits, your day-to-day spending should work in tandem with your long-term wealth goals. By identifying these opportunities early, you transform routine expenses into strategic tax shields.

Accelerating Capital Cost Allowance (CCA)

The timing of your asset purchases can significantly impact your immediate cash flow. Under the standard half-year rule, you generally only claim 50 percent of the allowable CCA on an asset in the year you acquire it. However, current regulations for CCPCs allow for the immediate expensing of up to $1.5 million in eligible property. This includes many types of equipment and machinery that drive your business forward. Strategic timing of these purchases toward the end of your fiscal year can result in a substantial first-year tax shield. Remember that CCA recapture will increase your taxable income if you later sell an asset for more than its undepreciated capital cost.

Unlocking SR&ED and Innovation Incentives

Many entrepreneurs mistakenly believe the Scientific Research and Experimental Development (SR&ED) program is reserved for high-tech laboratories. In reality, it supports any business that faces technical uncertainty while trying to improve a product or process. If you've spent weeks troubleshooting a software architecture or refining a manufacturing workflow, you likely qualify. For CCPCs, the SR&ED credit is exceptionally valuable because the federal portion is often refundable. This means you receive cash back even if your business isn't currently profitable. Success here depends on precision; you must maintain meticulous records of your technical challenges and failed attempts to satisfy a CRA review.

Don't overlook the smaller, consistent wins. A Private Health Services Plan (PHSP) allows your corporation to deduct 100 percent of health and dental costs for you and your family as a legitimate business expense. This effectively turns a personal, after-tax cost into a corporate deduction. These incremental strategies, combined with home office deductions and green energy incentives, ensure you aren't leaving money on the table. We help you identify these often-missed opportunities to ensure your tax optimization for business owners is as comprehensive as possible.

Advanced Strategies: Income Splitting and Cross-Border Optimization

Scaling a business requires a shift from basic tax reduction to sophisticated wealth preservation. Advanced tax optimization for business owners often involves the use of Holding Companies. These entities act as a protective layer, allowing you to move excess profits from your operating company via tax-free inter-corporate dividends. This strategy secures your capital from operational risks while facilitating easier reinvestment into other ventures. For entrepreneurs over age 40, the Individual Pension Plan (IPP) serves as a powerful alternative to the RRSP. It allows for significantly higher contribution limits, providing a predictable retirement income while creating a substantial corporate deduction.

The Evolution of Income Splitting

Tax planning changed significantly after 2018 with the expansion of the Tax on Split Income (TOSI) rules. The CRA now scrutinizes dividends paid to family members with much greater intensity. To successfully split income, you must meet specific exceptions. The "Excluded Business" rule applies if a family member works an average of 20 hours per week in the business. Another path is the "Excluded Shares" exception, available to family members over age 25 who own at least 10 percent of the company’s votes and value. Paying a reasonable salary to family members for actual work remains a steadfast strategy. For those planning an eventual exit, a Family Trust can multiply the $1.275 million Lifetime Capital Gains Exemption among several family members, potentially saving millions in taxes upon the sale of the business.

Cross-Border Compliance for the Global Owner

Expanding into the United States or holding dual citizenship introduces a layer of regulatory friction that few domestic firms can manage. Dual citizens often face US "Controlled Foreign Corporation" rules, which may tax Canadian corporate income even if it stays inside the company. The US-Canada Tax Treaty provides essential relief from double taxation, but only if your filings are precise. We provide specialized US and cross-border accounting to ensure your international growth doesn't become a compliance nightmare. Managing these complexities is a critical component of tax optimization for business owners with a global footprint.

If your business operations cross the border or involve complex family dynamics, you need a strategy that accounts for every variable. You can request a cross-border consultation today to secure your international interests and protect your family's financial future.

The Proactive Path: Year-Round Planning and Expert Advisory

Tax optimization for business owners is not a once-a-year event; it's a continuous commitment to financial health. While many entrepreneurs treat their tax return as a rearview mirror, the most successful realize that the greatest savings are found through the windshield. Shifting from a reactive mindset to a proactive one allows you to adjust your strategies as your revenue fluctuates. By the time your corporate tax return is due, which is six months after your fiscal year-end, the most impactful decisions should have already been made and documented.

