Holding Company Tax Planning in Canada: A Strategic Guide for 2026

Could your current corporate structure be quietly disqualifying you from a $1.275 million tax-free windfall? Many successful entrepreneurs feel the weight of high personal tax brackets and worry that their hard-earned retained earnings are sitting ducks for potential creditors. It's a common concern, especially when you realize that proactive holding company tax planning is often the only thing standing between your wealth and a 39 percent tax hit on personal dividend income. You've worked hard to build your business, and it's only natural to want to protect that legacy from unnecessary tax erosion and legal risks.

This guide will show you how a tailored corporate structure can shield your assets, keep your Lifetime Capital Gains Exemption intact, and facilitate the tax-free movement of cash between your businesses. We'll explore the 2026 regulatory environment, including how to manage the $50,000 passive income threshold and implement the purification strategies needed to secure your family's financial future. By the end of this article, you'll have a clear roadmap for moving from financial uncertainty to a position of total control over your corporate wealth.

Key Takeaways

- Understand how a Holdco and Opco structure creates a protective barrier between your active business operations and your accumulated wealth.

- Master the art of holding company tax planning to move profits as tax-free inter-corporate dividends, effectively creating a private corporate bank for future ventures.

- Learn how to navigate the $50,000 passive income threshold to protect your Small Business Deduction and keep your corporate tax rates as low as possible.

- Discover the purification techniques required to ensure your business qualifies for the $1.275 million Lifetime Capital Gains Exemption when it's time to sell.

- Recognize why a bespoke strategy is essential for aligning your corporate structure with your family's long-term financial security and succession goals.

What is a Canadian Holding Company (Société de Portefeuille)?

A Canadian holding company is a corporation that doesn't produce its own products or provide services directly to the public. Instead, its primary purpose is to own assets, such as shares in other companies, real estate, or investment portfolios. To understand the foundational concept of What is a Holding Company?, think of it as a specialized entity designed to house wealth rather than generate it through day-to-day operations. In Canada, we often refer to this as a "Holdco," while the business doing the actual work is known as an "Opco."

In legal and accounting circles, particularly within Quebec or when dealing with bilingual regulatory frameworks, you'll frequently hear the term société de portefeuille. This isn't just a simple translation; it reflects a specific corporate status that carries significant weight in holding company tax planning. Professionals also distinguish between a passive holding company and an active one, often called a société animatrice. An active holding company is more than just a vault for cash. It's actively involved in the management or financing of its subsidiaries, which can sometimes provide access to specific tax advantages that a purely passive entity cannot reach.