The Cost of Reactive Accounting

Relying on "DIY" software or waiting until the last minute often leads to expensive oversights. These tools frequently fail to capture the nuanced integration between your corporate structure and personal wealth goals. Poor record-keeping or missed deadlines result in non-deductible penalties and interest that can quickly erode your hard-earned profits. For instance, while self-employed individuals have until June 15 to file their 2025 personal returns, any taxes owed are due by April 30, 2026. Missing these windows creates unnecessary stress. Professional advisory provides the steady hand you need, offering robust support if the CRA ever selects your business for an audit.

Building a Long-Term Partnership

True financial security comes from a relationship with a firm that acts as a proactive guardian of your interests. At Tax Partners, we integrate wealth management and tax planning to create a bespoke experience tailored to your specific industry. We don't just record history; we help you write it. Our approach moves beyond simple compliance to ensure that every dollar in your business is positioned for maximum growth and protection. We recommend conducting quarterly reviews to evaluate your estimated tax payments and adjust your salary-dividend mix based on real-time performance.

Reliability is the foundation of our service. With a 40-year history of helping Canadian entrepreneurs and more than 1,390 five-star reviews, we've built a reputation for ethical steadfastness and deep-seated expertise. We invite you to move from a state of potential uncertainty toward total control over your financial legacy. Effective tax optimization for business owners requires foresight and precision. You can reach out for a consultation today to realize the full potential of your enterprise and secure the long-term wealth you've worked so hard to build.

Secure Your Financial Legacy and Future Growth

You've built a successful enterprise through hard work and innovation; now it's time to ensure those rewards remain with you. True tax optimization for business owners requires a holistic approach that balances corporate structure with personalized compensation strategies. By mastering the integration of salary and dividends while staying ahead of complex cross-border regulations, you move from a place of uncertainty to total financial control. Proactive planning is your most powerful tool to protect your assets and facilitate a smooth succession.

With over 40 years of Canadian tax expertise and more than 1,390 five-star Google reviews, we've helped our clients save over $87 million in taxes. Our team acts as a dedicated guardian of your wealth, ensuring you never pay more than your fair share to the CRA. You can Book a Strategic Tax Consultation with Tax Partners today to begin crafting your bespoke roadmap. Your business deserves a partner that is as invested in your success as you are. Let's work together to secure the future you've earned.

Frequently Asked Questions

What is the most effective way for a Canadian business owner to reduce taxes?

The most effective way to reduce your tax bill is through the deliberate integration of corporate and personal tax planning. By utilizing a Canadian-Controlled Private Corporation (CCPC) structure, you can access a federal tax rate of just 9 percent on your first $500,000 of active business income. This approach facilitates significant tax deferral, allowing you to reinvest more capital into your operations rather than losing it to high personal marginal rates. It's about looking at your entire financial picture as one cohesive strategy.

Is it better to take a salary or dividends from my corporation in 2026?

Choosing between salary and dividends in 2026 depends on your retirement goals and cash flow requirements. Taking a salary is essential if you want to build RRSP room, which has a 2026 limit of $33,810, or if you want to contribute to the Canada Pension Plan. Conversely, dividends avoid the 11.9 percent self-employed CPP contribution rate. Most owners find that a calculated blend of both provides the best balance of tax optimization for business owners while maintaining personal mortgage eligibility.

Can I still split income with my spouse under the new TOSI rules?

You can still split income with family members, provided you strictly adhere to the Tax on Split Income (TOSI) exceptions. The most common path is the "Excluded Business" exception, where a spouse or child over 18 works an average of 20 hours per week in the business. If they don't meet this threshold, payments may be taxed at the highest marginal rate. Precise documentation of their actual contribution to the company's daily operations is vital to satisfy any potential CRA scrutiny.

What business expenses are often missed by Canadian SMEs?

Canadian SMEs often miss out on Private Health Services Plans (PHSPs) and the full benefits of the Capital Cost Allowance (CCA). A PHSP allows your corporation to deduct 100 percent of your family's medical and dental expenses as a business cost. Additionally, many owners overlook the immediate expensing rules for CCPCs. These rules allow you to fully expense up to $1.5 million in eligible property in the first year, providing a massive upfront tax shield that significantly improves your immediate cash flow.

How does a holding company help with tax optimization?

A holding company acts as a strategic reservoir for your wealth, allowing for the tax-free transfer of dividends from your operating company. This structure protects your excess capital from the legal risks of daily operations while deferring personal taxes on those funds. It's a cornerstone of tax optimization for business owners who want to reinvest in new ventures or real estate without triggering immediate personal income tax. This layer of separation also simplifies your eventual succession or business sale planning.

What are the tax implications if I have business interests in both the US and Canada?

Operating across the border means you must navigate the complex interplay between the IRS and the CRA under the US-Canada Tax Treaty. Dual citizens or those with US operations face unique challenges like "Controlled Foreign Corporation" rules, which can trigger taxes even on income held within your Canadian company. Specialized cross-border accounting is necessary to avoid double taxation. We ensure your filings are precise and that you're taking full advantage of the treaty to protect your global earnings.

When should I incorporate my business to save on taxes?

You should consider incorporating when your business profit consistently exceeds the amount you need for personal living expenses. This transition allows you to benefit from the lower corporate tax rate and the $500,000 small business deduction limit. Incorporation also begins the clock on qualifying for the $1.275 million Lifetime Capital Gains Exemption (LCGE). This exemption is a critical tool for preserving wealth when you eventually decide to sell your business shares, making the timing of your incorporation a million-dollar decision.

How can I protect my business from a CRA audit?

The best way to protect your business from an audit is to maintain meticulous digital records and ensure all inter-company transactions are clearly documented. You should verify that any salaries paid to family members are "reasonable" for the work they perform. Moving from reactive filing to proactive, year-round tax planning ensures that your records are always audit-ready. Having a professional firm as your proactive guardian provides an essential layer of security, ensuring you don't have to face the CRA alone.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

Sole Proprietorship vs. Incorporation

As a sole proprietor, your business income is your personal income. You're taxed at progressive rates that can quickly exceed 53 percent in most provinces. This leaves little room for reinvestment. Incorporation introduces a distinct legal entity, allowing you to access the lower Corporate tax in Canada. The "tipping point" usually occurs when your business generates more profit than you need for personal living expenses. By keeping excess funds within the corporation, you benefit from tax deferral. You pay a much lower immediate rate and allow more capital to work for you. While incorporation involves higher legal and professional fees, the potential tax savings often justify the investment once your active income consistently exceeds your personal needs.

The Power of the CCPC Status

Achieving CCPC status is like unlocking a premium tier of the Canadian tax system. To qualify, your company must be a private corporation controlled by Canadian residents. This designation grants you access to the Small Business Deduction (SBD). This deduction reduces the federal tax rate to just 9 percent on the first $500,000 of active business income. When combined with provincial rates, the total tax is significantly lower than personal marginal rates. Beyond annual savings, CCPC status provides two vital long-term advantages: Foresight is required. If your corporation earns more than $50,000 in passive investment income, the CRA begins to reduce your SBD limit. This makes it essential to balance your corporate investments with your active business operations to maintain your preferential tax status. We help you monitor these thresholds to ensure your structure remains an asset rather than a liability. Deciding how to draw money from your business is a pivotal moment in tax optimization for business owners. The Canadian tax system operates on the principle of integration. This concept suggests that the total tax paid should be relatively consistent whether you earn income personally or through a corporation. While perfect integration is rare, understanding this framework helps you avoid double taxation. It allows you to align your compensation with your personal financial goals and the Canada Revenue Agency (CRA) corporate tax information regarding distributions.