The Relationship Between Holdco and Opco

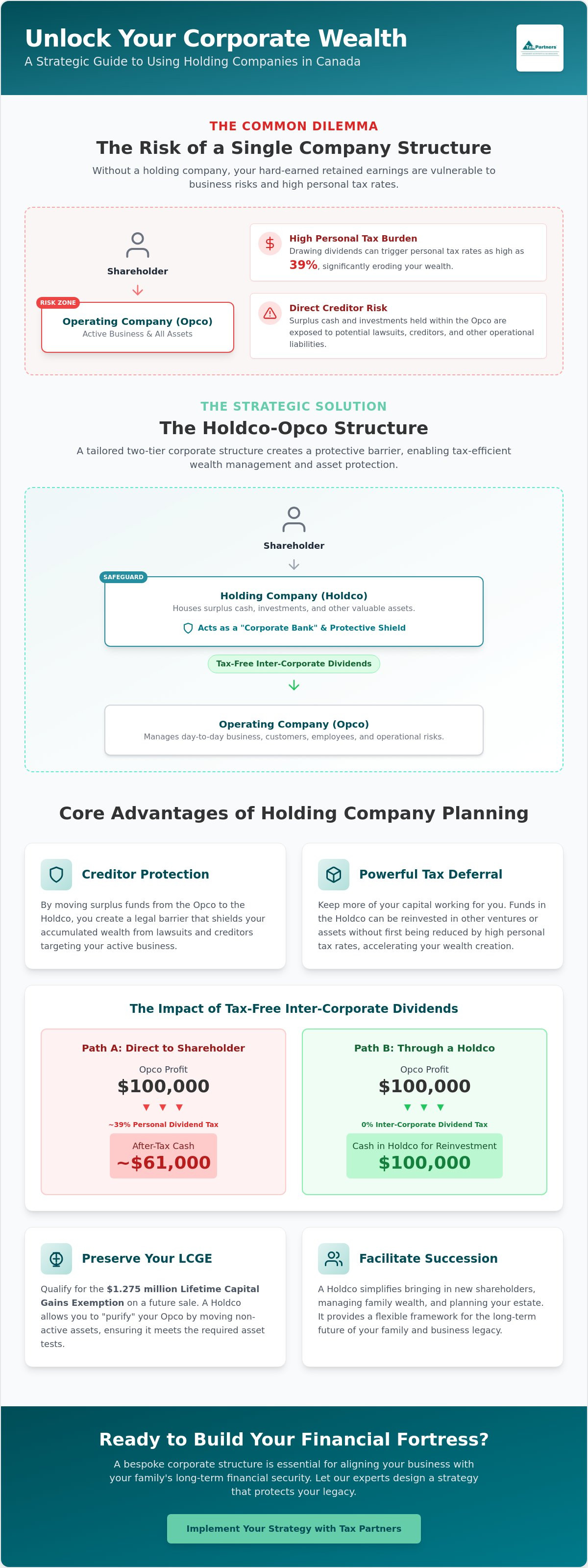

The most common structure involves a parent company (Holdco) sitting directly above an operating business (Opco). This hierarchy creates a clear division of labour. While the Opco manages the front line risks of employees, customers, and suppliers, the Holdco acts as a central reservoir for surplus capital. Moving excess cash from the Opco to the Holdco effectively moves it out of the line of fire. This structure serves as the bedrock for sophisticated holding company tax planning, allowing for the tax-efficient transfer of funds before they're exposed to the higher personal tax rates associated with individual withdrawals.

Common Use Cases for Canadian Entrepreneurs

Business owners often adopt this model to consolidate multiple ventures under one roof, making it easier to manage cash flow across different industries. It's also a powerful tool for risk mitigation. For example, you might house your company's valuable intellectual property or real estate in a Holdco while the Opco handles the riskier operational tasks. If the Opco faces a legal challenge, the assets in the Holdco remain protected. A tiered structure is also indispensable for succession. It allows you to introduce new shareholders or prepare for a sale without disrupting the core operations of the business. It's a proactive way to build a legacy that lasts.

Primary Tax Benefits: Inter-Corporate Dividends and Deferral

One of the most compelling reasons for holding company tax planning is the ability to move funds between connected corporations tax-free. Section 112 of the Income Tax Act serves as the engine for this strategy. It allows an operating company to pay dividends to its parent holding company without any immediate tax consequences. This is a massive advantage compared to taking a personal dividend, which in 2026 can attract tax rates of nearly 39 percent for high-income earners in provinces like Ontario. By keeping the cash within the corporate group, you protect it from both high personal taxes and the operational risks of the Opco.

This structure essentially turns your Holdco into a "corporate bank." The power of tax deferral lies in its ability to keep more of your capital working for you. When you withdraw profits personally, you're often left with 60 or 70 cents on the dollar after the CRA takes its share. By moving those funds to a Holdco, you keep 100 cents on the dollar to reinvest in new ventures or passive assets. It's about maintaining financial momentum. This strategy is a cornerstone of effective holding company tax planning, especially for entrepreneurs looking to scale without the friction of immediate personal tax liabilities. To maximize these efficiencies, Bluecrest Tax Advisors offers strategic tax reduction analysis to identify significant savings opportunities for high-income clients.

Under the 2026 rules, navigating the Tax on Split Income (TOSI) remains a priority. While the rules are strict, a well-structured holding company still offers legitimate ways to manage family wealth. You must ensure you meet the "excluded business" or "excluded shares" criteria to avoid the highest marginal tax rate on payments to family members. It requires precision and a proactive approach to ensure your income-splitting strategies remain compliant with current legislation.

The Section 85 Rollover: Transitioning Without Tax

Transitioning your existing business into a Holdco structure doesn't have to be a taxable event. A Section 85 rollover is a tax-neutral transfer mechanism that allows Canadian shareholders to move assets into a corporation in exchange for shares without triggering immediate capital gains. To execute this correctly, you must file a valid election with the CRA, ensuring the "agreed amount" falls within the specific limits defined by the Income Tax Act. This technical maneuver allows you to reorganize your affairs while preserving your hard-earned equity for the long term.

Optimizing Shareholder Remuneration

Deciding between a salary or a dividend is a classic dilemma that becomes more nuanced with a holding company. You can use your Holdco to time personal income spikes, keeping yourself in a lower tax bracket during high-profit years by retaining funds in the corporation. Additionally, the Capital Dividend Account (CDA) is a vital tool. It allows you to distribute the non-taxable portion of capital gains to shareholders entirely tax-free. Consulting with a firm that specializes in Canadian accounting and tax services can help you determine the ideal balance for your specific financial goals.

Identifying Risks: Passive Income and the SBD Grind

Many entrepreneurs hesitate to implement a Holdco because they fear it might jeopardize their Small Business Deduction (SBD). It's a legitimate concern. Within the framework of holding company tax planning, the "SBD grind" is a pivotal risk factor that requires proactive management. The Canadian tax system reduces the business limit for corporations that generate significant passive investment income. Once your associated corporate group earns more than $50,000 in Adjusted Aggregate Investment Income (AAII), your access to the lower 9 percent federal small business tax rate starts to shrink.

The math is unforgiving. For every $1 of investment income earned above the $50,000 threshold, your $500,000 small business limit drops by $5. By the time your passive income hits $150,000, your SBD is gone. This shift can push your active business income from a combined tax rate of approximately 12.2 percent in Ontario up to the general rate of 26.5 percent. Meticulous bookkeeping and precise filing are your only defences against an unexpected CRA audit. You must track every dollar of interest, rental income, and capital gains to ensure your corporate group stays within these critical limits.

CRA Scrutiny and Anti-Avoidance Rules

The 2026 tax landscape involves heightened vigilance from the CRA, particularly regarding the General Anti-Avoidance Rule (GAAR). Strategies that lack genuine commercial substance or exist solely to circumvent passive income rules are under the microscope. You must document inter-company loans with formal agreements and market-interest rates to avoid "deemed dividend" traps. If the CRA perceives a structure as a "sham," the resulting reassessments and penalties can quickly erase any intended tax savings. Maintaining corporate integrity is not just a best practice; it's a survival strategy.

Managing the Complexity of Multiple Corporations

Adding a holding company increases your administrative overhead. You'll face higher costs for professional accounting and tax preparation because you're now filing for two or more entities. Coordinating year-ends is a strategic move that can maximize tax deferral, but it requires careful planning. Most business owners find the "break-even" point occurs when the tax-free inter-corporate dividends and asset protection benefits significantly outweigh these annual compliance costs. It's about finding the right balance between sophisticated protection and manageable complexity for your specific situation.

Purification and the Lifetime Capital Gains Exemption (LCGE)

For many Canadian founders, the Lifetime Capital Gains Exemption (LCGE) represents the ultimate reward for years of risk and hard work. In 2026, this exemption shelters approximately $1,275,000 of capital gains from tax, potentially saving an individual over $250,000 in personal taxes upon the sale of their business. However, this benefit isn't automatic. To qualify, your company must meet the strict definition of a Qualified Small Business Corporation (QSBC). This is where holding company tax planning becomes an essential defensive strategy rather than just a financial preference.

The Canada Revenue Agency applies two primary asset tests to determine QSBC status. Throughout the 24 months before a sale, more than 50 percent of the fair market value of the corporation's assets must be used in an active business carried on primarily in Canada. More critically, the LCGE requires 90% of assets to be used in active business at the time of sale. If your operating company (Opco) accumulates too much "dead" asset value, such as excess cash, GICs, or investment properties, you risk failing these tests and losing the exemption entirely. A holding company acts as a vital purification tool, siphoning off these redundant assets to keep the Opco "pure" and compliant.

The Multi-Year Purification Strategy

Purification isn't a one-time event you can handle weeks before a sale; it requires a disciplined, multi-year approach. You don't want to be caught with a balance sheet full of passive investments when a surprise acquisition offer arrives. Effective purification follows a steady rhythm:

- Quarterly Monitoring: Review your Opco's balance sheet every three months to identify non-active assets that could jeopardize your QSBC status.