The Case for Taking a Salary

Drawing a salary provides a steady, predictable income stream that simplifies personal financial planning. It's classified as "earned income," which is the essential fuel for your Registered Retirement Savings Plan (RRSP). For 2026, the RRSP contribution limit has risen to $33,810, but you can only reach this maximum if you've generated sufficient earned income in previous years. Salary also requires contributions to the Canada Pension Plan (CPP). While this is an added cost, with the 2026 employee and employer rates at 5.95 percent each, it secures a foundational government pension for your future. Lenders also prefer the stability of a T4 salary when you're applying for a personal mortgage or significant credit line.

The Dividend Advantage

Dividends offer a more flexible, often lower-cost alternative to a traditional salary. Because the corporation pays dividends out of after-tax profits, you receive a federal dividend tax credit to compensate for the tax already paid at the corporate level. For 2026, non-eligible dividends are grossed-up by 15 percent with a federal tax credit of 9.03 percent of that grossed-up amount. This often results in a lower immediate personal tax bill. Dividends don't require CPP contributions, which can save a self-employed owner up to $8,460.90 in 2026. However, you must be mindful of the "Tax on Split Income" (TOSI) rules. These regulations generally prevent you from sprinkling dividends to family members who aren't actively involved in the business, taxing that income at the highest marginal rate instead. The ideal strategy usually isn't an "either-or" choice. It's a calculated blend. Younger owners might prioritize a salary to build RRSP room and CPP credits. Those nearing retirement or with high corporate investment income might lean toward dividends to manage their personal tax brackets more effectively. Finding the right mix requires a deep look at your lifestyle and long-term wealth preservation goals. If you're unsure which path fits your current growth stage, professional tax planning can provide the clarity you need to move forward with confidence. Operational efficiency is just as vital as your corporate structure. True tax optimization for business owners involves scouring your ledger for every legitimate deduction the CRA permits. This isn't about aggressive loopholes; it's about utilizing specific incentives designed to stimulate Canadian business growth. From depreciating assets to claiming innovation credits, your day-to-day spending should work in tandem with your long-term wealth goals. By identifying these opportunities early, you transform routine expenses into strategic tax shields.

Accelerating Capital Cost Allowance (CCA)

The timing of your asset purchases can significantly impact your immediate cash flow. Under the standard half-year rule, you generally only claim 50 percent of the allowable CCA on an asset in the year you acquire it. However, current regulations for CCPCs allow for the immediate expensing of up to $1.5 million in eligible property. This includes many types of equipment and machinery that drive your business forward. Strategic timing of these purchases toward the end of your fiscal year can result in a substantial first-year tax shield. Remember that CCA recapture will increase your taxable income if you later sell an asset for more than its undepreciated capital cost.

Unlocking SR&ED and Innovation Incentives

Many entrepreneurs mistakenly believe the Scientific Research and Experimental Development (SR&ED) program is reserved for high-tech laboratories. In reality, it supports any business that faces technical uncertainty while trying to improve a product or process. If you've spent weeks troubleshooting a software architecture or refining a manufacturing workflow, you likely qualify. For CCPCs, the SR&ED credit is exceptionally valuable because the federal portion is often refundable. This means you receive cash back even if your business isn't currently profitable. Success here depends on precision; you must maintain meticulous records of your technical challenges and failed attempts to satisfy a CRA review. Don't overlook the smaller, consistent wins. A Private Health Services Plan (PHSP) allows your corporation to deduct 100 percent of health and dental costs for you and your family as a legitimate business expense. This effectively turns a personal, after-tax cost into a corporate deduction. These incremental strategies, combined with home office deductions and green energy incentives, ensure you aren't leaving money on the table. We help you identify these often-missed opportunities to ensure your tax optimization for business owners is as comprehensive as possible. Scaling a business requires a shift from basic tax reduction to sophisticated wealth preservation. Advanced tax optimization for business owners often involves the use of Holding Companies. These entities act as a protective layer, allowing you to move excess profits from your operating company via tax-free inter-corporate dividends. This strategy secures your capital from operational risks while facilitating easier reinvestment into other ventures. For entrepreneurs over age 40, the Individual Pension Plan (IPP) serves as a powerful alternative to the RRSP. It allows for significantly higher contribution limits, providing a predictable retirement income while creating a substantial corporate deduction.