- Inter-Corporate Dividends: Use the tax-free transfer mechanisms discussed earlier to move surplus cash and investments from the Opco to your Holdco.

- Strategic Reinvestment: Once the funds are safely in the Holdco, you can invest them in real estate or securities without those assets counting against your 90 percent active asset test in the Opco.

Multiplying the Exemption Through Family

A sophisticated holding company tax planning strategy often involves a Family Trust. By having a trust own shares in your Holdco, you can potentially multiply the $1,275,000 LCGE across multiple family members, provided you navigate the 2026 TOSI rules carefully. This structure is frequently paired with an "estate freeze," which locks in the current value of the business for the founder while allowing future growth to accrue to the next generation. If you're planning an exit or a transition, our experts in Canadian accounting and tax services can help you purify your structure and maximize your family's after-tax wealth.

Implementing Your Strategy with Tax Partners

Successful holding company tax planning isn't a product you buy off the shelf. It's a living strategy that must evolve alongside your business and your family's changing needs. At Tax Partners, we've spent 40 years helping Canadian SMEs navigate the complexities of corporate tax evolution. We recognize that no two businesses are identical. A structure that works for a real estate holding company won't necessarily suit a manufacturing firm looking for a five-year exit. We act as your proactive guardian, spotting potential CRA pitfalls and regulatory shifts before they become costly liabilities.

Our approach integrates corporate accounting with wealth management and estate planning under a single roof. This holistic view ensures that every inter-corporate dividend or share reorganization serves a broader purpose. We don't just react to requirements; we look ahead to secure a better outcome for your estate. By housing these diverse financial disciplines together, we provide a seamless experience that eliminates the friction often found when working with multiple, disconnected advisors. It's about providing a steady hand at the helm while you focus on growing your enterprise.

The Tax Partners Planning Process

Assessing your current corporate health is our first priority. We begin with an initial diagnostic to understand your current structure and your long-term financial goals. Once we have a clear roadmap, our team manages the technical design and execution of Section 85 rollovers or complex share reorganizations with meticulous precision. Our commitment continues well after the initial setup. we provide ongoing vigilance through quarterly reviews to ensure your Opco remains pure for the LCGE and your Small Business Deduction is optimized against the 2026 passive income rules.

A Steady Hand for Your Corporate Future

Moving from a state of financial uncertainty to a feeling of total control over your tax liabilities is a transformative experience for any entrepreneur. You deserve the peace of mind that comes from a long-term partnership with seasoned CPAs who are deeply invested in your success. We combine decades of institutional wisdom with a modern, forward-thinking outlook to protect what you've built. It's about more than just numbers; it's about securing your family's hard-earned legacy. Secure your business legacy with a custom holding company strategy from Tax Partners.

Secure Your Corporate Legacy Today

Effective holding company tax planning is the foundation of a resilient financial future. We've explored how a Holdco serves as a protective vault for your wealth, allowing you to move profits tax-free and keep your business "pure" for the $1.275 million capital gains exemption. This isn't just about immediate savings. It's about building a structure that withstands the complexities of the 2026 tax landscape while securing your family's long-term interests. You've invested years into your business, and your corporate structure should reflect that dedication.

With over 40 years of Canadian tax expertise and more than 495,000 returns filed, our team has saved over $87 million for our clients. Our 1,390+ five-star Google reviews reflect our commitment to being a proactive guardian for every business owner we serve. Don't leave your hard-earned equity to chance. Book a consultation with Tax Partners to optimize your corporate structure and gain total control over your financial roadmap. You've worked hard to build your success. We're here to ensure it stays protected for the generations to come.

Frequently Asked Questions

What is the primary purpose of a holding company for a Canadian small business?

The primary purpose of a Canadian holding company is to protect corporate assets from business liabilities and facilitate tax-efficient wealth accumulation. By housing surplus cash or investments in a separate entity, you shield those resources from potential creditors of your operating company. This structure also enables seamless inter-corporate dividends, allowing you to move funds without triggering the high personal tax rates associated with individual income.