The Evolution of Income Splitting

Tax planning changed significantly after 2018 with the expansion of the Tax on Split Income (TOSI) rules. The CRA now scrutinizes dividends paid to family members with much greater intensity. To successfully split income, you must meet specific exceptions. The "Excluded Business" rule applies if a family member works an average of 20 hours per week in the business. Another path is the "Excluded Shares" exception, available to family members over age 25 who own at least 10 percent of the company’s votes and value. Paying a reasonable salary to family members for actual work remains a steadfast strategy. For those planning an eventual exit, a Family Trust can multiply the $1.275 million Lifetime Capital Gains Exemption among several family members, potentially saving millions in taxes upon the sale of the business.

Cross-Border Compliance for the Global Owner

Expanding into the United States or holding dual citizenship introduces a layer of regulatory friction that few domestic firms can manage. Dual citizens often face US "Controlled Foreign Corporation" rules, which may tax Canadian corporate income even if it stays inside the company. The US-Canada Tax Treaty provides essential relief from double taxation, but only if your filings are precise. We provide specialized US and cross-border accounting to ensure your international growth doesn't become a compliance nightmare. Managing these complexities is a critical component of tax optimization for business owners with a global footprint. If your business operations cross the border or involve complex family dynamics, you need a strategy that accounts for every variable. You can request a cross-border consultation today to secure your international interests and protect your family's financial future. Tax optimization for business owners is not a once-a-year event; it's a continuous commitment to financial health. While many entrepreneurs treat their tax return as a rearview mirror, the most successful realize that the greatest savings are found through the windshield. Shifting from a reactive mindset to a proactive one allows you to adjust your strategies as your revenue fluctuates. By the time your corporate tax return is due, which is six months after your fiscal year-end, the most impactful decisions should have already been made and documented.

The Cost of Reactive Accounting

Relying on "DIY" software or waiting until the last minute often leads to expensive oversights. These tools frequently fail to capture the nuanced integration between your corporate structure and personal wealth goals. Poor record-keeping or missed deadlines result in non-deductible penalties and interest that can quickly erode your hard-earned profits. For instance, while self-employed individuals have until June 15 to file their 2025 personal returns, any taxes owed are due by April 30, 2026. Missing these windows creates unnecessary stress. Professional advisory provides the steady hand you need, offering robust support if the CRA ever selects your business for an audit.

Building a Long-Term Partnership

True financial security comes from a relationship with a firm that acts as a proactive guardian of your interests. At Tax Partners, we integrate wealth management and tax planning to create a bespoke experience tailored to your specific industry. We don't just record history; we help you write it. Our approach moves beyond simple compliance to ensure that every dollar in your business is positioned for maximum growth and protection. We recommend conducting quarterly reviews to evaluate your estimated tax payments and adjust your salary-dividend mix based on real-time performance. Reliability is the foundation of our service. With a 40-year history of helping Canadian entrepreneurs and more than 1,390 five-star reviews, we've built a reputation for ethical steadfastness and deep-seated expertise. We invite you to move from a state of potential uncertainty toward total control over your financial legacy. Effective tax optimization for business owners requires foresight and precision. You can reach out for a consultation today to realize the full potential of your enterprise and secure the long-term wealth you've worked so hard to build. You've built a successful enterprise through hard work and innovation; now it's time to ensure those rewards remain with you. True tax optimization for business owners requires a holistic approach that balances corporate structure with personalized compensation strategies. By mastering the integration of salary and dividends while staying ahead of complex cross-border regulations, you move from a place of uncertainty to total financial control. Proactive planning is your most powerful tool to protect your assets and facilitate a smooth succession. With over 40 years of Canadian tax expertise and more than 1,390 five-star Google reviews, we've helped our clients save over $87 million in taxes. Our team acts as a dedicated guardian of your wealth, ensuring you never pay more than your fair share to the CRA. You can Book a Strategic Tax Consultation with Tax Partners today to begin crafting your bespoke roadmap. Your business deserves a partner that is as invested in your success as you are. Let's work together to secure the future you've earned.