Can a holding company help me avoid paying personal income tax?

A holding company does not allow you to avoid personal income tax entirely, but it is a powerful tool for tax deferral. You only pay personal tax when you withdraw funds from the corporation as a salary or dividend. By retaining earnings within the Holdco, you keep more capital working for you at the lower corporate tax rate, which is a core benefit of proactive holding company tax planning.

How does the CRA define passive income within a holding company in 2026?

In 2026, the CRA defines passive income as Adjusted Aggregate Investment Income (AAII), which includes interest, rental income, and taxable capital gains. This definition is critical because once your corporate group earns more than $50,000 in AAII, your Small Business Deduction begins to decrease. This "grind" reduces your access to the 9 percent federal small business tax rate, eventually eliminating it once passive income reaches $150,000.

Is it expensive to maintain a holding company in Canada?

Maintaining a holding company involves additional costs, including separate annual tax filings, bookkeeping, and legal minute book updates. While these administrative expenses are higher than managing a single corporation, the tax savings and asset protection benefits often outweigh the overhead for established businesses. Most owners find the structure becomes cost-effective once their operating company consistently generates more cash than is needed for personal living expenses.

Can I use my holding company to buy a personal home or vehicle?

Using a holding company to purchase personal assets like a home or vehicle is generally ill-advised because it triggers "shareholder benefit" rules. The CRA views the personal use of corporate assets as a taxable benefit, meaning you would likely pay tax on the value of that use as if it were income. It's almost always more tax-efficient to buy personal assets with after-tax personal funds rather than risking a costly audit.

What happens to the Lifetime Capital Gains Exemption if I have a holding company?

A holding company protects your Lifetime Capital Gains Exemption by "purifying" your operating company's balance sheet. To claim the 2026 LCGE limit of approximately $1,275,000, 90 percent of your Opco's assets must be used in active business at the time of sale. The Holdco allows you to siphon off excess cash and passive investments that would otherwise disqualify your shares from this significant tax-free windfall.

How much money should my business be making before I consider a holding company?

You should consider a holding company once your business consistently generates more profit than you need for your personal lifestyle and immediate business operations. There is no hard dollar limit, but many professionals suggest the "break-even" point occurs when you can leave at least $50,000 of profit inside the corporation annually. At this level, the benefits of tax deferral and holding company tax planning typically justify the additional professional fees.

Is a holding company the same as a professional corporation (PC)?

A holding company is not the same as a professional corporation (PC), although they often work together in a tiered structure. A PC is a specific entity for regulated professionals like doctors, lawyers, or accountants to provide their services. In many provinces, a professional can own their PC, which in turn is owned by a holding company to manage investments, provided provincial regulatory bodies allow such ownership structures.

Article by

Mahad Mohamed

Mahad Mohamed is an accountant and the CEO of Tax Partners, with over 26+ years of Canadian and international tax and accounting experience. His expertise includes corporate reorganization, cross-border tax structuring (Canada & US), tax disputes, CRA audits, and tax planning for small owner-managed private corporations. Most recently, Mahad is a pioneer in Canadian crypto taxation and founded Block3 Finance.

Previously, Mahad worked for the Canada Revenue Agency (CRA), Big4 accounting firms, and served as a Rulings Officer for the Federal Tax Authority of the UAE before acquiring Tax Partners in 2014.

Tax Partners has 44 full-time accountants and over 18,400+ clients.

Disclaimer

This article provides general information only and is current as of its publication date. It has not been updated and may be out of date. It does not constitute legal advice and should not be relied upon as such. Every tax situation is unique and may differ from the examples discussed in this article. If you have specific questions, you should seek the advice of our accountants for your unique circumstances. Book a FREE Initial Consultation Today!

Frequently Asked Questions

The Relationship Between Holdco and Opco

The most common structure involves a parent company (Holdco) sitting directly above an operating business (Opco). This hierarchy creates a clear division of labour. While the Opco manages the front line risks of employees, customers, and suppliers, the Holdco acts as a central reservoir for surplus capital. Moving excess cash from the Opco to the Holdco effectively moves it out of the line of fire. This structure serves as the bedrock for sophisticated holding company tax planning, allowing for the tax-efficient transfer of funds before they're exposed to the higher personal tax rates associated with individual withdrawals.

Common Use Cases for Canadian Entrepreneurs

Business owners often adopt this model to consolidate multiple ventures under one roof, making it easier to manage cash flow across different industries. It's also a powerful tool for risk mitigation. For example, you might house your company's valuable intellectual property or real estate in a Holdco while the Opco handles the riskier operational tasks. If the Opco faces a legal challenge, the assets in the Holdco remain protected. A tiered structure is also indispensable for succession. It allows you to introduce new shareholders or prepare for a sale without disrupting the core operations of the business. It's a proactive way to build a legacy that lasts. One of the most compelling reasons for holding company tax planning is the ability to move funds between connected corporations tax-free. Section 112 of the Income Tax Act serves as the engine for this strategy. It allows an operating company to pay dividends to its parent holding company without any immediate tax consequences. This is a massive advantage compared to taking a personal dividend, which in 2026 can attract tax rates of nearly 39 percent for high-income earners in provinces like Ontario. By keeping the cash within the corporate group, you protect it from both high personal taxes and the operational risks of the Opco. This structure essentially turns your Holdco into a "corporate bank." The power of tax deferral lies in its ability to keep more of your capital working for you. When you withdraw profits personally, you're often left with 60 or 70 cents on the dollar after the CRA takes its share. By moving those funds to a Holdco, you keep 100 cents on the dollar to reinvest in new ventures or passive assets. It's about maintaining financial momentum. This strategy is a cornerstone of effective holding company tax planning, especially for entrepreneurs looking to scale without the friction of immediate personal tax liabilities. Under the 2026 rules, navigating the Tax on Split Income (TOSI) remains a priority. While the rules are strict, a well-structured holding company still offers legitimate ways to manage family wealth. You must ensure you meet the "excluded business" or "excluded shares" criteria to avoid the highest marginal tax rate on payments to family members. It requires precision and a proactive approach to ensure your income-splitting strategies remain compliant with current legislation.

The Section 85 Rollover: Transitioning Without Tax

Transitioning your existing business into a Holdco structure doesn't have to be a taxable event. A Section 85 rollover is a tax-neutral transfer mechanism that allows Canadian shareholders to move assets into a corporation in exchange for shares without triggering immediate capital gains. To execute this correctly, you must file a valid election with the CRA, ensuring the "agreed amount" falls within the specific limits defined by the Income Tax Act. This technical maneuver allows you to reorganize your affairs while preserving your hard-earned equity for the long term.

Optimizing Shareholder Remuneration

Deciding between a salary or a dividend is a classic dilemma that becomes more nuanced with a holding company. You can use your Holdco to time personal income spikes, keeping yourself in a lower tax bracket during high-profit years by retaining funds in the corporation. Additionally, the Capital Dividend Account (CDA) is a vital tool. It allows you to distribute the non-taxable portion of capital gains to shareholders entirely tax-free. Consulting with a firm that specializes in Canadian accounting and tax services can help you determine the ideal balance for your specific financial goals. Many entrepreneurs hesitate to implement a Holdco because they fear it might jeopardize their Small Business Deduction (SBD). It's a legitimate concern. Within the framework of holding company tax planning, the "SBD grind" is a pivotal risk factor that requires proactive management. The Canadian tax system reduces the business limit for corporations that generate significant passive investment income. Once your associated corporate group earns more than $50,000 in Adjusted Aggregate Investment Income (AAII), your access to the lower 9 percent federal small business tax rate starts to shrink. The math is unforgiving. For every $1 of investment income earned above the $50,000 threshold, your $500,000 small business limit drops by $5. By the time your passive income hits $150,000, your SBD is gone. This shift can push your active business income from a combined tax rate of approximately 12.2 percent in Ontario up to the general rate of 26.5 percent. Meticulous bookkeeping and precise filing are your only defences against an unexpected CRA audit. You must track every dollar of interest, rental income, and capital gains to ensure your corporate group stays within these critical limits.