What is the most effective way for a Canadian business owner to reduce taxes?

The most effective way to reduce your tax bill is through the deliberate integration of corporate and personal tax planning. By utilizing a Canadian-Controlled Private Corporation (CCPC) structure, you can access a federal tax rate of just 9 percent on your first $500,000 of active business income. This approach facilitates significant tax deferral, allowing you to reinvest more capital into your operations rather than losing it to high personal marginal rates. It's about looking at your entire financial picture as one cohesive strategy.

Is it better to take a salary or dividends from my corporation in 2026?

Choosing between salary and dividends in 2026 depends on your retirement goals and cash flow requirements. Taking a salary is essential if you want to build RRSP room, which has a 2026 limit of $33,810, or if you want to contribute to the Canada Pension Plan. Conversely, dividends avoid the 11.9 percent self-employed CPP contribution rate. Most owners find that a calculated blend of both provides the best balance of tax optimization for business owners while maintaining personal mortgage eligibility.

Can I still split income with my spouse under the new TOSI rules?

You can still split income with family members, provided you strictly adhere to the Tax on Split Income (TOSI) exceptions. The most common path is the "Excluded Business" exception, where a spouse or child over 18 works an average of 20 hours per week in the business. If they don't meet this threshold, payments may be taxed at the highest marginal rate. Precise documentation of their actual contribution to the company's daily operations is vital to satisfy any potential CRA scrutiny.

What business expenses are often missed by Canadian SMEs?

Canadian SMEs often miss out on Private Health Services Plans (PHSPs) and the full benefits of the Capital Cost Allowance (CCA). A PHSP allows your corporation to deduct 100 percent of your family's medical and dental expenses as a business cost. Additionally, many owners overlook the immediate expensing rules for CCPCs. These rules allow you to fully expense up to $1.5 million in eligible property in the first year, providing a massive upfront tax shield that significantly improves your immediate cash flow.

How does a holding company help with tax optimization?

A holding company acts as a strategic reservoir for your wealth, allowing for the tax-free transfer of dividends from your operating company. This structure protects your excess capital from the legal risks of daily operations while deferring personal taxes on those funds. It's a cornerstone of tax optimization for business owners who want to reinvest in new ventures or real estate without triggering immediate personal income tax. This layer of separation also simplifies your eventual succession or business sale planning.

What are the tax implications if I have business interests in both the US and Canada?

Operating across the border means you must navigate the complex interplay between the IRS and the CRA under the US-Canada Tax Treaty. Dual citizens or those with US operations face unique challenges like "Controlled Foreign Corporation" rules, which can trigger taxes even on income held within your Canadian company. Specialized cross-border accounting is necessary to avoid double taxation. We ensure your filings are precise and that you're taking full advantage of the treaty to protect your global earnings.

When should I incorporate my business to save on taxes?

You should consider incorporating when your business profit consistently exceeds the amount you need for personal living expenses. This transition allows you to benefit from the lower corporate tax rate and the $500,000 small business deduction limit. Incorporation also begins the clock on qualifying for the $1.275 million Lifetime Capital Gains Exemption (LCGE). This exemption is a critical tool for preserving wealth when you eventually decide to sell your business shares, making the timing of your incorporation a million-dollar decision.

How can I protect my business from a CRA audit?

The best way to protect your business from an audit is to maintain meticulous digital records and ensure all inter-company transactions are clearly documented. You should verify that any salaries paid to family members are "reasonable" for the work they perform. Moving from reactive filing to proactive, year-round tax planning ensures that your records are always audit-ready. Having a professional firm as your proactive guardian provides an essential layer of security, ensuring you don't have to face the CRA alone.