CRA Scrutiny and Anti-Avoidance Rules

The 2026 tax landscape involves heightened vigilance from the CRA, particularly regarding the General Anti-Avoidance Rule (GAAR). Strategies that lack genuine commercial substance or exist solely to circumvent passive income rules are under the microscope. You must document inter-company loans with formal agreements and market-interest rates to avoid "deemed dividend" traps. If the CRA perceives a structure as a "sham," the resulting reassessments and penalties can quickly erase any intended tax savings. Maintaining corporate integrity is not just a best practice; it's a survival strategy.

Managing the Complexity of Multiple Corporations

Adding a holding company increases your administrative overhead. You'll face higher costs for professional accounting and tax preparation because you're now filing for two or more entities. Coordinating year-ends is a strategic move that can maximize tax deferral, but it requires careful planning. Most business owners find the "break-even" point occurs when the tax-free inter-corporate dividends and asset protection benefits significantly outweigh these annual compliance costs. It's about finding the right balance between sophisticated protection and manageable complexity for your specific situation. For many Canadian founders, the Lifetime Capital Gains Exemption (LCGE) represents the ultimate reward for years of risk and hard work. In 2026, this exemption shelters approximately $1,275,000 of capital gains from tax, potentially saving an individual over $250,000 in personal taxes upon the sale of their business. However, this benefit isn't automatic. To qualify, your company must meet the strict definition of a Qualified Small Business Corporation (QSBC). This is where holding company tax planning becomes an essential defensive strategy rather than just a financial preference. The Canada Revenue Agency applies two primary asset tests to determine QSBC status. Throughout the 24 months before a sale, more than 50 percent of the fair market value of the corporation's assets must be used in an active business carried on primarily in Canada. More critically, the LCGE requires 90% of assets to be used in active business at the time of sale. If your operating company (Opco) accumulates too much "dead" asset value, such as excess cash, GICs, or investment properties, you risk failing these tests and losing the exemption entirely. A holding company acts as a vital purification tool, siphoning off these redundant assets to keep the Opco "pure" and compliant.

The Multi-Year Purification Strategy

Purification isn't a one-time event you can handle weeks before a sale; it requires a disciplined, multi-year approach. You don't want to be caught with a balance sheet full of passive investments when a surprise acquisition offer arrives. Effective purification follows a steady rhythm:

Multiplying the Exemption Through Family

A sophisticated holding company tax planning strategy often involves a Family Trust. By having a trust own shares in your Holdco, you can potentially multiply the $1,275,000 LCGE across multiple family members, provided you navigate the 2026 TOSI rules carefully. This structure is frequently paired with an "estate freeze," which locks in the current value of the business for the founder while allowing future growth to accrue to the next generation. If you're planning an exit or a transition, our experts in Canadian accounting and tax services can help you purify your structure and maximize your family's after-tax wealth. Successful holding company tax planning isn't a product you buy off the shelf. It's a living strategy that must evolve alongside your business and your family's changing needs. At Tax Partners, we've spent 40 years helping Canadian SMEs navigate the complexities of corporate tax evolution. We recognize that no two businesses are identical. A structure that works for a real estate holding company won't necessarily suit a manufacturing firm looking for a five-year exit. We act as your proactive guardian, spotting potential CRA pitfalls and regulatory shifts before they become costly liabilities. Our approach integrates corporate accounting with wealth management and estate planning under a single roof. This holistic view ensures that every inter-corporate dividend or share reorganization serves a broader purpose. We don't just react to requirements; we look ahead to secure a better outcome for your estate. By housing these diverse financial disciplines together, we provide a seamless experience that eliminates the friction often found when working with multiple, disconnected advisors. It's about providing a steady hand at the helm while you focus on growing your enterprise.

The Tax Partners Planning Process

Assessing your current corporate health is our first priority. We begin with an initial diagnostic to understand your current structure and your long-term financial goals. Once we have a clear roadmap, our team manages the technical design and execution of Section 85 rollovers or complex share reorganizations with meticulous precision. Our commitment continues well after the initial setup. we provide ongoing vigilance through quarterly reviews to ensure your Opco remains pure for the LCGE and your Small Business Deduction is optimized against the 2026 passive income rules.

A Steady Hand for Your Corporate Future

Moving from a state of financial uncertainty to a feeling of total control over your tax liabilities is a transformative experience for any entrepreneur. You deserve the peace of mind that comes from a long-term partnership with seasoned CPAs who are deeply invested in your success. We combine decades of institutional wisdom with a modern, forward-thinking outlook to protect what you've built. It's about more than just numbers; it's about securing your family's hard-earned legacy. Secure your business legacy with a custom holding company strategy from Tax Partners. Effective holding company tax planning is the foundation of a resilient financial future. We've explored how a Holdco serves as a protective vault for your wealth, allowing you to move profits tax-free and keep your business "pure" for the $1.275 million capital gains exemption. This isn't just about immediate savings. It's about building a structure that withstands the complexities of the 2026 tax landscape while securing your family's long-term interests. You've invested years into your business, and your corporate structure should reflect that dedication. With over 40 years of Canadian tax expertise and more than 495,000 returns filed, our team has saved over $87 million for our clients. Our 1,390+ five-star Google reviews reflect our commitment to being a proactive guardian for every business owner we serve. Don't leave your hard-earned equity to chance. Book a consultation with Tax Partners to optimize your corporate structure and gain total control over your financial roadmap. You've worked hard to build your success. We're here to ensure it stays protected for the generations to come.

What is the primary purpose of a holding company for a Canadian small business?

The primary purpose of a Canadian holding company is to protect corporate assets from business liabilities and facilitate tax-efficient wealth accumulation. By housing surplus cash or investments in a separate entity, you shield those resources from potential creditors of your operating company. This structure also enables seamless inter-corporate dividends, allowing you to move funds without triggering the high personal tax rates associated with individual income.

Can a holding company help me avoid paying personal income tax?

A holding company does not allow you to avoid personal income tax entirely, but it is a powerful tool for tax deferral. You only pay personal tax when you withdraw funds from the corporation as a salary or dividend. By retaining earnings within the Holdco, you keep more capital working for you at the lower corporate tax rate, which is a core benefit of proactive holding company tax planning.

How does the CRA define passive income within a holding company in 2026?

In 2026, the CRA defines passive income as Adjusted Aggregate Investment Income (AAII), which includes interest, rental income, and taxable capital gains. This definition is critical because once your corporate group earns more than $50,000 in AAII, your Small Business Deduction begins to decrease. This "grind" reduces your access to the 9 percent federal small business tax rate, eventually eliminating it once passive income reaches $150,000.

Is it expensive to maintain a holding company in Canada?

Maintaining a holding company involves additional costs, including separate annual tax filings, bookkeeping, and legal minute book updates. While these administrative expenses are higher than managing a single corporation, the tax savings and asset protection benefits often outweigh the overhead for established businesses. Most owners find the structure becomes cost-effective once their operating company consistently generates more cash than is needed for personal living expenses.

Can I use my holding company to buy a personal home or vehicle?

Using a holding company to purchase personal assets like a home or vehicle is generally ill-advised because it triggers "shareholder benefit" rules. The CRA views the personal use of corporate assets as a taxable benefit, meaning you would likely pay tax on the value of that use as if it were income. It's almost always more tax-efficient to buy personal assets with after-tax personal funds rather than risking a costly audit.

What happens to the Lifetime Capital Gains Exemption if I have a holding company?

A holding company protects your Lifetime Capital Gains Exemption by "purifying" your operating company's balance sheet. To claim the 2026 LCGE limit of approximately $1,275,000, 90 percent of your Opco's assets must be used in active business at the time of sale. The Holdco allows you to siphon off excess cash and passive investments that would otherwise disqualify your shares from this significant tax-free windfall.

How much money should my business be making before I consider a holding company?

You should consider a holding company once your business consistently generates more profit than you need for your personal lifestyle and immediate business operations. There is no hard dollar limit, but many professionals suggest the "break-even" point occurs when you can leave at least $50,000 of profit inside the corporation annually. At this level, the benefits of tax deferral and holding company tax planning typically justify the additional professional fees.

Is a holding company the same as a professional corporation (PC)?

A holding company is not the same as a professional corporation (PC), although they often work together in a tiered structure. A PC is a specific entity for regulated professionals like doctors, lawyers, or accountants to provide their services. In many provinces, a professional can own their PC, which in turn is owned by a holding company to manage investments, provided provincial regulatory bodies allow such ownership structures.